John Kemp is a Reuters market analyst. The views expressed are his own.

By John Kemp

London

Rather than taking profits, hedge funds continued to add to their record bearish positions after the Organisation of the Petroleum Exporting Countries (Opec) failed to reach agreement on a production target at the start of the month.

By December 8, hedge funds and other money managers had accumulated short positions in the main WTI and Brent futures and options contracts equivalent to 364mn barrels.

The combined short position in Brent and WTI was up by almost 5mn barrels compared with the previous week and 161mn barrels since the middle of October.

The combined short position is easily the largest on record, dwarfing the previous records of 325mn barrels set in August and 299mn barrels in March.

Hedge funds booked some profits on Brent, reducing short positions by 8mn barrels last week, but added 13mn in WTI, according to data from the US Commodity Futures Trading Commission and ICE Futures Europe.

Hedge fund short positions have been strongly correlated with movements in the price of Brent and WTI throughout 2015, so it comes as no surprise that the extra shorts helped push both markers to new lows.

By the end of the week, both Brent and WTI were trading well below $40 per barrel, at their lowest levels since the depths of the financial crisis and recession in 2008/2009.

There has been no sign of mass short covering among speculators despite the fact that WTI and Brent prices have both fallen almost $12 in less than two months. Both the poor supply-demand fundamentals and momentum trading strategies appear to favour the downside for the time being.

But the risks associated with such a large short position that will need to be covered at some point are clearly rising.

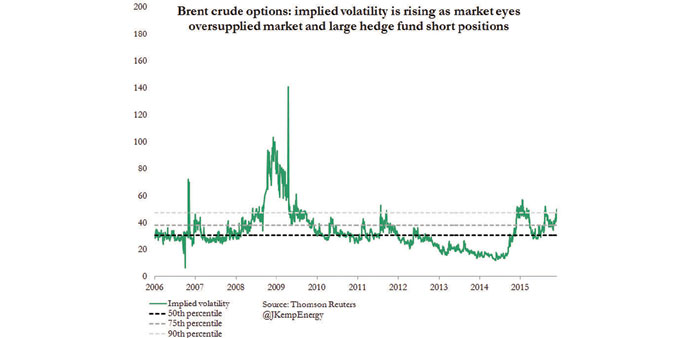

The cost of buying protection against a sudden price movement up or down through options is becoming progressively more expensive.

Brent crude options are now even more expensive than they were before the Opec meeting on December 4 as implied volatility continues to increase.

The implied volatility embedded within one-month at the money Brent options has risen to more than 50%, up from a previous high of 47% before Opec’s decision was announced.

Implied volatility is now the in 93rd%ile for all trading days since 2006, according to estimates derived from Thomson Reuters Eikon. In the short term, the short positions can be rolled forward profitably because the market remains in contango so the hedge funds are buying back cheap futures positions and selling more expensive ones.

Positive roll yield is adding to the returns from being short in a falling market and ensuring the positions are very profitable.

But at some point the short positions will have be scaled back significantly; the high level of implied volatility shows that option dealers are braced for turbulence when some of the hedge funds try to exit.