Extraordinary circumstances require global fiscal and monetary co-ordination, QNB has said referring to the economic fallout from the global spread of Covid-19.

“We are all Keynesians now.” That was “notoriously stressed” by US president Richard Nixon in 1971, months before engineering the end of dollar convertibility into gold and launching fresh new measures of price controls and tariffs, QNB said in an economic commentary.

The famous quote, referring to John Maynard Keynes’ prescriptions of government intervention to stimulate demand during cyclical downturns, is a testament to the central role of employment levels in determining the perceived performance of elected officials.

Whenever an economic crisis threatens to disturb the labour market, creating unemployment, even fiscal conservatives such as Nixon turn to “big government’, it said.

This time is no different, except, perhaps, for the magnitude of the challenge ahead, QNB noted.

The fallout from the global spread of Covid-19 has already produced cascading sudden economic stops that disrupted financial markets in record speed, triggering negative feed-back loops.

As governments around the world respond to the health crisis with tight social distancing measures and lock downs, businesses suffer with unforeseen economic challenges. It is difficult to turn this story around before Covid-19 is properly contained. Thus, in order to avoid a more persistent impairment on the balance sheets of both companies and households, governments are off to the rescue.

But the options to handle the crisis are limited as the policy ammunition was partially exhausted in recent years.

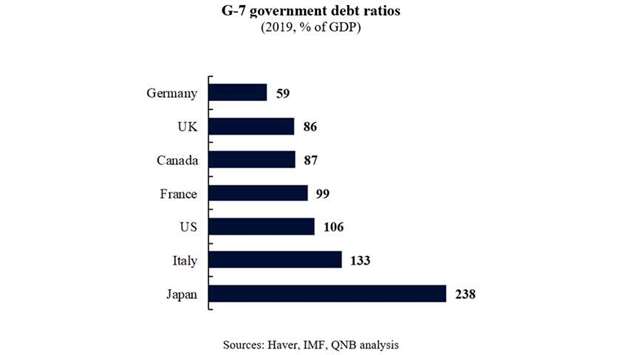

Despite significant deficits in most of the major economies and high public debt in all G7 countries except for Germany, fiscal policy is the natural choice to counter the economic consequences of Covid-19.

QNB analysis delves into the three reasons why fiscal policy is key for the G7 countries over the next quarters.

First, as policy rates are already at or close to the effective lower bound (zero or slightly negative), monetary authorities have come to the end of their tools to stimulate the economy. While central bank action is still key to providing liquidity to the system and partially unclog monetary transmission channels, it cannot provide the traction to stimulate the real economy through rate cuts.

The same logic applies for quantitative easing (QE), given that long-dated yields from government papers are also at record lows if not already at or close to or even below zero. In other words, traditional monetary policy tools are currently ineffective to respond to a deep economic downturn.

Second, fiscal policy tools are more appropriate to provide the relief that companies and households need at this juncture. This includes a wide array of measures such as paid sick leave for the vulnerable, extension of unemployment benefits, additional funding for direct transfers, subsidised loans to small and medium enterprises, coverage of health costs for the uninsured, transfer of funds for healthcare services, and tax holidays.

In different shapes and forms, G7 governments have already announced measures like that. As the crisis deepens, there is much more to come, but fiscal policy room is also limited by high debt levels and subdued demand for low-yielding papers.

Third, despite existing structural deficits and high debt levels, there are unorthodox mechanisms to be deployed in such extraordinary circumstances. A massive increase in budget deficits (more than 10% of GDP) would normally produce large spikes in bond yields, tightening financial conditions.

This would be detrimental to the highly leveraged corporate and government sectors, increasing the overall global debt burden. As a response, economic authorities can enact fiscal-monetary coordination, i.e., intervention of central banks to hold interest rates down during a fiscal expansion (debt monetisation with central bank financing of government deficits), QNB said.

In contrast to QE, in which central banks buy government papers from private agents in the secondary market, fiscal-monetary co-ordination would allow central banks to directly purchase newly issued government debt on the primary market.

With the central bank operating in the primary government debt market, a massive supply of bonds can be accommodated with no pressure on yields. This can temporarily create additional fiscal space to tackle emergencies.

“We believe the current crisis requires extraordinary fiscal measures. In fact, during deep downturns in aggregate demand, debt monetisation can be key in quickly reestablishing global economic activity to pre-Covid-19 levels. However, it should be made clear that extreme deficits and fiscal-monetary co-ordination are meant to be temporary,” QNB said.

There is a risk that such measures would empower existing “fiscal populists” in demanding ever more spending in generous entitlements and other government programmes. Over the medium term, such policies can be conducive to fiscal dominance, ie, a condition that generally involves debt monetisation with un-tamed inflation and financial repression.

Moreover, an orderly round of fiscal-monetary co-ordination in all major economies would require strong global co-operation. In the current absence of G7 or G20 co-ordination, or even deeper support for existing international financial institutions, synchronised debt monetisation will potentially disrupt foreign exchange (FX) markets.

Disorderly capital flows and FX pressures can dent the effectiveness of fiscal-monetary co-ordination. Therefore, in order to assure policy success on the national level, mechanisms for global economic governance need to be reformed and strengthened, QNB noted.