Bloomberg

Santiago

Alexandre Tombini’s pledge to use all the tools he has to tame volatility in Brazil’s real provided a respite on Thursday for the beleaguered currency. Strategists at Citigroup Inc and Standard Chartered say it won’t be enough to calm markets.

The central bank president’s comments helped send the real from a record low to its biggest gain in seven years on Thursday as it surged 5.8%. It trimmed gains on Friday. The currency’s down 9% in the past month, more than any other emerging-market currency. And investors are bracing for more pain amid doubts the government will be able to shore up its budget and lead Brazil out of what’s forecast to be its worst recession since the 1930s.

The rout in the real shows the loss of confidence in Brazil and prompted Tombini’s attempts to reassure investors at a surprise press conference, one day after the central bank said it would sell new foreign-exchange swaps to support the real for the first time in six months. Currency derivatives show investors betting on further losses as President Dilma Rousseff struggles to win support for spending cuts and tax increases her administration says are needed to avoid further credit-rating downgrades to junk.

“I don’t think they can do anything to stop the market,” Christian Lawrence, a currency strategist at Rabobank, said from New York. “There’s no central bank in the world that can defend against this selloff.”

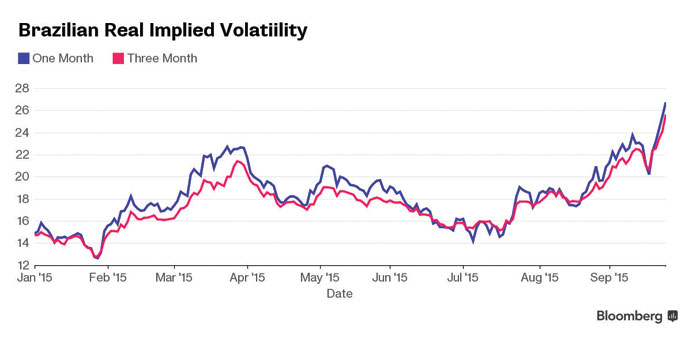

After Standard & Poor’s cut its rating on the country to junk earlier this month, implied one-month volatility in the real surged to the highest in emerging markets. Local interest rates soared on bets the central bank will have to raise borrowing costs to keep a lid on inflation that’s already double policy makers’ target. Bond risk is at the highest since October 2008, with five-year credit default swaps up more than 1 percentage point since the downgrade to 4.76 percentage points, trailing only Venezuela among sovereigns in the Americas.

Brazil finds itself in dire straits at what’s already a horrible time for emerging markets. Currencies from developing nations are trading at the lowest since at least 2008, while the yields investors demand to hold emerging-market bonds are at their highest since 2011 amid concern that a slowdown in China will damp global growth just as a potential interest-rate increase in the US draws capital from the most vulnerable markets.

Investors have been disheartened at Rousseff’s inability to win support for a package of fiscal measures that she says will return the country to a primary budget surplus next year. Opposition lawmakers say her proposals will hurt Brazil’s middle class after a decade of progress fuelled by a surge in commodities prices helped pulled 35mn people out of poverty.

Tombini’s comments reassured traders who were nervous the central bank would move toward emergency rate increases, said Kenneth Lam, a currency strategist at Citigroup. Yet on their own they won’t calm volatility, he said.

“From the outset this has been a political crisis,” Lam said from New York. “At the end of the day, you need a political solution to turn things around.”

At a press conference in Brasilia on Thursday, Tombini said the central bank could use all instruments, including its international reserves, to assure that currency and interest- rate markets function properly. He rejected traders’ bets on rate increases and reiterated policy makers’ plans to keep benchmark borrowing costs on hold.

“The increase of interest rates in the market will not be used as a guide for monetary policy,” Tombini said.

Brazil’s central bank offered up to $4bn in foreign- exchange credit lines in two different auctions on Wednesday, and announced two auctions of new swap contracts for Wednesday and Thursday. A similar programme was in place from August 2013 to March 2015 amid efforts to quell inflation.

The swaps and credit lines weren’t particularly effective at supporting the real in the past and bringing them back is unlikely to make an impact, according to Morgan Stanley.

“Political uncertainty makes any adjustments more difficult, in particular structural reforms with potential for meaningful positive impact,” Morgan Stanley strategists led by James Lord said on Thursday in a note to clients.

The gap between spot values for the real and one-month non-deliverable forwards rose to the highest in six years. That implies traders still expect yields in reais to rise faster than yields in dollars. Twelve-month non-deliverable forwards show wagers that the currency will decline to about 4.45 per dollar in a year’s time.

“To arrest this decline we’re going to have to see something quite dramatic from a policy standpoint,” Mike Moran, the head of economic research for the Americas at Standard Chartered, said from New York. “Direct intervention typically doesn’t work.”