Positive global economic growth prospects and a possible improvement in oil prices are among the factors that QNB Financial Services has taken into account in forecasting a “decent” 6.5% increase in aggregate earnings by key Qatari equities in 2016.

“We have compiled net income expectations of key Qatari equities that we cover. Factors that can positively reinforce our thesis includes but not limited to improvement in oil prices, positive global economic growth prospects, easing of regional geopolitical issues and better than expected earnings from stocks under coverage,” QNBFS said.

However, QNBFS has listed some key risks, which included depressed oil prices, increase in volatility, and exit of hot money from emerging and frontier markets.

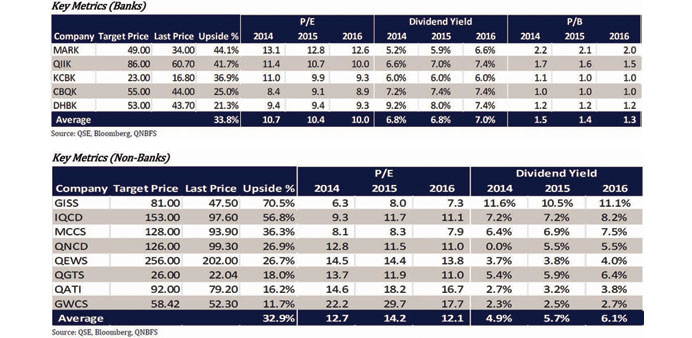

QNBFS said it remained “optimistic” on the Qatari equity market in the long term. “We believe the significant sell-offs driven by declining oil prices have been overdone and consider most of our equities under coverage as attractive opportunities. On an average basis, the 17 Qatari equities we cover imply a long-term upside of 26% to our price targets. Dividend yields remain strong with stocks under coverage expected to yield 5.6% and 5.9% in 2015 and 2016, respectively.

“Valuations continue to be attractive with most companies trading at compelling price-to-earnings multiples along with the best dividend yields in the region. On an overall basis, the Qatar Exchange index trades at a 2016 P/E of 10.4x complemented by a dividend yield of 5.6%, while the Bloomberg GCC 200 Index trades at 10.8x 2016 P/E along with a 2016 dividend yield of 4.9%.”

The QSE’s benchmark Qatar Index has corrected by 32.8% (27.5% annualised) to 9,643.65 as of December 13 from its all-time high of 14,350.5 on September 18 last year.

Like any other market, the Qatar Index experienced regular troughs and peaks. “As such, we revisit past periods of significant movements when the Index corrected and subsequently followed through with a major rally,” QNB said.

For instance, the index dropped by 54.8% (48.2% annualised) and by 66.5% (77.8% annualised) between 2005-2006 and 2008-2009, respectively. Consequently, the index gained 112.4% (88.5% annualised) and 118.5% (51.8% annualised) during 2007-2008 and 2008-2011, respectively.

“Having said that, we can expect history to repeat itself,” QNBFS said.

Quoting QNB, QNBFS said Qatar’s economy is expected to remain “resilient” to lower oil prices.

Qatar is “well-positioned to withstand lower oil prices” thanks to its strong macroeconomic fundamentals including a relatively low fiscal breakeven oil price ($60.7 in 2015), the accumulation of significant savings from the past and low levels of public debt.

QNB has forecast Qatar’s real GDP growth would accelerate from 4% in 2014 to 4.7% in 2015 and 6.4% in both 2016 and 2017, as the government expands its investment spending program in the non-hydrocarbon sector.

The non-hydrocarbon sector is projected to remain the engine of growth in the economy. Its near double-digit expected growth is underlined by strong investment spending in line with the Qatar National Vision 2030. QNB Group anticipates non-hydrocarbon GDP growth at 10.4% in 2015, followed by 9.9% in 2016 and 10% in 2017, it said.