In a drug sector awash with cash, even US government moves to call time on an acquisition boom aren’t dousing hopes for more takeover deals as companies look to expand.

The US Treasury set out regulations this week to curb tax-avoiding corporate “inversions”, resulting in the collapse of Pfizer’s agreed deal to buy Allergan for $160bn.

While the move was aimed at deals in which companies move abroad to cut tax, European drug stocks responded positively. Traders said the regulations seemed targeted at the Pfizer-Allergan and cash-rich pharma firms would look to consolidate elsewhere.

European drug stocks have benefited from M&A activity in the sector, which hit records in 2015. And investors see valuations could be further inflated if more deal-making is on the horizon.

“Because there is so much cash in the sector, other companies in the sector are becoming a target,” said BNP Paribas equity and derivative strategist Ankit Gheedia, estimating companies in the MSCI World Healthcare sector held cash equating to about 9% of their total market value.

Cash levels in the sector have been running at near highest-ever levels for three years, Gheedia said.

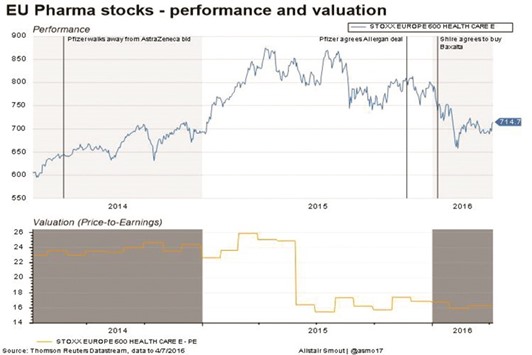

While valuations have been supported by merger activity, they have come down from the peaks seen a year or two ago. So that while not cheap, the sector is not too expensive for those betting on more deals. AstraZeneca, which rose after the Pfizer-Allergan deal collapsed, trades at 15 times prospective earnings, having traded as high as 18 in early 2014, around the time that Pfizer was looking to by the UK-listed drugmaker.

Another stock to bounce this week was Shire, on 13.7 times prospective earnings, below a 10-year median of 16.7 times and as much as 25 in 2014. The stock has fallen more than 20% over the last year, as some investors worried over its costly deal to buy US peer Baxalta.

Exane BNP Paribas analyst David Finch added Shire to its M&A Target list, noting: “Big Pharma in general has other reasons than tax efficiency to make big acquisitions.”

He cites Shire’s cheap valuation, as well as favourable forex conditions and the unsustainability of share buybacks, as contributing to the case for Pfizer to bid for Shire. And even if Shire resists an approach, the stock’s valuation meant that: “Deal or no deal, we think we will make money.”

Of course, a new M&A splurge in 2016 could hit a roadblock if regulators are equally keen to crack down on other deals as they were to derail Pfizer-Allergan. The sector had its biggest deal-making streak in history last year, even setting aside the failed deal from the $673bn total for 2015, according to Thomson Reuters data.

A similarly performance will be hard to replicate if other deals are blocked, and some believe the risks of these deals going wrong is reason enough for large companies to avoid big-ticket manoeuvres.

“Pfizer have had two big, failed deals, and I think they’re going to pull back a bit. They’ve just paidmns of dollars in break fees to Allergan,” said Jupiter Global Managed Fund manager Stephen Mitchell.

“It’s very expensive stuff to get wrong. The M&A I would expect is more bolt-on M&A, filling in specific areas in the portfolio,” Mitchell added. Yet some analysts say other situations, such as Shire’s deal to buy Baxalta, should not be impacted by the new rules.

Julien Jarmoszko, European equity research manager at S&P Global Market Intelligence, said cheap funding would encourage M&A, with companies such as France’s Sanofi looking to enhance earnings that way.

“As long as your target is cash generative, you get earnings enhancements, because you’re given free money to target a company which is making money,” Jarmoszko said.

BNP Paribas’s Gheedia said M&A is one of the 10 reasons why he likes the sector, with good growth prospects thanks to expanding health care spending in emerging markets also positive. But still, “M&A is the cherry on the cake”.