After three years of negative returns in emerging market currencies and local bonds, and at least as many false dawns, some investors are punting again on a turning point – this time hopeful of a downturn in the dominant US dollar.

Dollar-based investors suffered an average 15% losses last year on bonds denominated in currencies such as Turkish lira and Mexican peso, and sector funds tracked by the EPFR Global consultancy witnessed $12.6bn in capital outflows – the third straight year of losses.

But some say that even if the outlook for emerging economies is precarious, local-currency bonds are now attractive. Already this year, emerging currency debt has returned 4% in dollar terms, comparable to German and US government bonds but well above most other mainstream asset classes, this chart shows:

BlackRock, the world’s largest asset manager, predicts domestically issued debt will deliver double-digit returns in 2016, as external headwinds start to ease. And the main gale has been a worldwide revaluation of the US dollar of more than 25% against major developed country currencies, with gains against many emerging currencies amounting to as much as 30-60%.

For investors in emerging currency bonds that meant heavy losses in dollar terms wiped out gains on yield.

This year, as recession fears raged in January and early February and US interest rate rises fell off the horizon, the dollar backed off and forecasters started to rethink.

Like most investors, BlackRock’s head of emerging fixed income, Sergio Trigo Paz, spent three years sheltering in the relative safety of emerging market bonds denominated in hard currencies such as the dollar or the euro, but he recently turned bullish on local debt for the first time in three years.

“We expect double-digit returns so...we are very overweight. The more things go our way, the more we shall add (to positions),” Trigo Paz said.

Predicting a dollar pullback, he added: “If you talk of a one-third (dollar) retracement, we talk of 7%. So in emerging local debt you get to clip your coupon of 7%, plus another 7% on EM currencies if you get a dollar depreciation of 7% across the board.” There may also be support from steadier commodity prices, Trigo Paz argues, noting exporting nations have shown willingness to act to prevent further crude price falls.

If dollar risks are indeed neutralised, investor focus should turn again to emerging market yields. That’s especially so because around $6tn worth of global bonds carry negative yields and interest rates in a swathe of developed countries are below zero.

Average yield premia offered by emerging local bonds over US, eurozone and Japanese government debt is around 5.4, 7.2 and 7.1 percentage points, according to Salman Ahmed, chief global strategist at Lombard Odier, who is advising investors to reconsider emerging markets.

The premium paid in 2012 was much lower at 4.5, 4.7 and 5.3 percentage points respectively, he estimates.

Finally, steadier currencies should allow some central banks to cut interest rates - Indonesia, India and South Korea are among those likely to soon ease policy. Russian 10-year yields have fallen 100 bps in the past month as oil prices stabilised.

But the emerging world still faces formidable challenges. Recent business activity data showed recovery remains elusive for most economies; exports and domestic demand are sluggish and the population’s hardships are hampering governments from implementing vital reforms.

There are also question marks over China, which many fear will be forced to devalue its yuan, in turn dragging down other emerging currencies.

So despite the lure of 7% yields, Steve Ellis, portfolio manager at Fidelity International, still prefers emerging dollar bonds, citing high currency volatility on the local debt sector.

“We’ve had times before when we thought it was a good time to go into emerging local currency, we thought there were green shoots but they were false dawns,” Ellis said.

“You need to see the growth backdrop improving, that will give you the green light.”

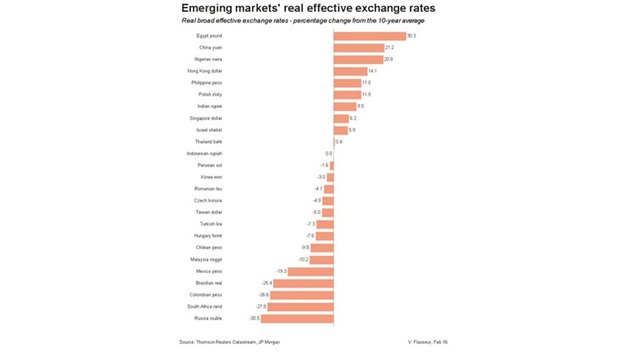

What’s more, with the US industrial sector showing signs of a bounceback and labour markets increasingly tight, Fed hikes have returned to the agenda and the dollar may yet have sting in the tail. For the faithful, emerging currencies are undoubtedly cheap on historical comparisons - the rouble and Brazilian real for instance are 25-30% below their own long-term averages against trade partners’ currencies and adjusted for inflation.