Hedge funds scaled back some of their short positions in crude oil futures and options after prices failed to fall further, suggesting the market was running out of negative momentum.

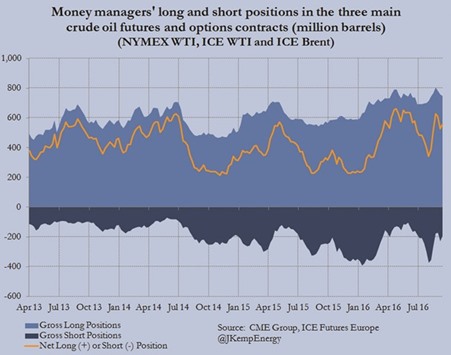

Along with other money managers they cut their combined short position in the three main Brent and WTI contracts by 36mn barrels in the week to September 13.

This partially reversed an increase the previous week of 57mn barrels, according to an analysis of position data published by regulators and exchanges which showed that money managers cut their short positions in WTI by the equivalent of 25mn barrels and in Brent by 11mn barrels.

The fall in bearish short positions came as benchmark prices steadied after dropping sharply since the middle of August.

Brent prices for November dropped just 16 cents between September 6 and September 13, after declining by $1.47 and $1.59 in the two previous weeks.

With the benchmark already down by more than $4 per barrel from the recent high, and not falling any further in the short term, some bearish hedge funds decided to take profits.

By contrast, there were few changes on the long side, and certainly no sign of increased bullishness.

Long positions fell by 8mn barrels in WTI and 3mn barrels in Brent.

The combined impact of these changes is that hedge funds and other money managers increased their net long position in crude futures and options by a modest 26mn barrels to 555mn barrels.

The overall impression is of a market stuck in an uneasy truce after bulls and bears fought each other to a standstill.

Hedge funds boosted their net long position by a record 287mn barrels over just three weeks between August 2 and August 23. The rapid gains produced an almost inevitable reaction with the net long position cut by 99mn barrels over the next two weeks from August 23 to September 6.

Now the reaction has produced its own counter-reaction, with the net long position boosted by 26mn barrels in the week to September 13.

But overall the price and position fluctuations have grown smaller, which suggests the market has been groping towards a new level.

Brent prices are now close to the midpoint ($46.50) of their recent trading range ($41-$52) which is another reason why there is no strongly bullish or bearish tendency.

The oil market has experienced four cycles of hedge fund short-selling since the start of 2015.

The accumulation and liquidation of short positions has corresponded with the fall and rise in prices, especially in the NYMEX WTI contract.

The start and end of these accumulation and liquidation cycles are clearly identifiable in retrospect, but are never so clear cut at the time.

The big increase in hedge fund short positions reported in the week between August 30 and September 6 was a possible signal that a possible fifth short-selling cycle might be underway.

But the reduction in short positions in the week to September 13 suggests the market is probably still in the tail end of the liquidation phase of Cycle 4.

If that proves correct, further short-covering could provide some support for oil prices in the short term, but with short positions already reduced so far, the degree of support is likely to be modest.

*John Kemp is a Reuters market analyst. The views expressed are his own.