Fears of an imminent US rate rise along with higher bond yields in developed markets hit emerging assets yesterday, with the main equity index tumbling 2.5% and currencies weakening against the dollar.

US and German 10-year yields were at the highest in 2-1/2 months, rising further after Friday’s spike caused by speculation the US Federal Reserve could move interest rates this month, instead of December as markets had reckoned.

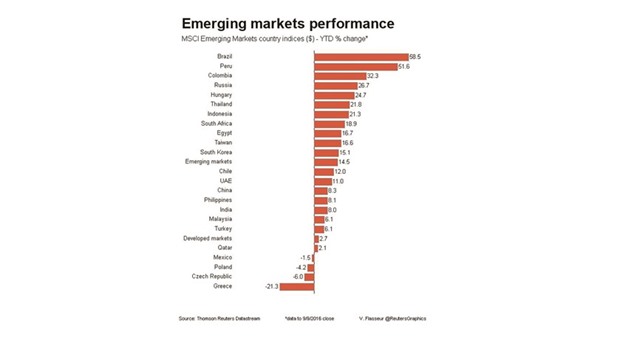

With US stocks falling around 2% on Friday, emerging markets, like other riskier assets, felt the heat.

MSCI’s benchmark emerging equity index hit one-month lows for the biggest daily loss since immediately after the Britain’s referendum vote to leave the European Union. The index fell 1.9% on Friday.

“(Boston Fed President Eric) Rosengren’s comments last week really set this (sell-off) in motion, with his more hawkish comments...and that mood has continued now on Monday,” SEB’s chief emerging markets strategist Per Hammarlund said, adding however he saw the current moves as a “blip”.

He expects other Fed speakers to quash the hawkish tone, adding: “I think the data is a bit too weak and too unconvincing for them to already hike in September.”

Hammarlund said markets also were rattled by a rise in Chinese overnight rates on offshore yuan to seven-month highs.

Speculation has grown of a liquidity squeeze to control yuan depreciation via offshore markets.

“(The PBoC) is trying to make offshore yuan funding more expensive, driving up forwards quite sharply and I suspect that will eventually squeeze out some long-dollar yuan forwards, but for now it is touching off a bit of a risk-off mood,” he added.

While onshore-traded yuan was supported by reports of dollar sales by state-run banks, local stocks fell around 2% while Hong Kong listed H-shares slumped 3.4% for their biggest one-day fall since February.

Emerging markets appear all the more vulnerable to a shift in Fed expectations, given emerging debt and equity funds have received bumper inflows in recent months

Bonds came under pressure, with yields on South Africa’s benchmark, one of the most liquid in emerging markets, now almost 20 basis points higher than Thursday’s close and Russian 10-year yields up about 24 bps.

Yields on JPMorgan’s GBI-EM local debt index rose around 7 basis points on Friday and dollar bond yield spreads over Treasuries at a five-day high.

On currency markets, the South African rand and Turkish lira weakened close to 1% to the dollar while oil’s 1% fall drove the rouble 0.6% lower

BNP Paribas analysts predicted any shakeout would be far smaller than the 2013 ‘taper tantrum’.

“Although a September rate hike would trigger a correction in EM, we continue to think that the eventual impact on EM assets will be manageable, as we expect the Fed to indicate a modest upward trajectory for interest rates,” they added.

In central Europe, the Hungarian forint slipped 0.4% to three week lows to the euro while the Czech crown strengthened further in forward markets amid expectations the currency’s 27-per-euro exchange rate cap will be scrapped.

Six-month euro/crown forwards fell 7% but stayed off record lows hit on Friday.

The forwards are pricing the crown well above its current 27 per euro rate where the central bank is holding it.

“They pledged to keep it until 2017 — but they have all good reasons to drop the floor earlier,” Hammarlund said.”One is that the economy is red hot...The second thing is they are accumulating reserves and the longer they wait, the more of an FX loss they are going to do on the reserves.”

Croatia’s kuna was flat after the conservative HDZ looked set to win parliamentary elections.