By Arno Maierbrugger

Gulf Times Correspondent

Bangkok

The Istanbul-based World Bank Global Islamic Finance Development Center together with the Islamic Development Bank is stepping up its initiatives to include small and medium-sized enterprises (SMEs) in Islamic finance.

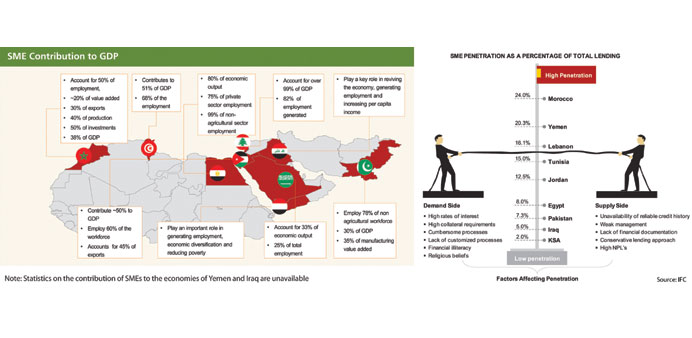

In a recent joint policy paper released during the G20 summit in Turkey this November, called “Leveraging Islamic Finance for SMEs,” the two institutions stated that there was significant “unmet demand” by SMEs for Islamic finance. The study, referring to previous research by the International Finance Corporation, an organisation of the World Bank, points out that there is a potential gap of up to $13.2bn for Islamic financing for SMEs in some key countries in the Middle East and North Africa (Mena).

In detail, a potential gap of $8.6bn to $13.2bn for Islamic SME financing is seen in nine countries in the region, namely Egypt, Iraq, Jordan, Saudi Arabia, Lebanon, Morocco, Pakistan, Tunisia and Yemen. This corresponds with a deposit potential of $9.7bn to $15bn, the study found, therefore identifying “a large untapped potential for Islamic financing in this area. Including more asset-backed financing and removing regulatory and tax impediments to equity-like financing, as well as strengthening financial infrastructure would help penetration in this segment.”

Furthermore, Shariah-compliant SME financing represent only 7% of the total loans in Egypt, whereas the demand for Islamic financial products is about 20%. Saudi Arabia is the country with the least gap between demand (90%) and supply (67%), due to the large number of Islamic banks residing in Saudi Arabia. It is estimated that about 32% of SMEs across the Mena region in addition to Pakistan are totally excluded from access to Islamic financing, mainly because of the lack of Shariah-compliant products. The risk-averse approach of banks and specifically Islamic banks has also led to a narrow product range offered to SMEs in these countries.

But Islamic finance for SME would be a perfect match.

“The asset-backed finance and risk-sharing nature of Islamic financial products aims to contribute to social and economic development through promoting entrepreneurship,” the report points out. Asset-based financing — the mainstay of Islamic finance — ensures that real economic activity is financed. However, equity-based Islamic financing on the other hand would promote profit-and-loss sharing between financiers and entrepreneurs resulting in increased alignment of interests, increased risk sharing and fostering entrepreneurship especially of seed and early-stage startups, which rely purely on equity financing for their ventures.

The World Bank comes to the conclusion that the Islamic SME banking challenge can be met by adequate policy response and also presented a number of recommendations to improve the situation. Among them are obvious demands that are regularly made in discussions on the topic, such as standardisation of Islamic finance regulations and the increase of product offerings, namely towards equity-based Shariah-compliant financing and towards the use of movable collaterals, as well as general improvement of Islamic finance literacy and the capabilities of human resources involved in Islamic finance. But the institution also suggests introducing tax incentives for SME investors through Islamic finance, more digital payment channels including regulated Islamic crowdfunding platforms, branding of Islamic finance as “ethical finance” and the creation of Islamic finance or ethical quality indexes.