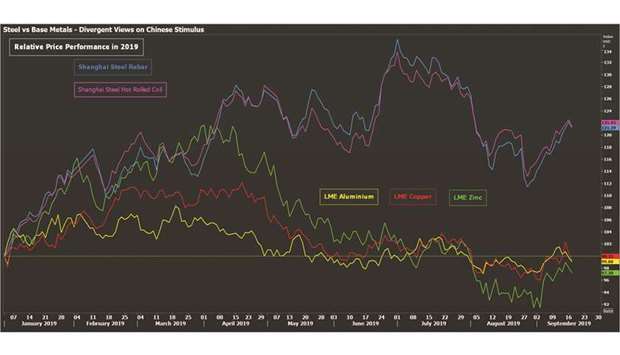

Industrial metals have fallen into two very distinct camps over the course of 2019. In the one corner is the ferrous complex.

The Shanghai Futures Exchange’s (ShFE) steel rebar and hot-rolled coil contracts are both showing year-to-date gains of over 21%. In the other corner are the base metals traded on the London Metal Exchange (LME). Copper, the metal with an honorary degree in economics, is now trading flat relative to the start of January.

So too are other core LME contracts such as aluminium and zinc. Nickel is the sole exception, partly because of its own bullish supply story and partly because Chinese speculators tend to trade it as a quasi steel derivative.

The divergence in performance represents two differing views on the current state of play in China, the world’s industrial engine room. Steel’s reaction to last Monday’s release of a disappointing set of Chinese macroeconomic indicators was instructive. Headline industrial growth weakened to 4.4% in August relative to last year, the slowest pace since February 2002.

Fixed asset investment growth slowed to 5.5% in January-August from 5.7% in January-July, while retail sales growth also eased with the automotive sector remaining a key point of weakness. Yet Shanghai steel rebar and hot-rolled coil futures both jumped on the news, the latter hitting a one-and-a-half month peak.

Chinese steel markets are, as my colleague Clyde Russell has pointed out, taking a “bad news is good news” view of China. The weaker the data, the argument runs, the greater the incentive for Beijing to do something about it in the form of more steel-intensive infrastructure and property investment.

This is what happened during China’s industrial slowdown in 2015-2016 and more spectacularly in the period immediately following the 2008-2009 Global Financial Crisis.

It also reflects the fact that steel has already benefited from the current round of stimulus with Chinese production running red hot, up 9.1% over the first eight months of the year, but exports falling by 4.4%. The implied strength of domestic demand means Chinese steel markets are sufficiently insulated from the Sino-US trade dispute that it can be neatly folded into the “bad news is good news” trade.

Base metals, on the other hand, seem to taking the opposite view that bad news really is bad news.

LME copper, for example, fell sharply on slew of Chinese data. Expectations about the demand boost from Beijing’s current stimulus package are low because base metals haven’t yet seen the sort of tangible impact experienced by steel markets.

Investment in the power grid, arguably the single biggest driver of copper demand in China, has risen by a negligible 0.4% so far this year.

Railway investment, another key sector for copper, has recovered from last year’s contraction but growth rates have been slowing since March. There should, in theory, be some positive knock-on from strength in the property sector as new builds, positive for steel, translate into more completions, positive for base metals.

But copper’s underperformance relative to steel tells you base metals think the current round of stimulus is “metals-lite” and will remain so even if Beijing unleashes more of it. That also leaves them more worried about the broader downturn in the global industrial economy and the potential further negative impact from any escalation of the China-US tensions.

Although rooted in the divergent impact so far of Chinese stimulus, the split between ferrous and nonferrous markets is also a reflection of differing views between Chinese and international players.

Shanghai’s two steel contracts largely reflect domestic market conditions and therefore domestic views as to what will happen next. Chinese speculators are firmly in the “bad news is good news” camp, drawing on the experiences of the past two stimulus cycles to stay positive on steel market dynamics.

They are also reluctant to turn too negative on the base metals complex for the same reason.

The lack of speculative interest in the ShFE copper contract is noticeable with volumes and open interest decidedly humdrum. The same holds true across other ShFE base contracts, again with the exception of nickel, which has sucked in lots of hot money on its recent super-charged rally.

Outside of China, however, funds seem overwhelmingly negative on the industrial metals with nickel the only exception.

Money managers have trimmed their collective short position on the CME copper contract over the last week but only marginally so. It stood at 51,459 contracts as of last Tuesday, still a massive bear bet by historical standards.

On the London market funds were short copper, aluminium, zinc and tin and were neutral lead as of last Thursday, according to LME broker Marex Spectron.

* Andy Home is a columnist for Reuters. The views expressed are those of the author.