Buffered by relatively strong external positions, the Asean countries are set to outperform other key emerging markets in terms of both growth and overall dynamism, QNB has said in an economic commentary.

With a more dovish US Federal Reserve (Fed) and positive developments in global trade disputes, emerging markets (EM) have benefited from a substantial recovery in risk sentiment. However, recent gains can easily be reversed should major global risks materialise, including resurgence in US-China trade jitters, an unexpected tightening by the Fed or a hard landing in China, QNB said.

New bouts of external pressure on vulnerable EM would be expected to follow any sudden reversal in risk sentiment. In this sense, it is ever more important to track and analyse the leading indicators of external vulnerability in key EM.

QNB analysis delves into external financing requirements and foreign exchange liquidity positions of the four largest economies of the Association of Southeast Asian Nations (Asean) – Indonesia, Thailand, Malaysia and the Philippines – drawing conclusions about their resilience to external shocks.

“Thailand is the best positioned economy of our cohort to weather sudden changes in capital flows,” QNB said.

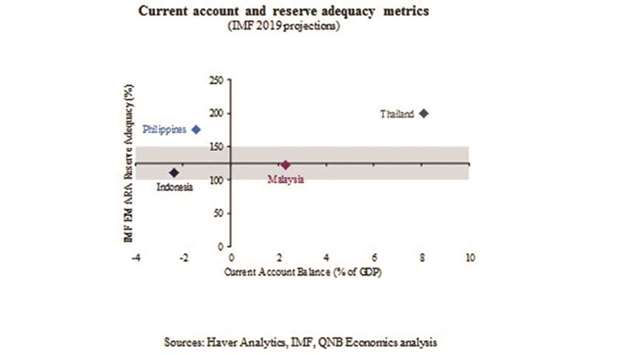

The country runs sizeable current account surpluses as both structural and cyclical factors contribute to push residents to save and non-residents to increase their imports of Thai goods and services, not least for electronics and tourism.

Terms-of-trade have also been supportive in recent years as crude oil prices have trended down from record highs before the 2014 oil price crash. In addition, Thailand has amassed $212bn in official FX reserves, which comfortably covers all relevant reserve adequacy metrics, including with over 11 months of import cover, three years of short-term external debt, 33% of broad money and nearly 200% of the composite IMF’s EM benchmark reserve adequacy ratio (IMF EM ARA metric).

FX reserves are traditionally considered within adequate levels whenever they range above three months of imports, one year of short-term external debt, 20% of broad money and 100-150% of the ‘IMF EM ARA’ metric.

Malaysia is another country in which residents are net lenders to the rest of the world. The country also runs persistent current account surpluses, albeit not quite as pronounced as in Thailand and gradually declining since 2011.

A net oil and commodity exporter, Malaysia has been “negatively affected by structural changes” in the oil industry and more volatility in commodity markets.

Despite current account surpluses, non-residents hold an important share of Malaysia’s government and central bonds (about 22% of total outstanding), exposing the country to capital flows.

Importantly, reserve adequacy metrics are much tighter than for Thailand, with the central bank holding $102bn in total official FX reserves. This is an adequate level as it accounts for nearly five months of import cover, one year of short-term external debt, 22% of broad money and around 120% of the ‘IMF EM ARA’ metric.

The Philippines is a net external borrower, QNB noted. With a large trade deficit that is currently only partially offset by sizeable inflows of remittances from the community of Philippine expatriate workers, the country runs a current account deficit that amounts to close to 1.5% of GDP.

However, the deficits are mostly driven by a healthy push for much needed investment, and monetary authorities have ample FX reserves. In fact, official reserves amount to $82bn and hover around nine months of import cover, six years of short-term external debt, 40% of broad money and around 175% of the IMF EM ARA metric.

Indonesia is the significant Asean economy most exposed to volatile capital flows. The country runs persistent current account deficits on the back of both fiscal imbalances and net external borrowings from the non-financial corporate sector. The current account deficit has been widening recently from 0.9% of GDP by the end of 2016 to 3.6% of GDP by the end of last year.

In addition, sensitivity to international capital flows are amplified by a significant currency mismatch, i.e., the fact that a large share of the debt from the public and corporate sectors is denominated in USD, even though most of their revenues or earnings are in local currency.

On a more positive note, while not as ample as other Asean countries, Indonesian official FX reserves amount to $120bn, also fulfilling the adequate criteria with seven months of import cover, two years of short-term external debt, 30% of broad money and around 110% of the ‘IMF ARA’ metric.

“All in all, large Asean economies are relatively resilient to sudden changes in risk sentiment and capital flows. Such resiliency is a major source of support in a context of higher global uncertainty,” QNB said.