The effects of weakening demand in large advanced and emerging economies (US, EU, Japan, and China) are spilling over to other corners of the globe, QNB has said in an economic commentary.

Despite positive developments in US-China trade negotiations and supportive communication from the US Federal Reserve, small open economies in Asia have been struggling.

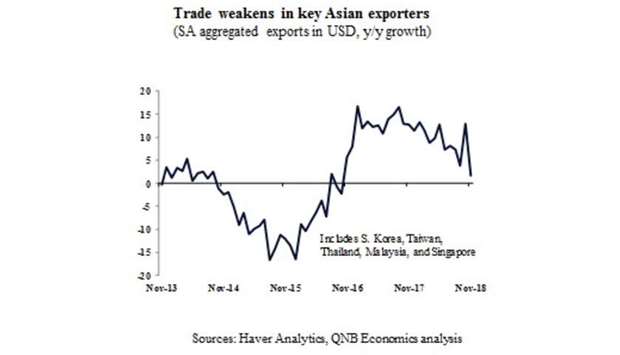

QNB analysis delves into the main reasons behind sluggish data coming from key Asian exporters, namely South Korea, Taiwan, Thailand, Malaysia, and Singapore, referred to here in aggregate as ‘key Asian exporters.’

Higher frequency data in key Asian exporters is pointing to further weakness in global and regional growth. Over the last months, business surveys and export data have been trending down in the Asian region, QNB said.

Manufacturing Purchaser Managers’ Indices (PMIs) are down by a range of 1.5-4.7 in all key Asian exporters except for Thailand, where the manufacturing PMI has been roughly stable at around the neutral 50 level.

Worryingly, only Singapore presents manufacturing PMI data hovering on expansion territory (above 50), even if its latest 51.1 reading is very far from striking.

Exports are also on a decreasing trend in our cohort of countries, with export growth slowing to 1.9% year-on-year (y-o-y) in November 2018 from several consecutive months of two digit y-o-y growth.

The momentum is expected to worsen as South Korea and Taiwan, early reporters for trade data, have seen their overall exports contract by respectively 1.2% and 2.6% y-o-y in December 2018.

Four reasons are contributing to the poorer performance in key Asian exporters, QNB noted.

First, led by the US, EU, Japan and China, global growth is slowing. Importantly, the US economy, boosted in 2018 by a sugar rush of fiscal stimula, is gradually moderating as financial conditions tighten and the fiscal impulse wears off.

Highly dependent on exports and external demand, key Asian exporters tend to move in sync with the global economy.

Second, trade relations of key Asian exporters with China are worsening. This outlook is driven by uncertainties over the performance of the Chinese export sector but also by the overall slowing domestic demand across different metrics (retail sales/ transport/ cargo and freight/ rents/ credit growth/ PMI, etc.).

Until late last year, trade frictions were mostly affecting the global economy through the indirect channel of fixed asset investments and inventories, as capital expenditures were cut back or delayed due to a gloomy outlook.

However, QNB said there was new evidence that direct trade was now more on the line. After holding up for several months, China’s exports to the US have declined by 3.8% y-o-y in December 2018. This may be reflecting the waning of the so-called front-loading effect in US-China trade, i.e., US based companies increasing imports from China to stock up before new tariffs come into effect. As key Asian exporters are major suppliers to China’s export sector, this is already slowing intra-regional trade.

In fact, seasonally adjusted total exports of QNB’s cohort to China contracted by 4.3% y-o-y in November 2018, the first contraction in more than two years. Figures are expected to deteriorate further over the coming months as early reporters (South Korea and Taiwan) have presented an even more significant export contraction to China of 12.6% y-o-y in December 2018.

Third, trade impacts of FX movements are weighing on overall exports from Asia. As QNB’s Asian exporters price and invoice a significant amount of their exports in dollar irrespective of their current FX rates, exogenous USD appreciation dampens demand for exports from those countries.

In this sense, the slowdown in exports from Asia is partially explained by the dollar appreciation against the currencies of major importers since April 2018.

Fourth, microeconomic idyosincratic factors coming from South Korea are also dragging on growth. The end of the boom in South Korea’s dominated semi-conductor industry is slowing the memory chip cycle, affecting regional activity and trade.

After a strong pick up since mid-2016, the sector is set to slow as supply increases and inventories ramp up. This is reflected in the recent profit warnings from Samsung as well as weaker intra-regional imports of semi-conductors and global exports of mobile devices.

South Korean exports accounted for more than 30% of total exports of key Asian exporters, and memory exports represented more than 20% of total South Korean exports in 2018. In addition, memory exports or exports from the semi-conductor industry accounted for more than 90% of export growth in South Korea last year, QNB said.

“In short, worsening global conditions are manifesting themselves even with the traditionally resilient key Asian exporters. Higher frequency data suggests that the global economy is losing further momentum, and risks to the Bloomberg consensus forecasts of 3.5% y-o-y global growth this year are tilted towards the downside,” QNB said.

ends

Despite positive developments in US-China trade negotiations and supportive communication from the US Federal Reserve, small open economies in Asia have been struggling.

QNB analysis delves into the main reasons behind sluggish data coming from key Asian exporters, namely South Korea, Taiwan, Thailand, Malaysia, and Singapore, referred to here in aggregate as ‘key Asian exporters.’

Higher frequency data in key Asian exporters is pointing to further weakness in global and regional growth. Over the last months, business surveys and export data have been trending down in the Asian region, QNB said.

Manufacturing Purchaser Managers’ Indices (PMIs) are down by a range of 1.5-4.7 in all key Asian exporters except for Thailand, where the manufacturing PMI has been roughly stable at around the neutral 50 level.

Worryingly, only Singapore presents manufacturing PMI data hovering on expansion territory (above 50), even if its latest 51.1 reading is very far from striking.

Exports are also on a decreasing trend in our cohort of countries, with export growth slowing to 1.9% year-on-year (y-o-y) in November 2018 from several consecutive months of two digit y-o-y growth.

The momentum is expected to worsen as South Korea and Taiwan, early reporters for trade data, have seen their overall exports contract by respectively 1.2% and 2.6% y-o-y in December 2018.

Four reasons are contributing to the poorer performance in key Asian exporters, QNB noted.

First, led by the US, EU, Japan and China, global growth is slowing. Importantly, the US economy, boosted in 2018 by a sugar rush of fiscal stimula, is gradually moderating as financial conditions tighten and the fiscal impulse wears off.

Highly dependent on exports and external demand, key Asian exporters tend to move in sync with the global economy.

Second, trade relations of key Asian exporters with China are worsening. This outlook is driven by uncertainties over the performance of the Chinese export sector but also by the overall slowing domestic demand across different metrics (retail sales/ transport/ cargo and freight/ rents/ credit growth/ PMI, etc.).

Until late last year, trade frictions were mostly affecting the global economy through the indirect channel of fixed asset investments and inventories, as capital expenditures were cut back or delayed due to a gloomy outlook.

However, QNB said there was new evidence that direct trade was now more on the line. After holding up for several months, China’s exports to the US have declined by 3.8% y-o-y in December 2018. This may be reflecting the waning of the so-called front-loading effect in US-China trade, i.e., US based companies increasing imports from China to stock up before new tariffs come into effect. As key Asian exporters are major suppliers to China’s export sector, this is already slowing intra-regional trade.

In fact, seasonally adjusted total exports of QNB’s cohort to China contracted by 4.3% y-o-y in November 2018, the first contraction in more than two years. Figures are expected to deteriorate further over the coming months as early reporters (South Korea and Taiwan) have presented an even more significant export contraction to China of 12.6% y-o-y in December 2018.

Third, trade impacts of FX movements are weighing on overall exports from Asia. As QNB’s Asian exporters price and invoice a significant amount of their exports in dollar irrespective of their current FX rates, exogenous USD appreciation dampens demand for exports from those countries.

In this sense, the slowdown in exports from Asia is partially explained by the dollar appreciation against the currencies of major importers since April 2018.

Fourth, microeconomic idyosincratic factors coming from South Korea are also dragging on growth. The end of the boom in South Korea’s dominated semi-conductor industry is slowing the memory chip cycle, affecting regional activity and trade.

After a strong pick up since mid-2016, the sector is set to slow as supply increases and inventories ramp up. This is reflected in the recent profit warnings from Samsung as well as weaker intra-regional imports of semi-conductors and global exports of mobile devices.

South Korean exports accounted for more than 30% of total exports of key Asian exporters, and memory exports represented more than 20% of total South Korean exports in 2018. In addition, memory exports or exports from the semi-conductor industry accounted for more than 90% of export growth in South Korea last year, QNB said.

“In short, worsening global conditions are manifesting themselves even with the traditionally resilient key Asian exporters. Higher frequency data suggests that the global economy is losing further momentum, and risks to the Bloomberg consensus forecasts of 3.5% y-o-y global growth this year are tilted towards the downside,” QNB said.

ends