Bloomberg/Mumbai

Prime Minister Narendra Modi’s goal to put a roof over India’s 1.3bn people just got a fillip.

After slashing the benchmark repurchase rate by a more-than-expected 50 basis points last month to a four-year low, Reserve Bank of India governor Raghuram Rajan on October 8 eased mortgage rules, allowing lenders to set aside less capital to cover home-loan default risks, effectively helping lower their cost of funds.

Rajan’s policies are starting to show results in a boost to Modi’s plan for 20mn homes by 2022 under his “Housing for All” programme. State Bank of India, the country’s biggest lender by assets, says it is assessing the impact of the reduction in risk weights and may consider further decreasing borrowing costs for home buyers after already dropping its housing loan rates last month.

“Reduction in interest rates along with the increased loan-to-value ratio will help in growing home loans at a faster pace,” Jayanthi Lakshmi, SBI’s chief general manager for real estate, habitat and housing development said in an interview. “In a market like India, where mortgage penetration is low, this will help in expanding the market.”

The central bank increased the threshold for loans with a loan-to-value ratio of 90% to Rs3mn ($46,111) from an earlier Rs2mn. It reduced the risk weight for some loans to as low as 35% from as high as high as 50%.

The push for housing from both the central bank and Modi is good news for the nation’s banks that are struggling as credit growth near a 20-year low weighs on profits.

Lending in India grew by 9.6% in 12 months to September, the least in almost two decades. The five largest banks by assets in India have lowered their lending rates since September 29 after the RBI cut the benchmark interest rate. State Bank cut its mortgage rates for new borrowers to 9.55% starting October 5, the lowest offered by the lender in four years.

The average size of home loans at SBI is Rs2.3mn and the central bank’s move will help in bolstering the affordable housing segment, Lakshmi said.

The new rules may also help boost volumes where Indian real-estate companies are struggling with dwindling sales.

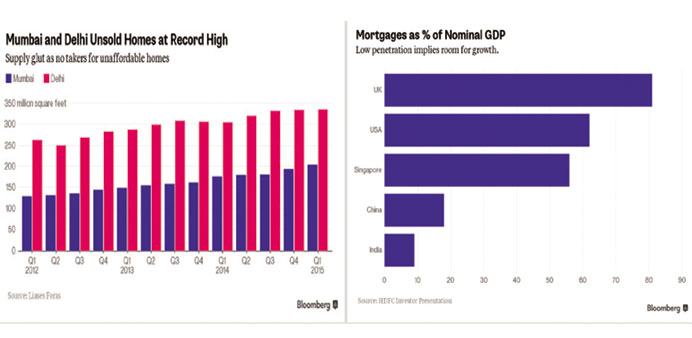

Home sales in India’s top eight property markets fell 4% in the quarter through June from a year earlier, while unsold inventory rose by 18%, according to research firm Liases Foras, which estimates it will take at least 45 months to find buyers for unsold homes in Mumbai alone.

The 13-member S&P BSE India Realty Index has declined 7.2% this year. Shares of DLF Ltd, the country’s largest developer by market value, have slipped 2.1% in the period, while those of Poddar Developers Ltd, a builder of affordable homes in the outskirts of Mumbai, have advanced 21%.

Rohit Poddar, managing director of Poddar Developers, says the steps are in the right direction because non-performing assets in home loans across segments are less than 1% and a small fraction of the overall soured debt.

Still, they aren’t enough to boost demand until the full benefits are passed on to the home buyer, he said, adding the ticket size of the loan should be raised to Rs4mn.

“If one is building affordable homes in Mumbai, one has to realise that higher land costs make affordable homes cost more here than in other cities,” he said.

India’s urban population may reach 600mn by 2031, up from 377mn in 2011, according to the government. With a shortage of 18.78mn urban housing units, the government is focusing more on reducing squalor in cities and towns. It has shortlisted 305 cities and towns across nine states to start building houses for the poor.

The central bank measures “will make more credit available to borrowers and thus improve the current market sentiment especially in the upcoming festive season,” according to Tata Housing Development Co. “This will help to improve the affordability of low-cost housing for the economically weaker sections.”