Bloomberg

Dubai

Middle East corporate bonds are mispricing the effects plunging oil prices are having on the region’s finances, leaving borrowers vulnerable to a deterioration in market sentiment.

The average premium investors require to hold bonds from the Middle East and North Africa was 159 basis points on Friday, two points lower than this year’s high in June, JPMorgan Chase & Co indexes show. That compares with 165 basis points on US investment-grade debt, according to the Bloomberg US Corporate Bond Index.

“The Middle East’s grossly mispriced credit spreads will eventually blow out to reflect the new economic reality,” Ghassan Chehayeb, the chief investment officer at Texas-based Sancta Capital Group Ltd, a distressed-debt money manager, wrote in a note this month. The change in spreads since Opec’s decision to maintain oil output last year doesn’t take into account “the risk premium investors should demand given the deteriorating fundamentals,” he said.

With crude prices close to six-year lows, budget deficits in the six-member Gulf Cooperation Council will reach 13.2% of gross domestic product this year - compared with a surplus in 2014 - as financial buffers in some nations are depleted, the International Monetary Fund said on October 21. The pricing discrepancy that has left GCC spreads narrower than in the US since August reflects how Middle Eastern banks and institutions have favoured a buy-and-hold strategy amid a slump in bond issuance to a four-year low, according to Abdul Kadir Hussain at Mashreq Capital DIFC Ltd.

Brent crude, the benchmark for about half the world’s oil, has slumped more than 30% since Opec decided to hold production steady in November.

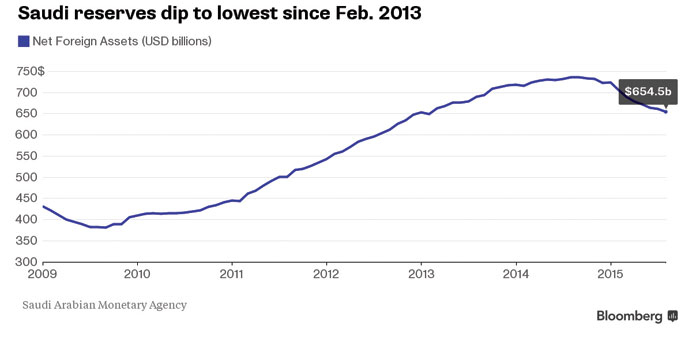

Saudi Arabia, the biggest Arab economy, relies on oil revenue to fund about 90% of its spending, and the decline will widen its budget deficit to more than 20% of economic output this year from 2.3% last year, the IMF said last Wednesday.

The bonds don’t reflect the change in the region’s “risk profile,” said Hussain, chief executive officer of Dubai-based Mashreq, which runs the region’s best-performing sukuk fund, describing corporate debt as “overvalued.” A change could occur if “you have a lot of new issues which then come and reprice the market,” he said.

A 15% decline in bond sales from the Middle East and North Africa this year to $30.3bn has helped keep bond yields depressed. Issuers held back sales in the summer to avoid the volatility in bond markets sparked by China’s slowing economy and expectations that the US Federal Reserve was close to raising interest rates after leaving them near zero since 2008.

Some widening of spreads in the region over the past three months has created pockets of value as oil remains in a narrow range and credit risk is contained, according to Anita Yadav, the Dubai-based head of fixed-income research at Emirates NBD, the UAE’s second-biggest bank by assets.

UAE paper including from Abu Dhabi National Energy Co and Bank of Sharjah is oversold “and we also find value in Oman Electricity Transmission Co’s 2025 bond,” Yadav said by phone on October 20.

Saudi Arabia may run out of financial assets needed to support spending within five years if the government maintains current policies, the IMF said. The same is true of Bahrain and Oman, while Kuwait, Qatar and the UAE have financial assets that could support them for more than 20 years, the Washington based lender said.

Investors are “still not fully pricing in the geopolitical risk in the region nor the cheaper oil,” Ahmed Shehada, executive director for advisory and institutions at NBAD Securities, a unit of the UAE’s biggest bank, said by phone from Dubai last Thursday. Middle East spreads “should be about 20-30 basis points higher than the US and we will eventually adjust when governments start to cut spending and corporates start to report numbers that are not as expected,” he said.