Bloomberg/New York

To see why Wall Street analysts were so bullish on Valeant Pharmaceuticals International before its stunning fall, you need to consider just how dangerous it was to be bearish.

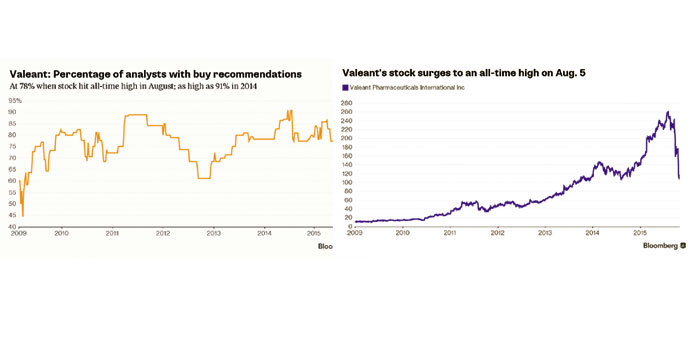

Few have risen so fast, or so relentlessly, in recent years. Built on scores of debt-financed takeovers, Valeant transformed itself from a small biotech valued at $2bn in 2010 into a specialty drug behemoth worth $90bn. That’s made naysaying a futile and costly endeavour. Analysts cut their ratings on the stock 14 times between 2009 and 2014. In the year following each downgrade, Valeant surged 90% on average.

So on Wall Street, where straying from consensus for too long rarely pays, it’s not hard to see why so few people covering Valeant have been bearish. That remains true after accusations of fraud - made by short seller Citron Research - sent Valeant’s shares into a tailspin.

“This is emblematic of how Wall Street works,” according to Lawrence Brown, a professor of accounting at Temple University’s Fox School of Business, who has researched analyst ratings for five decades.

Laurie Little, a spokeswoman for Valeant, didn’t respond to an e-mail seeking comment. In a statement last week, the company said Citron Research’s allegations questioning its sales practices were erroneous and drew false conclusions.

Of the 23 analysts covering it, about 80% called Valeant a buy on August 5, when the shares peaked. Only one, Dimitry Khmelnitsky of Veritas Investment Research Corp of Toronto, considered it a sell, a call that he’s had since July 2014.

“You feel like a fool as the stock price goes up and up,” said the 38-year-old analyst, who told clients to get rid of Valeant shares after he became concerned about its accounting practices. “It really hurts your confidence and how you feel about yourself. But you have to persevere if you believe in your call.”

In the year after Khmelnitsky, a former infantryman of the Israel Defense Forces, published the sell rating, the stock more than doubled. Even after an 12-week plunge that lopped $50bn from its market value, Valeant is only down 6.1% from when the analyst initiated the sell recommendation. Since Valeant’s record in August, the stock has tumbled 55% to $117, and three analysts have cut ratings.

Among 19 other firms that followed the company before the plunge, 11 have reduced their price targets and none have touched the ratings.

“It’s a lonely place, no question,” said Khmelnitsky, who has worked at Veritas since 2006. “You try to do what you can and keep your head above water.”

Annabel Samimy, an analyst at Stifel Nicolaus & Co, has maintained a buy recommendation on the stock since 2010 and a price target of $285 since July. “If I did a fundamental analysis today, I would still probably come to the same place,” she said in an e-mail.

Samimy’s price target is based on discounted cash flows, she said, adding that the stock will bounce back only when perception shifts. “Clearly from the stock movement in recent weeks, the stock call has been wrong,” she wrote. “I still think the company is undervalued; that hasn’t changed. Perception has shifted, not performance.”

Other analysts have cut price targets while leaving their recommendations alone. Tim Chiang, an analyst at BTIG, has trimmed his 12-month forecast to $175 from $290 as recently as Sept. 25. The more tepid target is feasible, particularly now that “valuation has been cut in half,” he said by phone.

“Specialty pharmacy made up about what, 7%? So the other 90-plus% of their business we think is still intact,” Chiang said. “In a lot of ways the damage has already been done to the stock.”

Michael Waterhouse, an analyst at Morningstar has maintained a buy rating on Valeant since late September, saying the company is fairly valued at $230 a share. “It’s entirely possible we’re overestimating management’s ability to steer through this,” he said by phone. “We’re going to revisit our assumptions. We’re still in the process of doing that.”

Thirteen other analysts with the equivalent of buy ratings didn’t respond to phone calls or messages seeking comments.

Analysts are generally more optimistic about stocks with a history of huge gains. Among the 10 high-flyers in the S&P 500 whose bull-market share trajectories are most similar to the Laval, Quebec-based drug company, 62% of ratings are buys, compared with 50% for the index. Those companies included Wyndham Worldwide Corp, which soared 2,471% in the six years to August to Netflix, which added 2,149%.

Short sellers did no better than analysts in anticipating Valeant’s rout. Short interest averaged 0.27% of shares outstanding in the two years leading up to October, according to data from Markit. That compares with an average level of 2.2% in S&P 500 stocks.

Irina Koffler, an analyst at Mizuho Securities, said Valeant’s conference call on Monday helped allay some worries and prompted her to upgrade the stock to buy from neutral on Tuesday. Koffler, who has only covered the stock since October 8, is the lone newly optimistic analyst among the 25 who now follow the company.

Speaking generally and not about Valeant in particular, Wall Street analysts are too optimistic about the stocks they cover, said Douglas Cumming, a professor at York University’s Schulich School of Business in Toronto, who has researched stock ratings.