Reuters

Hong Kong

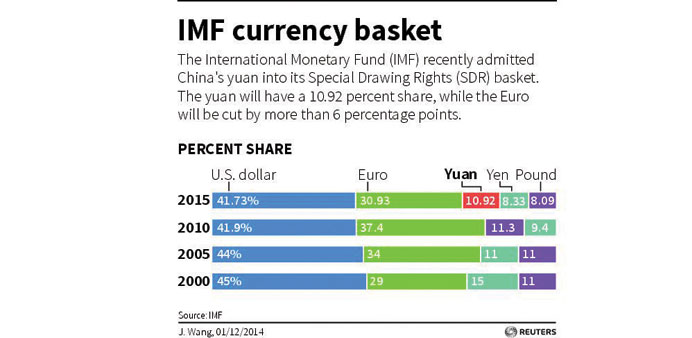

The International Monetary Fund’s decision to add China’s yuan to its reserves basket is a triumph for Beijing, but the fund’s verdict that the currency met its “freely usable” test will have little financial impact unless Beijing recruits more users.

The desire of Chinese reformers to internationalise the currency has a clear economic rationale; a yuan in wide circulation overseas would reduce China’s dependence on the dollar system and on policy set in Washington.

It would also make it easier for Chinese firms to invoice and borrow offshore in yuan, reducing the risk of exchange rate fluctuations and prompting China’s inefficient state-owned banks to improve their performance or lose business.

Those concerned about a potential global liquidity crisis caused by overdependence on the US might also welcome the yuan as an alternative to the dollar, as would countries locked out of dollar capital markets by sanctions.

But to serve these purposes, there needs to be a much bigger pool of yuan outside China, which requires offshore institutions – and not just in Hong Kong – to buy and hold yuan.

Few believe the IMF decision alone, which economist Alicia Garcia-Herrero called a “beauty contest”, will change investor behaviour much.

For that, says Swiss bank UBS, Beijing needs to continue financial reforms and capital account liberalisation to improve the efficiency of capital allocation in China. Foreign investors want Beijing to provide predictable and transparent legal and taxation treatment, and drop its penchant for pilot programmes and quotas in favour of consistency.

They also want to know they can freely sell their yuan assets, not just buy, a concern that only grew over the summer, when Beijing stepped into its stock markets to stop a sell-off. Foreign investors aren’t making full use of the existing channels to buy Chinese assets that Beijing allows - quotas for the two Qualified Foreign Institutional Investor programmes (QFII and RQFII) and the Shanghai-Hong Kong Stock Connect have yet to be used up. And for all the impressive trade statistics, much of the “offshore” yuan isn’t travelling the globe but bouncing to and fro across the internal border with Hong Kong, largely traded between Chinese companies.

“The number one thing we would like to see changed is that the QFII and RQFII quotas are dropped, just as they dropped in July the quotas for central banks, sovereign wealth funds and supernationals. It’ll make it a lot easier for global institutional investors,” said Hayden Briscoe, Director of Asia Pacific Fixed Income at AllianceBernstein in Hong Kong.

Others have called for Beijing to address distortions in its bond market caused by state support for some issuers and patchwork regulatory oversight.

It was little surprise after the summer stock interventions that index compiler MSCI said it was not ready to include yuan-denominated stocks in its indexes, citing reservations expressed by foreign institutional clients like national pension funds.

Central bankers also remain to be convinced and have yet to significantly crank up their yuan reserves.

“Markets in China have yet to evolve further in terms of breadth, depth and institutions,” said a foreign central banker, speaking on condition of anonymity, saying he expects any increase in the offshore yuan pool to happen slowly.

“Once the currency becomes one of the currencies in the basket, I will say, it is a huge responsibility on the part of the government to ensure the currency will be stable, and the economy will be open, to deserve the status of an international reserve currency,” said Ji Liqun, president-designate of the China-led Asian Infrastructure Investment Bank (AIIB), during a press conference yesterday.

But combining openness with stability has been a struggle in 2015. As China has lowered domestic interest rates to support growth, the yuan fell and capital fled.

Instead of opening the capital account to lure foreign investment, Beijing has been closing it to prevent outflows.

So on the same morning China was celebrating the yuan joining the dollar, euro, yen and pound in the IMF basket, the People’s Bank of China took the time during its morning press conference to repeat that there is no basis for the yuan, already down 3% against the dollar so far this year, to decline further.

Both onshore and offshore yuan declined against the dollar in subsequent trade.