Activity is expected to diverge across regions and geographies although the global economy has been slowing down, QNB has said in an economic commentary.

But as global inflation soared amid the combination of strong demand with supply chain constraints on logistics and energy, the recovery momentum started to fade. This has been caused by the withdrawal of policy support, monetary policy tightening, supply disruptions and idiosyncratic dynamics across regions. The result is higher inflation with a squeeze in disposable incomes globally.

While the latest print of 52.4 for the global manufacturing PMI is still comfortably within expansionary territory, there are signs of a slowdown or even reversal of economic activity.

Nevertheless, QNB noted different patterns can be observed across regions and geographies. Its analysis delves into the regional-specificities to explain the global divergence.

In the US, since the beginning of the pandemic, strong policy stimulus and support left the private sector in a strong position, with growth peaking in March 2021.

Activity remained firm in the US but less fiscal support, high inflation and a less accommodative (hawkish) Federal Reserve started to weigh on growth in recent months. The slowdown is set to continue over the next several months, with a potential recessionary risk at a later stage.

In the Euro area, where the economic impact of the pandemic was harsher and policy support was delayed, the recovery peaked in June 2021.

Activity is slowing at a very fast pace in the Euro area as the continent faces a quadruple shock of less fiscal support, higher inflation, a less accommodative European Central Bank and geopolitical turmoil, due to the Russo-Ukrainian conflict.

The geopolitical situation, in particular, is likely to drive the Euro area into a recession before the end of the year, QNB said.

A reversal of the negative momentum is unlikely any time soon, as this would require a conflict resolution in Eastern Europe or some stable alternative solutions for the energy crisis. This seems uncertain at the moment, as the conflict has entered a prolonged state.

China, on the other hand, is in a very different place. The country had a much more effective initial response to the pandemic, which allowed for a quicker recovery and a shorter period of policy stimulus.

In fact, the Chinese economic rebound peaked in November 2020. Thereafter, however, the Chinese economic performance worsened significantly, spurred by an early withdrawal of policy stimulus, a comprehensive regulatory tightening in key industries (real estate, consumer products and technology) and the ‘Zero-Covid’ response to new waves of the pandemic.

Continuing Omicron outbreaks in recent weeks led to hard lockdowns and social distancing measures across areas that generate 40% of China’s GDP and ship 80% of its exports. As a result, China’s recent manufacturing PMI prints have slipped into contractionary territory.

Nevertheless, authorities have taken necessary measures with more accommodative fiscal policy, an easing of the central bank policy stance and a more moderate regulatory tightening. Furthermore, once the Omicron wave recedes, we expect that the current situation will improve and the outlook will brighten.

Finally, member countries of the Association of Southeast Asian Nations (ASEAN) are also on a different path. After underperforming advanced economies for several quarters, on the back of the Delta wave of the pandemic, lower vaccination rates and more modest policy support, they are now seeing some relief. Activity bottomed from the Delta slump in August 2021 and is since then recovering as vaccination rates improved, social distancing measures eased and the economic recovery resumed.

QNB expects economic activity to further gain momentum for commodity export-driven economies, such as Indonesia and Malaysia. On the other hand, growth will be more subdued for net commodity importers, such as in Thailand, the Philippines and Vietnam.

“All in all, while the global economy has been slowing down, the picture looks very different across regions and geographies. This, however, assumes that inflation will moderate, supply chain constraints ease and geopolitical conflicts do not worsen,” QNB added.

In early 2021, when several major economies were benefiting from a stimulus-driven recovery from the pandemic, activity indicators had a sharp positive run, QNB noted.

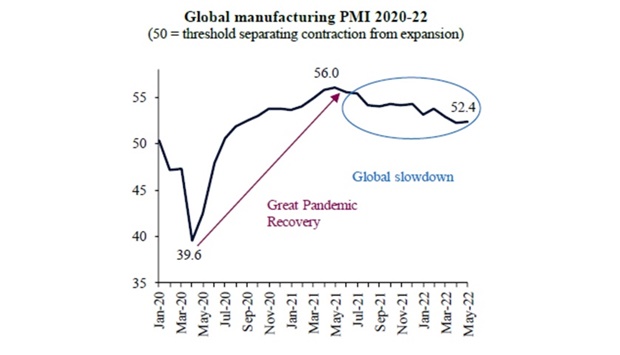

The global manufacturing Purchasing Managers’ Index (PMI), a survey-based indicator that measures whether several components of activity improved or deteriorated versus the previous month, peaked at a high of 56 in May 2021. Traditionally, an index reading of 50 serves as a threshold to separate contractionary (below 50) from expansionary (above 50) changes in business conditions.

The global manufacturing Purchasing Managers’ Index (PMI), a survey-based indicator that measures whether several components of activity improved or deteriorated versus the previous month, peaked at a high of 56 in May 2021. Traditionally, an index reading of 50 serves as a threshold to separate contractionary (below 50) from expansionary (above 50) changes in business conditions.

But as global inflation soared amid the combination of strong demand with supply chain constraints on logistics and energy, the recovery momentum started to fade. This has been caused by the withdrawal of policy support, monetary policy tightening, supply disruptions and idiosyncratic dynamics across regions. The result is higher inflation with a squeeze in disposable incomes globally.

While the latest print of 52.4 for the global manufacturing PMI is still comfortably within expansionary territory, there are signs of a slowdown or even reversal of economic activity.

Nevertheless, QNB noted different patterns can be observed across regions and geographies. Its analysis delves into the regional-specificities to explain the global divergence.

In the US, since the beginning of the pandemic, strong policy stimulus and support left the private sector in a strong position, with growth peaking in March 2021.

Activity remained firm in the US but less fiscal support, high inflation and a less accommodative (hawkish) Federal Reserve started to weigh on growth in recent months. The slowdown is set to continue over the next several months, with a potential recessionary risk at a later stage.

In the Euro area, where the economic impact of the pandemic was harsher and policy support was delayed, the recovery peaked in June 2021.

Activity is slowing at a very fast pace in the Euro area as the continent faces a quadruple shock of less fiscal support, higher inflation, a less accommodative European Central Bank and geopolitical turmoil, due to the Russo-Ukrainian conflict.

The geopolitical situation, in particular, is likely to drive the Euro area into a recession before the end of the year, QNB said.

A reversal of the negative momentum is unlikely any time soon, as this would require a conflict resolution in Eastern Europe or some stable alternative solutions for the energy crisis. This seems uncertain at the moment, as the conflict has entered a prolonged state.

China, on the other hand, is in a very different place. The country had a much more effective initial response to the pandemic, which allowed for a quicker recovery and a shorter period of policy stimulus.

In fact, the Chinese economic rebound peaked in November 2020. Thereafter, however, the Chinese economic performance worsened significantly, spurred by an early withdrawal of policy stimulus, a comprehensive regulatory tightening in key industries (real estate, consumer products and technology) and the ‘Zero-Covid’ response to new waves of the pandemic.

Continuing Omicron outbreaks in recent weeks led to hard lockdowns and social distancing measures across areas that generate 40% of China’s GDP and ship 80% of its exports. As a result, China’s recent manufacturing PMI prints have slipped into contractionary territory.

Nevertheless, authorities have taken necessary measures with more accommodative fiscal policy, an easing of the central bank policy stance and a more moderate regulatory tightening. Furthermore, once the Omicron wave recedes, we expect that the current situation will improve and the outlook will brighten.

Finally, member countries of the Association of Southeast Asian Nations (ASEAN) are also on a different path. After underperforming advanced economies for several quarters, on the back of the Delta wave of the pandemic, lower vaccination rates and more modest policy support, they are now seeing some relief. Activity bottomed from the Delta slump in August 2021 and is since then recovering as vaccination rates improved, social distancing measures eased and the economic recovery resumed.

QNB expects economic activity to further gain momentum for commodity export-driven economies, such as Indonesia and Malaysia. On the other hand, growth will be more subdued for net commodity importers, such as in Thailand, the Philippines and Vietnam.

“All in all, while the global economy has been slowing down, the picture looks very different across regions and geographies. This, however, assumes that inflation will moderate, supply chain constraints ease and geopolitical conflicts do not worsen,” QNB added.