Market calm shows acceptance for monetary divergence; weaker euro is double-blessing to ECB, but for how long?; little spill-over seen on eurozone yields

Reuters

Frankfurt

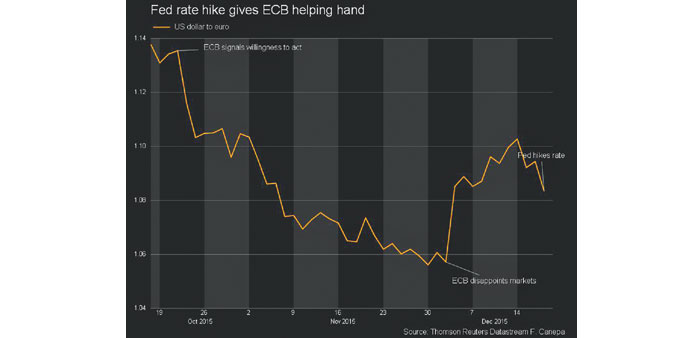

Just weeks after disappointing investors with smaller-than-expected stimulus, the European Central Bank has got a helping hand from the Federal Reserve with a US rate hike that could limit the need for further action of its own.

The Fed and the ECB are moving in opposite policy directions as the US economy strengthens while Europe struggles with tepid growth, high unemployment and anaemic inflation far from the ECB’s target despite its best efforts so far to boost it.

The US hike, the first in almost a decade, immediately started weakening the euro - a move which if prolonged would be a double-blessing for the ECB as it boosted the currency zone’s exporters while simultaneously helping to kickstart inflation.

More importantly, the calm market reaction to Wednesday’s hike suggests investors accept divergence between the world’s top two central banks, allowing the ECB to hold a steady course.

“The ECB will to some extent be able to decouple financing conditions in the euro area from the US,” Dirk Schumacher, senior European economist at Goldman Sachs, said. “The divergence story will stay with us.”

The ECB extended quantitative easing two weeks ago to prop up growth. But its move to shave 10 basis points off the deposit rate and extend but not substantially expand bond-buying was far less ambitious than expected, disappointing markets and pushing the euro more than 3% higher on the day.

Some of that is already being reversed, with the euro weakening around 1% since the Fed decision. Government bond yields of euro zone members like Germany, France, and Italy, which had risen after the ECB decision, edged down 6-8 basis points for 10-year paper on the back of the Fed’s move.

That was seen by some as a thumbs-up to the Fed and fixing what some investors saw as a misstep by the ECB: Rising US rates could in theory have raised European borrowing costs so a counter-intuitive yield fall suggests ECB policy is increasingly detached from the Fed.

“We are not seeing any spillover of the US monetary policy in Europe and we will likely not see it because the rate hike was fully priced in,” Marco Brancolini, RBS European rates strategist, said.

“More importantly, euro rates are driven by US rates only in the very short term. In the long term, 10-year Bund levels depend on ... (ECB) monetary policy.”

Danske Bank predicted only a ‘slight upward pressure’ on eurozone debt yields in the coming six to 12 months.

Others noted that this disconnect would allow the euro to fall further against the dollar.

“There is the potential for a further devaluation in the euro and that’s the best thing that can happen to the eurozone,” Peter Bofinger, one of the ‘wise men’ that advise the German government on economic policy.

Although the ECB has repeatedly said it was ready to ease policy further if necessary, analysts polled by Reuters only see a 40% chance of further action next year.

Indeed, with growth picking up and the euro staying weak or getting weaker, the need for more action could also decrease.

“While the interest rate change doesn’t make any difference economically, it has a big psychological impact,” said Bofinger.

“If the euro starts to slip, the fall can happen fast - there is no speed limit for devaluations.”

That said, the picture for the ECB becomes more mixed further out. If a weaker euro remains a key tool for it to boost inflation, that lever could also be compromised as growth in the euro zone gradually starts to improve. The ECB predicted more solid growth over the next two years yesterday while German manufacturers reported solid demand this week, suggesting security fears and a China slowdown have not dented recovery. Consumer demand is also buoyant.

Moreover the smooth way in which Fed chief Janet Yellen massaged market expectations before Wednesday’s move only highlighted the failure of ECB president Mario Draghi to do the same only a few weeks earlier.

“It is now more difficult for Mario Draghi to talk the euro down. In general, everybody knows we are able to do more if needed. But they also know we didn’t do as much last time as some had wanted,” one ECB source acknowledged.