Bloomberg

Beijing

Stimulus unleashed by China’s central bank will cushion Chinese companies – the region’s biggest dollar debt issuers – from a potential Federal Reserve interest rate increase next month, making cheaper yuan funds available.

Five interest rate cuts by the People’s Bank of China since November and rules to relax yuan bond issuance onshore mean Chinese companies are becoming less reliant on dollar funding.

Corporates from the world’s second-biggest economy have some $302.9bn in dollar-denominated bonds outstanding, and will face higher costs to issue more such notes, or repay them in yuan, if the US central bank tightens monetary policy.

“Fed rate hikes would imply that the cost of borrowing offshore debt will be higher, assuming the same credit spread,” Raymond Chia, the head of credit research for Asia ex-Japan at Schroder Investment Management in Singapore, said. “But given the PBoC is relaxing measures and cutting rates, more issuers would consider raising funds onshore as onshore funding costs are getting cheaper.”

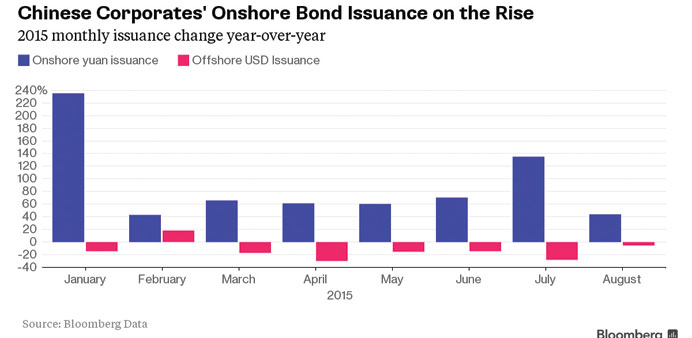

The shift to yuan funding is already happening, with domestic corporate bond sales jumping 77% to 7.85tn yuan ($1.23tn) in 2015 from the same period last year, according to data compiled by Bloomberg. Dollar offerings from Chinese companies fell 17% to $117.2bn. It’s a contrast to 2013 when the Fed’s ‘taper tantrum’ saw Chinese companies mostly shut out of the US currency market for about three months while yuan borrowing costs were higher than current levels.

Yields on five-year onshore government bonds have dropped 34 basis points so far in 2015 to 3.17% while yields on similar-maturity AA rated corporate notes have declined by 1 percentage point to 5.15%.

Last month’s yuan devaluation by the PBoC could also work to stoke demand from wealthy Chinese for dollar assets because the US currency is still on a rising path, said Ben Sy, the Hong Kong-based head of Asia fixed income, currencies and commodities at JPMorgan Chase & Co’s private banking unit. That could alleviate the negative impact on Chinese dollar bonds in the case a Fed rate increase boosts market volatility, he said.

Higher-yielding US currency debt, such as junk-rated Chinese notes, could benefit. Yields on such bonds have dropped 12 basis points to 9.66% this month, according to a Bank of America Merrill Lynch index.

The yuan may depreciate to 6.5 per dollar by the end of this year and 6.8 next year, according to forecasts by Liu Dongliang, a senior analyst at China Merchants Bank Co. “Onshore demand for China dollar bonds is going up whereas offshore supply is down this year,” said Owen Gallimore, a senior Asia credit analyst at Australia & New Zealand Banking Group in Singapore. “The depreciation of the yuan and a potential Fed hike is only adding to the secular growth in demand for dollar assets.”