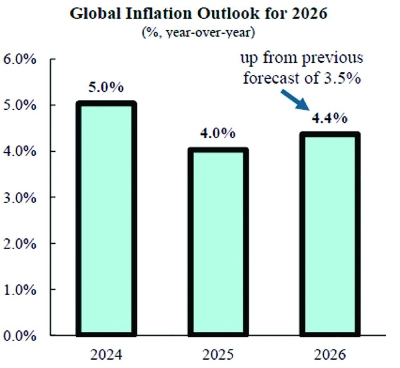

At the beginning of the year, the global economy was on a steady path of stable growth and diminishing inflation. This trajectory was suddenly disrupted by the Iran conflict, QNB stated in its latest economic report.Prior to the beginning of hostilities on February 28, global headline inflation was on a continuous downward trend from its post-Covid-19 pandemic peak of 9% in 2022. Price increases were gradually converging towards central bank targets across advanced and emerging economies alike, QNB stated.“That trajectory has now sharply reversed. Global headline inflation is now projected at 4.4% for 2026, an upward revision of 0.9 percentage points from the pre-conflict forecast of 3.5%. What had been shaping up as a year of monetary policy normalisation could now turn into a new cycle of inflationary pressures defined by a major energy shock,” stated QNB.Following the US-Israeli military campaign against Iran, launched on February 28, Tehran retaliated by effectively closing the Strait of Hormuz – the waterway through which approximately 20% of the world’s oil and liquefied natural gas (LNG) normally flows.Brent crude surged by more than 25% in the weeks that followed, reaching above $120 per barrel at its peak, before settling near $110 per barrel in early April, while LNG spot prices in Asia increased by more than 85% since the initial strikes. The inflationary consequences of this energy shock are already materialising.“An energy shock of this magnitude operates through two distinct channels. The first is the direct, or headline, effect: The immediate pass-through of higher oil and gas prices into fuel, electricity, and transportation costs, which is visible and felt immediately by households and businesses.“The second, is the indirect effect on core inflation – the underlying price dynamics that strip out volatile energy and food components – through which higher energy costs gradually feed into production costs, wages, and services prices, embedding themselves more persistently in the broader price level,” stated the QNB report, which discusses the inflation effects across the globe, delving into the US, the Euro Area, and Asia.As a net energy exporter, the US is structurally less exposed to crude oil supply disruptions than Europe or Asia. However, the inflation outlook was already challenging, since tariff-driven goods inflation had been creating pressures and feeding into consumer prices, QNB stated.Following the outbreak of hostilities, gasoline prices crossed $4 per gallon, up by close to $1. Headline inflation surged to 3.3% year-on-year (y-o-y) in March, well above the Federal Reserve’s 2% annual target.Core CPI, which excludes items with more volatile prices such as food and energy, came in at 2.6% y-o-y, with early signs of broadening pass-through into transportation, food, and services. With this, the IMF raised its US inflation forecast for this year to 2.8%. “This development complicates the Federal Reserve’s ability to characterise the inflation surge as a purely transitory energy spike, creating an additional challenge for upcoming monetary policy decisions,” QNB pointed out.In contrast to the US, QNB stated that the Euro Area is nearly fully import-dependent for both oil and natural gas, and therefore much more sensitive to energy price disruptions. Therefore, the consequences were immediate and measurable, noted QNB.The Euro Area headline inflation jumped from 1.9% in February 2026 to 2.5% in March, driven by a swing in energy prices with an annual increase of 5.1%. The shift was broad-based across the bloc’s largest economies, with Germany recording 2.8%, Spain 3.4%, France 2.0%, and the Netherlands 2.6%, reflecting structural differences in how energy prices are transmitted into consumer prices across member states.“Before the conflict, the ECB had succeeded in stabilising inflation near its 2% target after the most aggressive tightening cycle in its history. That hard-won disinflation is now under direct threat, with headline inflation expected to reach 3.0% for 2026,” QNB stated.The shock of the war in Iran represents a major supply disruption for Asia. The region accounts for around 80-85% of crude oil and LNG that normally transits the Strait of Hormuz, making it structurally the most exposed geography to the closure of this critical chokepoint.The IMF projects Emerging Asia inflation rising from 1.9% in 2025 to 2.7% in 2026. According to QNB, China is relatively better insulated but not immune. China imports around 45% of its oil from the Middle East but has benefited from large strategic reserves, continued access to Russian energy supplies and its shift toward renewables.“Nevertheless, higher energy costs are feeding into production costs for high energy-intensive sectors such as steel and chemicals, as well as for electronics. In South Asia, the acceleration is even more pronounced, with inflation projected to reach 5% this year.“In addition to higher energy costs, a stronger US dollar reflects the domestic currency depreciation and the higher cost of imported goods. This amplifies the inflationary effects, feeding into fertilisers, food, and transportation costs,” noted QNB.QNB added: “The Iran war has delivered a significant blow to the global disinflation trend, with global headline inflation now projected at 4.4% – a sharp reversal from the pre-conflict trajectory. The shock is producing a broad-based inflation acceleration across major economies. In all three major regions – the US, the Euro Area, and Asia – the critical variable remains the speed at which energy supply will normalise.”

")