Andy Home is a columnist for Reuters. The opinions expressed are his own.

By Andy Home

London

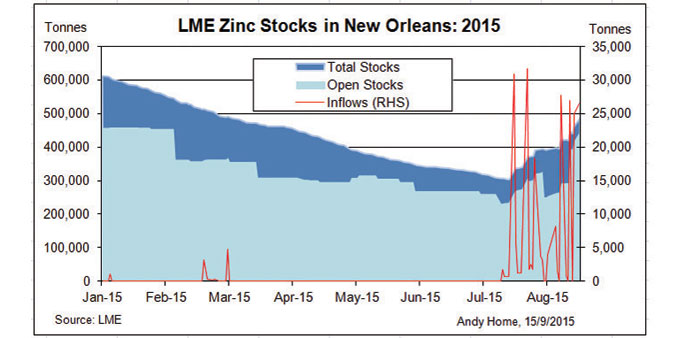

There sure is a lot of zinc in New Orleans. Yesterday’s latest stocks report from the London Metal Exchange (LME) showed another 26,600 tonnes of zinc being warranted at the US port.

That brings the cumulative inflow to a massive 228,225 tonnes since the start of August. The deluge of metal has transformed the LME zinc stocks landscape.

The headline total hit a low point of 426,875 tonnes on August 6, at which stage exchange stocks were down by almost 264,000 tonnes, or 38%, on the start of the year. As of today that year-to-date decline has been slashed to just 73,500 tonnes.

Moreover, open tonnage of 553,075 tonnes is now at the highest level since December last year. Not entirely surprising, the appearance of so much metal has extinguished any residual bull ardour for zinc. The galvanising metal was the second-best performer in the LME pack back in May, when LME stocks were grinding steadily lower. It is now the second-worst performer next to bombed-out nickel.

But what exactly is going on in New Orleans?

New Orleans is nicknamed The Big Easy and as far as zinc is concerned it’s long been the easiest location for storing surplus metal.

Lacking any significant consumer base in its hinterland, New Orleans operates as something of a black hole in global zinc flows. Warranting metal in the city means effectively quarantining it from the rest of the market, particularly in terms of alleviating pressure on physical premiums elsewhere.

If it’s in New Orleans, it’s surplus to immediate physical requirements.

And if it’s surplus to requirements, the metal needs financing, a trade dependent on the shape of the forward curve. If the curve is in contango, financing stocks can generate a small but easy, low-risk return. If it’s in backwardation, that return becomes a cost.

The zinc curve has been relatively tight over much of this year but the exception was in February and March, when the benchmark cash-to-three-months period traded as wide as $22.25 contango.

Over those two months a total 155,375 tonnes of zinc in New Orleans were cancelled, the subsequent daily load-outs driving the downtrend in both local and system-wide stock levels.

The more optimistic of the bulls equated falling stocks with physical tightness, a perennial holy grail for believers in the zinc narrative of pending raw materials shortfall. Yet, it should have been obvious that when someone cancels 91,400 tonnes of metal in one day, as was the case back on February 10, it is far more likely to be the work of a financier than a physical metals player.

Just as contango incentivised financiers to grab large amounts of zinc in the first quarter of this year, the recent tightening of the spreads has coincided with much of that metal reappearing.

As recently as the end of August the cash-to-three-months period was trading in small backwardation, in essence removing any incentive for a stocks financier either to roll over any existing deal or to initiate a new one.

The main cost component of the financing trade is the cost of storage. The cheaper the warehousing storage deal, the more return can be made from the curve structure on the LME.

This is why so much zinc left New Orleans earlier this year. Off-exchange storage is a lot cheaper than LME storage.

Warehouse companies will compete both for off-market storage and for metal being returned to the LME system by offering special deals and incentives.

And it’s clear that one of the complicating factors in the current mass movement of zinc at New Orleans is the underlay of a warehousing war. Zinc storage, indeed storage of all LME metals, in New Orleans has been largely controlled by Pacorini Metals this year.

At the end of July the warehousing arm of physical power-house Glencore held all but 4,335 tonnes of the 388,740 tonnes registered in New Orleans.

That changed dramatically over the course of last month.

Three other operators saw significant amounts of metal warranted at their New Orleans sheds. ISTIM Metals took in 78,400 tonnes, Henry Bath 14,585 tonnes and Pacorini Holding, the original owner of the Pacorini franchise which has now returned to the LME storage game, 4,400 tonnes.