Bloomberg

Hong Kong

Alibaba Group Holding is heading for the fourth straight monthly decline in its stock price as analysts cut their revenue estimates for the most important quarter of the year.

Twelve analysts have cut sales predictions for the Chinese e-commerce company in the past four weeks for both this quarter and the next as the country’s economy cools. Alibaba shares have dropped 13% in September, bringing the market value decline since the end of May to about $75bn.

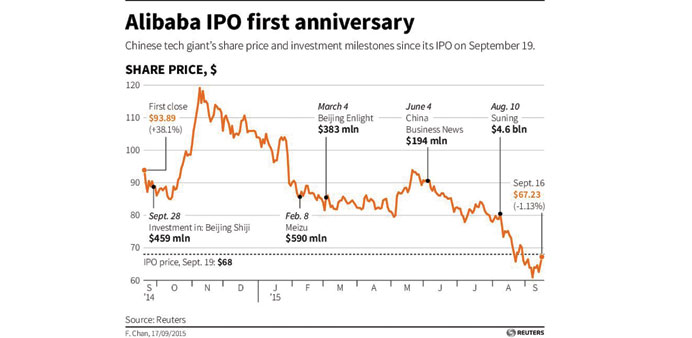

Alibaba has gone through a dramatic reversal of fortune since holding the largest-ever initial public offering last year, dropping to a record low close this week. China’s slowing economy has raised concerns that sales will be muted during the biggest shopping day of the year, Singles’ Day on November 11, with the challenges compounded by competition from JD.com Inc and other rivals.

“I would refrain from recommending this stock to investors as there are too many uncertainties,” said Ray Zhao, a Shenzhen- based analyst at Guotai Junan Securities Co. “China’s macro economy isn’t upbeat, and Alibaba’s facing a market saturation in big cities, which means a slowdown in new user growth.” The analyst downgrades follow a more bearish prediction by the company itself.

Gross merchandise value in the quarter ending September may come in “mid-single-digits lower” than Alibaba’s initial expectations, investor relations chief Jane Penner told the Citi Global Technology Conference earlier this month.

Alibaba is now projected to post the slowest sales growth since its IPO, with revenue rising 27% to 21.4bn yuan ($3.4bn) in the three months ending Wednesday, according to the average of analyst estimates. Next quarter will weaken even further, with a 24% increase, according to analysts’ average estimate.

In the previous 12 quarters, Alibaba’s average revenue growth rate was 56%. Singles’ Day generated 57.1bn yuan of sales last year.

“The next couple of quarters will be difficult,” said RJ Hottovy, an analyst at Morningstar, who upgraded Alibaba to a buy on September 22. Recent criticisms of the company have been overblown, presenting a good buying opportunity, he said.

“Investors have to have some patience.”

While analysts are more bearish on sales growth at Alibaba, that sentiment hasn’t spread to its rivals. In the past month, there haven’t been any revisions to sales estimates for JD.com, China’s second-largest e-commerce operator, or its partner Tencent Holdings, according to data compiled by Bloomberg. While Alibaba shares have dropped 44% this year, both of its rivals have risen in the same period. JD shares have risen 5.6% this year in New York trading, and Tencent about 15% in Hong Kong.

Alibaba’s decision to replace its chief executive officer and buy back stock has failed to calm investor fears about slowing growth, with short sellers boosting bearish bets on the stock to a record in September.

Even increasing mobile shopping on its Taobao Marketplace and Tmall.com platforms to capture a customer shift to smartphones and tablet computers, now generating more than half of transaction volumes, has failed to turn around the stock. “Investors fancy Alibaba’s mobile prospects because they expect Alibaba to capture new customers in low-tier cities that are new to Taobao and mobile shopping. Yet we do not see this as a new growth catalyst,” Li Muzhi, a Hong Kong-based analyst at Arete Research Service, wrote in a report. “We also do not see a case for paying a premium valuation for Alibaba’s mobile transition.”