With buyouts at a virtual standstill, private equity firms are finding a new place to put their billions of dollars: Investing in public companies that have been pummeled by the Covid-19 economic collapse.

The technique is a throwback to the 2008 financial crisis when, in one notable deal, Warren Buffett threw a $5bn lifeline to Goldman Sachs Group Inc.

This time around, it’s gotten so popular that the bidding for slices of distressed companies can resemble a heated takeover battle, with as many as 20 private equity firms clamoring for a piece of one deal.

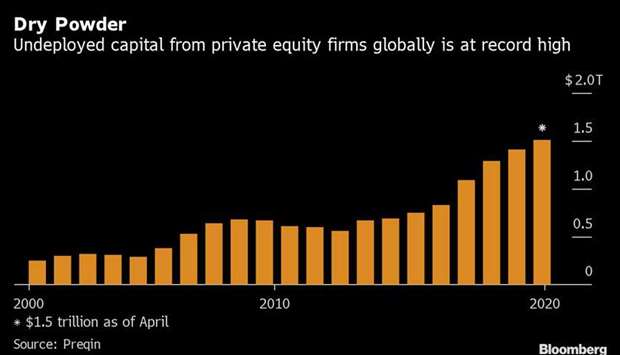

The fever underscores the huge amount of money buyout shops are sitting on – some $2tn – and the dwindling number of traditional buyouts available. The firms are betting that struggling companies such as Cheesecake Factory Inc and Expedia Group Inc will recover once the economy opens up.

Yet the competition for the deals has forced some firms to lower their typically high sights. Nowadays, they are shooting for an internal rate of return in the mid-teens to low 20%, down from 30% to 40% before March, according to estimates by dealmakers.

“There’s so much committed capital trying to find investment opportunities, the processes are highly competitive and terms are reflective of that,” Leo Greenberg, an attorney at Kirkland & Ellis, said.

Since late March, companies have raised about $8bn from buyout shops in negotiated deals known as a PIPE -- private investment in public equity. While buyout shops are typically in business to buy companies outright, these deals instead get them fat dividends and eventually an equity stake.

For struggling companies, PIPE financing still isn’t cheap. But with their stocks depressed, they may have little choice other than to turn to private money. And at the very least, the competition among buyout shops affords them an opportunity to negotiate terms more favorable than existed before the Covid-19 crisis.

Preferred stock: Cheesecake Factory, whose restaurant dining rooms are shut but providing take-out, spoke to about 20 parties before agreeing to a $200mn convertible preferred stock investment from Roark Capital, according to a person with knowledge of the matter who asked not to be identified because the information was private. Roark will get a dividend of 9.5% and can convert the preferred shares into common stock when the shares hit $22.23. Cheesecake Factory declined to comment.

Outfront Media Inc spoke to about 10 parties and ultimately settled on Providence Equity Partners and Ares Management Corp.

Ares was an attractive partner because it was already an investor in the industry though Clear Channel Outdoor Holdings Inc, a person familiar with the matter said. Outfront will pay Providence and Ares a 7% dividend on the preferred shares.

Furniture retailer Wayfair Inc had also spoken to multiple parties before signing on to a $535mn investment with a group of investors including private equity’s Great Hill Partners, which had a stake when Wayfair was still a private company, a person familiar with the matter said. Wayfair declined to comment.

Deal premium: Both Wayfair and Outfront were able to strike deals that allowed for the investors to convert their shares to common stock at a significant premium to where their stocks are trading.

That will mean less equity dilution at the time of conversion. Wayfair’s deal sets a 43% premium above the stock price while Outfront’s had a premium of about 39%, filings show. Outfront Media didn’t immediately respond to requests for comment.