They’ve been billed as a solution to the rock-bottom interest rates weighing down the returns of America’s asset managers.

Collateralised loan obligations – which package and sell leveraged loans into chunks of varying risk and return – have been touted as safe, high-yielding alternatives to everything from government bonds and mortgage securities to corporate debt.

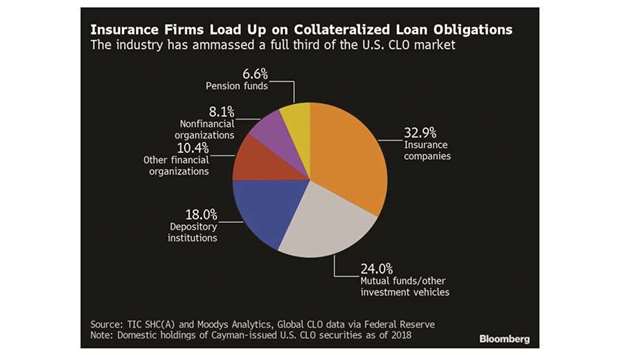

And one industry more than any other has gone all in.

Insurers have become the biggest US investors in the market, topping banks and hedge funds to amass a third of all domestic holdings, according to data compiled by the Federal Reserve. The love affair was sudden: By the end of 2019, they owned $158bn of CLO bonds, a 22% jump from the prior year and almost double what they had in 2016, according to Barclays Plc figures.

What makes this especially alarming is the fact that some insurers – from Athene Holding Ltd to American Equity Investment Life Holding Co – loaded riskier slices of CLOs rated BB and BBB into their portfolios. Now loan defaults are rising and recovery rates are falling. In a stress test released in June by the National Association of Insurance Commissioners, a severe recession would result in enough losses to completely wipe out the capital and surplus of four insurance firms and hobble a handful of others. They declined to name which ones.

“Using realistic modelling assumptions that reflect this new pandemic-affected world we are in, there are BBB and lower bonds that could suffer from interest shortfall and principal loss,” said Jason Merrill, a CLO specialist at Penn Mutual Asset Management, which oversees about $28bn, largely on behalf of insurers. “So investors that are going to participate in those lower-rated tranches need to go in with eyes wide open about potential future issues.” Representatives for Athene – co-founded and part owned by Apollo Global Management Inc – and American Equity said their own analysis of their CLO portfolios indicate they would actually show resiliency in a downturn.

To be clear, no one is predicting a repeat of 2008, when collateralised debt obligations – the more dangerous cousins of CLOs – helped bring down what was once the world’s largest insurance company, American International Group Inc, and nearly the entire global financial system along with it.

This go around, the risk appears to be more idiosyncratic. Some firms, like Prudential Financial Inc and MetLife Inc, hold large swaths of AAA rated CLO tranches, the safest and least likely to face principal losses should the default cycle worsen. Even in the NAIC’s most draconian scenarios, AAA bonds were unscathed, a big reason why it ultimately concluded that CLOs weren’t a significant risk to the industry as a whole.

But others, including Athene, American Equity, Fidelity National Financial Inc’s FGL Holdings and Eldridge Industries’ Security Benefit Life Insurance Co have piled into lower-rated assets.

About 9%, or $11bn, of Athene’s invested assets were in CLOs as of the end of March, according to a first quarter earnings presentation. Of that, nearly 40% of were rated BBB. That means that under an NAIC stress scenario where BBB bonds take a 25% principal and interest loss, Athene would experience a $1.2bn hit. A severe recession could lead to losses of about $3.7bn, based on the regulatory body’s analysis.

A representative for Athene said that the methodology used in the NAIC study resulted in “extreme illustrative outcomes” that are unlikely to reflect the actual performance of CLOs under stress. Based on the company’s own estimates, even in the most severe model, the broader industry would experience double the rate of impairments that Athene would see on its BBB CLOs.

American Equity has also amassed significant CLO investments. The firm held $4.8bn of CLOs as of March, about 9% of its assets, of which 55% consists of BBBs and 8% of BB bonds. Fitch Ratings estimates that Athene and American Equity have CLO holdings in excess of 75% of their total adjusted capital.

“Resiliency analysis of our CLO book indicates that we are unlikely to see permanent credit losses even if peak default rates are 25% higher than actual during the global financial crisis, and no modelled loss to our BBB and higher even if peak defaults are 75% higher,” Anant Bhalla, chief executive officer of American Equity, said in an e-mailed statement.

FGL and Security Benefit didn’t respond to multiple requests for comment. Of course, insurers aren’t the only ones to increase their exposure to CLOs in recent years. The market has ballooned over the past decade, fuelled by significantly higher payouts relative to comparably rated bonds.

CLO tranches rated BBB currently yield about 5.01%, according to Palmer Square index data. In comparison, the Bloomberg Barclays US Aggregate Baa index is hovering near a record low 2.34%.

The asset class’s strong performance during the financial crisis, when few CLOs saw material losses, has also helped lure buyers. Moreover, post-crisis changes have led to bigger equity cushions, more limitations on risk taking and other investor protections.

But while the structure has gotten safer, the quality of assets that go into CLOs has deteriorated.

Leverage ratios have increased, covenant quality has weakened, and exaggerated earnings have proliferated, all of which are helping fuel higher default rates and lower recovery levels.

The one-year US speculative-grade default rate is forecast to climb to 10.5%, according to a July presentation from Moody’s Investors Service. In a pessimistic economic scenario, that climbs to 18.1%.

And whereas loans have historically recovered about 70 to 80 cents on the dollar, many analysts are recommending investors start reducing that to 50-60 cents when modelling CLO returns going forward. The NAIC used 40 cents in its downside scenarios.