Significant tightening of fiscal policies is expected across the G-7 countries over the coming quarters, QNB has said in an economic commentary.

Last year, as the Covid-19 pandemic disrupted activity across the globe, governments and central bank officers came to mitigate the economic impact of the outbreak on countries, corporations, institutions and individuals.

In fact, this was the second time that policymakers engineered such large-scale economic mobilisation plans since World War II.

Major central banks cut policy rates aggressively or supported the financial system with massive injections of liquidity, preventing a disorderly dislocation of credit and equity markets.

More importantly, QNB noted fiscal expansion became paramount. Fiscal policy tools were more appropriate to provide the relief that corporates and households needed.

This, it said was done through different programs, including extensions of paid sick leave and unemployment benefits, tax holidays, direct cash transfers to families, postponement of loan payments, and subsidised loans to small and medium enterprises.

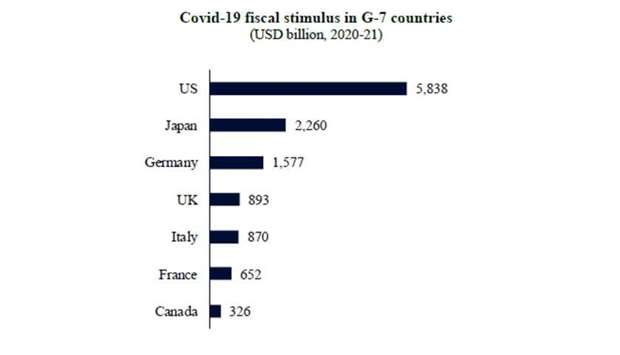

There was no shortage of fiscal policy action to respond to the economic consequences of the pandemic. According to the International Monetary Fund (IMF), extraordinary fiscal stimulus measures amounted to $16.6tn globally in 2020 and 2021.

Half of these measures consisted of additional spending or foregone revenue with the other half including “below the line measures,” such as loans, guarantees and equity injections. Importantly, around 75% of the total fiscal support was deployed by the major economies of the G-7 (Canada, France, Germany, Italy, Japan, the UK, and the US).

However, while extremely stimulative fiscal policies were key to mitigate the impact of the pandemic, QNB does not expect this to continue. Two factors underpin its view.

First, on a year-on-year (y/y) basis, the reduction of fiscal stimulus produces a negative effect on total GDP contribution, as less government spending or more taxation produce a hit to total demand. Deficits are already moderating and the negative y/y contribution is expected to be particularly large in the US, Japan and the UK, where the scale of the stimulus was also bigger than in other G-7 economies after the pandemic started.

Such sizeable drag in these large economies is set to cap global demand next year, offsetting the positive impact of private investment growth and the expected relaxation of supply constraints. This will increase the risks of negative surprises for global growth moving forward.

Second, as the economic recovery matures, there are no serious underlying reasons for large doses of fiscal stimulus to the G-7 countries anymore. With employment strengthening, investments picking up and consumption surging, the demand for extraordinary fiscal policy fades.

Moreover, after a period of large fiscal deficits, G-7 governments need to stabilise their finances to avoid the risks of fiscal profligacy or continuous overspending. This has already started in the US, after the government delivered the last batch of direct cash transfers and expanded unemployment benefits to the population over the last few months.

A similar process is also taking place in Europe, where support benefits are expiring and new fiscal initiatives are more modest than the previous emergency measures. In Japan, while funds are still widely available for new investments, execution is slow and the government spending should moderate over the next couple of years.

“All in all, we expect to see a significant tightening of fiscal policies across the G-7 over the coming quarters. This will likely weight on the ongoing economic recovery, limiting the prospects for continued strong growth in major economies. This will also make the global economy more vulnerable to shocks or negative events, as private demand is more sensitive to overall economic conditions,” QNB said.

Last year, as the Covid-19 pandemic disrupted activity across the globe, governments and central bank officers came to mitigate the economic impact of the outbreak on countries, corporations, institutions and individuals.

In fact, this was the second time that policymakers engineered such large-scale economic mobilisation plans since World War II.

Major central banks cut policy rates aggressively or supported the financial system with massive injections of liquidity, preventing a disorderly dislocation of credit and equity markets.

More importantly, QNB noted fiscal expansion became paramount. Fiscal policy tools were more appropriate to provide the relief that corporates and households needed.

This, it said was done through different programs, including extensions of paid sick leave and unemployment benefits, tax holidays, direct cash transfers to families, postponement of loan payments, and subsidised loans to small and medium enterprises.

There was no shortage of fiscal policy action to respond to the economic consequences of the pandemic. According to the International Monetary Fund (IMF), extraordinary fiscal stimulus measures amounted to $16.6tn globally in 2020 and 2021.

Half of these measures consisted of additional spending or foregone revenue with the other half including “below the line measures,” such as loans, guarantees and equity injections. Importantly, around 75% of the total fiscal support was deployed by the major economies of the G-7 (Canada, France, Germany, Italy, Japan, the UK, and the US).

However, while extremely stimulative fiscal policies were key to mitigate the impact of the pandemic, QNB does not expect this to continue. Two factors underpin its view.

First, on a year-on-year (y/y) basis, the reduction of fiscal stimulus produces a negative effect on total GDP contribution, as less government spending or more taxation produce a hit to total demand. Deficits are already moderating and the negative y/y contribution is expected to be particularly large in the US, Japan and the UK, where the scale of the stimulus was also bigger than in other G-7 economies after the pandemic started.

Such sizeable drag in these large economies is set to cap global demand next year, offsetting the positive impact of private investment growth and the expected relaxation of supply constraints. This will increase the risks of negative surprises for global growth moving forward.

Second, as the economic recovery matures, there are no serious underlying reasons for large doses of fiscal stimulus to the G-7 countries anymore. With employment strengthening, investments picking up and consumption surging, the demand for extraordinary fiscal policy fades.

Moreover, after a period of large fiscal deficits, G-7 governments need to stabilise their finances to avoid the risks of fiscal profligacy or continuous overspending. This has already started in the US, after the government delivered the last batch of direct cash transfers and expanded unemployment benefits to the population over the last few months.

A similar process is also taking place in Europe, where support benefits are expiring and new fiscal initiatives are more modest than the previous emergency measures. In Japan, while funds are still widely available for new investments, execution is slow and the government spending should moderate over the next couple of years.

“All in all, we expect to see a significant tightening of fiscal policies across the G-7 over the coming quarters. This will likely weight on the ongoing economic recovery, limiting the prospects for continued strong growth in major economies. This will also make the global economy more vulnerable to shocks or negative events, as private demand is more sensitive to overall economic conditions,” QNB said.