Bloomberg

Beijing

China’s riskier banks are investing more customer funds in financing that is kept off their loan books, making it harder for rating companies to gauge their asset quality.

There has been a surge in a balance-sheet item known as receivables, which often includes shadow funding such as trusts and wealth products, said Moody’s Investors Service. Fitch Ratings said it is hard to analyse this escalation in activity.

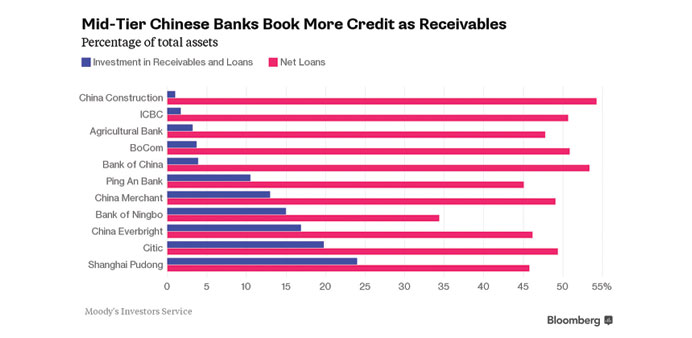

Listed banks excluding the Big Four saw short-term investments and other assets – which include receivables – jump 25% in the first-half, compared with total asset growth of 12%, data compiled by Bloomberg show.

Slower growth in the world’s second-largest economy coupled with “still significant” credit expansion prompted Standard & Poor’s to cut its view of the banking industry’s economic risk to negative from stable this week. Shadow-finance assets, estimated at 41tn yuan ($6.4tn) by Moody’s at the end of 2014, have become more attractive as five interest-rate cuts by the central bank since November curbed profits from lending.

“Our concern with some of these investment positions is banks are using them as a way to bypass lending restrictions,” said Grace Wu, a senior director at Fitch in Hong Kong. “Unlike bank loans, they don’t get reported into loan provisions, so it’s more difficult for us to ascertain the asset quality.” The opacity of Chinese banks’ credit exposure helps explain why they are priced as if investors are expecting a non-performing loan ratio of 10 to 12% next year, which would mark a “sizeable credit crisis” in other countries, according to Wei Hou, a banking analyst at Sanford C Bernstein & Co. The reported ratio is 1.5%, according to the China Banking Regulatory Commission. The nation’s shadow-banking industry emerged as a way for creditors to circumvent lending restrictions and for savers to attain yields higher than the legally capped deposit rate. It includes trusts, asset-management plans and wealth-management products, which package loans into products for buyers.

Shanghai Pudong Development Bank Co’s receivables made up about a quarter of assets as of June 30, according to its semi- annual financial statement. Out of 1.1tn yuan of receivables, 82% were trusts and asset-management plans that purchase trust loans, while 11% were other lenders’ wealth management products. The receivables climbed in the first-half because the bank invested more in other lenders’ guaranteed WMPs as well as in asset-management products derived from bills issued by large banks, Shanghai Pudong said in an e-mail. It added that its credit and liquidity risks are both manageable.

Adding loan investments and receivables to banks’ loan-to-deposit ratios pushes the figure close to or even over 100% for some commercial lenders, such as Shanghai Pudong and China Citic Bank Corp, according to Moody’s analysis.

“Though they’re called investments, they’re less liquid than most investments,” Christine Kuo, a senior vice president at Moody’s, said at a briefing in Taipei. “So the funding you’re relying on isn’t steady deposits but more sensitive wholesale money. When the market is tighter, the banks’ liquidity management will be more difficult.” Chinese banks are already facing slowing deposit growth amid competition from higher-yielding investments. Deposits climbed an average 12% each month in 2015 from a year ago, compared with 15% in the five previous years. While interbank rates have become steadier in the past year amid monetary easing, they are still more volatile than in other markets. The three-month Shanghai Interbank Offered Rate moved in a range of 2.3 percentage points over the past year, compared with 0.12 percentage point for the London interbank offered rate of the same tenor.