Doha

The exchange rate peg to the dollar is an “appropriate” policy framework for the GCC as it provides a “stabilisation” of inflation and output growth, QNB has said in a report.

For decades, five countries in the Gulf Cooperation Council (GCC) have kept their currencies pegged to the dollar. Only Kuwait links its currency to a basket, but even this is believed to be heavily weighted towards the dollar. However, the recent sharp decline of oil prices has fuelled speculation in the currency forward markets about possible devaluation of GCC currencies, QNB said.

“These bets are likely to be misplaced for two reasons,” QNB said.

First, the peg makes economic sense given the structure of GCC economies. Second, there is political will and ample resources in the GCC to maintain the peg.

To appreciate the virtues of the peg, QNB said it is instructive to think about what would have happened if the GCC had been running a free-floating exchange rate regime.

Under that scenario, the decline in oil prices would have led to a depreciation of local currencies. This has happened to major oil exporters like Brazil and Russia, whose currencies fell by 71% and 88% respectively against the dollar since mid-2014. Even other oil exporters who are less reliant on oil such as Canada and Norway experienced large depreciations of their currencies (25% and 42% respectively over the same period).

Currency depreciation would have triggered a spike in inflation, given the large share of imported goods and services in the consumers’ basket. International experience confirms this: consumer prices in Brazil and Russia are growing at a double-digit annual rate.

In response, GCC central banks would have increased interest rates to attract foreign capital, limit the depreciation of their currencies and control the rise in inflation.

As a result, growth would have almost surely been negatively impacted. Private consumption would have fallen as elevated inflation would have reduced the purchasing power of consumers and higher interest rates would have made consumption less attractive compared to saving.

Investment would have also declined due to the higher interest rates. And the increased volatility of inflation and exchange rate under the floating regime would have made it difficult to attract foreign labour and capital, which are key drivers of growth in some GCC countries, QNB said.

The thought experiment illustrates the benefits of the current exchange rate regime. But it has been argued that currency depreciation could be helpful in boosting export competitiveness and driving growth. This is a valid argument for economies such as Canada and Norway, but not applicable for the GCC given that most of its exports are hydrocarbons, whose prices are determined internationally and are denominated in dollars.

For example, the depreciation of a GCC currency would not make its barrels of oil more attractive than, say, Russian barrels of oil. Of course, as GCC exports become more diversified, currency depreciation could benefit non-hydrocarbon exports. But while the GCC has managed to diversify the sources of economic growth away from hydrocarbons, the diversification of exports is still lagging.

Given that the fixed exchange rate regime is appropriate for the GCC, the next question is: Is it likely to be maintained?

“We believe the answer is a clear yes for two reasons,” QNB said.

First, there is political will and commitment to maintaining the peg given its economic benefits to consumers and the economy as a whole.

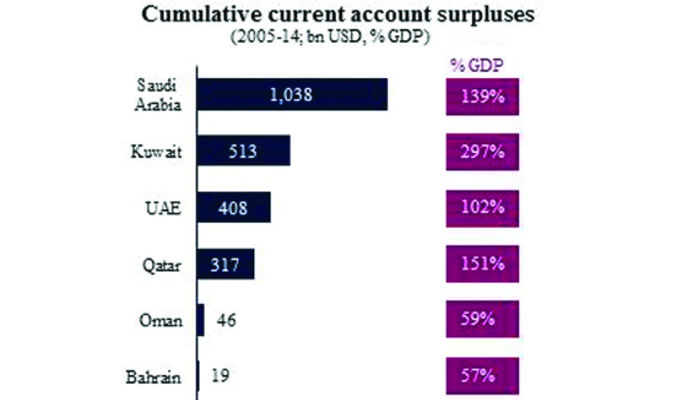

Second, there are ample financial resources to maintain the exchange rate peg. The GCC has accumulated large foreign-currency savings during the last oil boom that can be used to defend the peg.

In many countries, these savings are in excess of 100% of GDP. And while some of these reserves have been used in recent months, they remain sizable and sufficient to defend the peg even if oil prices stay low for a few years.

According to QNB as the GCC moved further down the diversification path, especially with regard to exports, it could benefit from a more flexible exchange rate regime in the future. But until then, there is policy commitment and sufficient resources in the GCC to maintain the exchange rate peg, it said.