Qatar’s bonds are “likely to remain popular with investors” although sovereign creditworthiness in the Mena economies will broadly deteriorate over the coming quarters given rising interest rates, tightening liquidity and a slowdown in growth, a new report has shown.

Qatar, Kuwait and the UAE have been “proactive in carrying out fiscal reform”, and can rely on extensive sovereign wealth fund holdings, BMI Research said in a recent analysis on the Mena region’s sovereign debt.

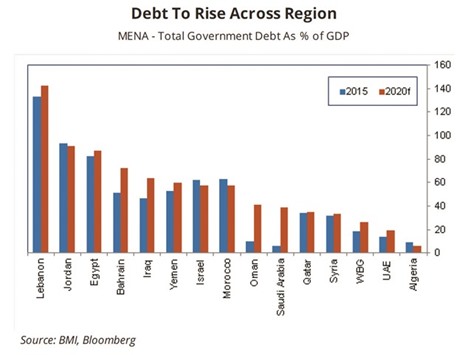

While the GCC is well positioned, the outlook is more concerning for Egypt and Lebanon, it said.

Sovereign debt risk will increase across the Mena economies over the coming quarters as lower oil prices and the slow pace of fiscal reform are hindering revenue generation and forcing increased government borrowing.

While oil prices bottomed in Q1, 2016, BMI Research forecasts only a modest pickup over the coming years, with prices remaining far off the average price of $107.6/barrel recorded between 2011 and 2014.

“We project Brent to average $46.5/b in 2016 and $57/b in 2017,” the Fitch Group Company said.

This, it said would “stand below the budget breakeven levels” for nearly all Mena oil producers and force most sovereigns to tap debt markets before December of this year and beyond.

“While intuitively it may seem that the oil importers will face a more benign operating environment, in the case of Lebanon and Egypt this is outweighed by the negative impact of modest economic growth, tightening liquidity and, in the latter’s case, our expectation for a devaluation in the currency,” BMI Research said.

The report said, “We forecast rising fiscal deficits across the oil exporters and only a slight improvement in the fiscal position in the oil importers over the coming year; indeed only Qatar will register a budget surplus in 2016. These deficits will broadly be financed by turning to the debt markets, resulting in some large increases in debt as a percentage of GDP.”

The GCC States, BMI Research said, are turning to the market at a time of hardening investor sentiment, as reflected in a sustained rise in credit default swap (CDS) spreads since 2015.

Saudi Arabia’s five-year CDS has surged by 95 basis points since October 2015, a more significant widening than seen for the more vulnerable Bahrain.

Certainly, the deterioration observed across a wide range of fundamental economic indicators means that further downgrades to the Gulf States’ sovereign credit rating are likely in the current second half of this year, following S&P and Fitch’s cuts to Saudi Arabia and Oman’s ratings around the turn of 2016.

An increasing supply of bonds across Mena combined with more modest support from local investors (owing to growing liquidity constraints) will also put pressure on the GCC’s overseas debt issues over H2, 2016 and 2017, forcing governments to issue at higher yields than have been the case in recent years, the report noted.

“That said, we expect investors to differentiate between Bahrain and Oman on the one hand, and the UAE, Kuwait, and Qatar on the other,” BMI Research said.

In the case of the former, limited foreign reserve buffers increase the vulnerabilities: Oman’s ability to defend the currency against speculative outflows is thus more limited than its peers, and Bahrain already has an elevated debt ratio by emerging market standards.

By contrast, BMI Research said, “The UAE and Qatar have been proactive in carrying out fiscal reform, and can rely on extensive sovereign wealth fund holdings (as can Kuwait). Their bonds are likely to remain popular with investors.”