Emerging markets (EMs) appear to be “at the heart of the third wave of the fallout from the global financial crisis”, QNB has said in a report.

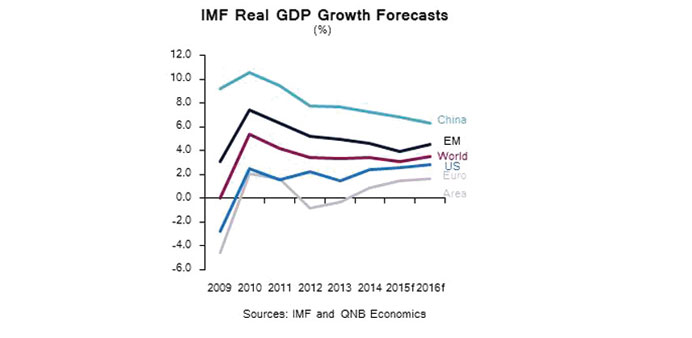

In its recently published World Economic Outlook, the International Monetary Fund (IMF) expects global growth to fall to 3.1% in 2015, down from 3.4% in 2014. This is the “slowest” expansion in the world economy since the “great recession” of 2009.

The activity in emerging markets (EMs) is forecast to slow for the fifth consecutive year, while the recovery in advanced economies is projected to pick up slightly. EMs have been the engine of growth in the global economy in recent years, growing at an average annual rate of 5.3% between 2010-14.

They were responsible for more than 80% of global growth, which averaged 3.6% a year over that period.

However, EMs appear to be at the heart of the third wave of the fallout from the global financial crisis. The first wave was the US housing and financial crisis in 2008-9. This was followed by the sovereign debt crisis in the euro area in 2011-12. And now, EMs are in the midst of a crisis sparked by the prospect of US monetary policy normalisation and the rebalancing of the Chinese economy from investments and exports towards consumption and services.

“EMs are facing a number of headwinds,” QNB said.

First, there are “long-term structural drags on growth” as the “economic rebalancing in China leads to slower growth.” The slowdown is impacting external demand, particularly in emerging Asia, where a number of economies are heavily dependent on China for exports. Weak Chinese demand has depressed prices of a number of commodities, negatively impacting commodity-exporting economies, which are predominantly EMs.

Second, there are “cyclical drags” on growth, mainly related to “high debt levels and tightening financial conditions”. Expectations of higher US interest rates have led to capital flight, weaker currencies and higher interest rates within EMs. Meanwhile, a stronger dollar has increased the value of EM foreign-currency debt, making it more burdensome to service.

Finally, “deleveraging is leading to slower credit growth and further dragging on GDP.”

Going forward, QNB said the structural factors dragging on growth are likely to persist. China’s rebalancing and working through its large debt overhang will continue into the medium term.

As low commodity prices are related to the strength of China’s economy, these may also take time to recover. But cyclical drags on growth, which are mainly financial, may be less persistent.

Financial markets may have already partially adjusted to higher expected US interest rates, so drags from capital flight and weaker exchange rates should start easing by 2017. Therefore, the IMF expects emerging markets’ GDP growth to recover from 4% in 2015 to 4.5% in 2016 and 4.9% in 2017.

Meanwhile, advanced economies grew by 1.8% in 2014, a relatively slow rate but still above their potential growth, which has been weakened by declining and ageing population and slower productivity growth. Favourable cyclical factors have contributed to above-trend growth. These include: fading fiscal drag; lower energy prices which have boosted household disposable income given that most of these countries are net energy importers; unprecedentedly easy monetary policy; and positive wealth effects from the recovery in the housing market in the US and the stock market in Japan.

Some regions, such as the euro area and Japan, have also benefited from a sharp depreciation in their currencies, which has helped boost their exports. Since May 2014, the euro and the yen have depreciated by 18.5% and 17% against the dollar, respectively. Overall, these favourable cyclical dynamics led to falling unemployment rates in advanced economies.

The IMF expects advanced economies to continue growing at an above-trend rate. Real GDP growth is expected to pick up from 1.8% in 2014 to 2% in 2015 and then 2.2% in 2016, as most of the cyclical tailwinds are projected to persist despite the expected normalisation of monetary policy in the UK and the US.

“Overall, the recovery in advanced economies is not strong enough to compensate for the slowdown in EMs. As a result, global growth is expected to remain below its pre-crisis levels for the foreseeable future. The risks remain tilted to the downside, largely concentrated in EMs and, in particular, China,” QNB said.