By John Kemp /London

Saudi Arabia and its Opec allies are counting on strong growth in demand coupled with slower growth in non-Opec supply to rebalance the oil market in 2016.

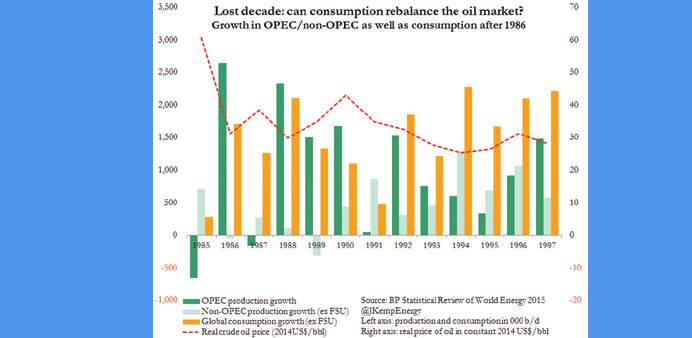

But the experience of the “lost decade” after prices slumped in 1986 suggests rebalancing could take longer than some Opec members and market analysts expect.

Following the price slump in 1985/86, the oil market struggled with persistent surpluses for much of the next 17 years. In real terms, oil prices did not rise above the 1986 crisis level on a sustained basis until 2003.

Lower prices led to consistent strong growth in oil consumption after 1986, reversing the decline in demand that had occurred in the first half of the 1980s.

Non-Opec supplies were flat between 1985 and 1989, as lower prices halted the exploration and production boom that had caused non-Opec production to surge since 1976.

But non-Opec oil supplies did not fall, disappointing expectations of some oil ministers that lower production outside the organisation would make way for increased production by its members.

From 1991 onwards, non-Opec began growing rapidly again, and generally kept pace with the growth in the organisation’s output until 2003.

Opec’s own output grew strongly after 1986 even though prices failed to rise. Real prices were essentially unchanged between 1986 and 1997 while the organisation’s output rose from 18.5mn bpd to 29.5mn bpd.

Saudi Arabia, Iraq, Iran, Kuwait and the United Arab Emirates all boosted production and invested in extra capacity in pursuit of a higher share of the oil market.

The unexpected resilience of non-Opec production, coupled with continued output increases from within Opec itself, ensured real oil prices did not rise despite the rapid growth in consumption.

The organisation’s members successfully increased their market share after 1986, but failed to achieve the rise in real prices that they repeatedly stated was their objective.

It was not until the early 2000s, almost two decades later, that falling non-Opec supplies and surging fuel demand from China and the rest of East Asia, resulted in sustained price increases.

In a prescient editorial published in the New York Times in July 1985, oil expert Daniel Yergin reviewed the factors which had caused prices to fall and how the market would eventually recover.

“When corrected for inflation, US oil prices in 1985 are just about back to where they were in 1975,” he wrote.

“Four factors have been responsible for this: conservation, the recession, weak economic activity and the growth of alternative, non-Opec supplies. All of this has put us in an era of surplus in which prices have nowhere to go but down.”

Yergin went on to predict the oil market would eventually adjust. “Further weakness in price will undermine the rationale for a great deal of existing and new investment in energy. Energy consumers will conclude that conservation investment is less important. Oil companies will reduce their efforts to develop new oil fields in frontier regions,” he concluded.

“Does this mean that the world will again face a difficult energy situation in the future? Not for several years, at least.

The surplus of oil and energy worldwide is very large ... That cushion will be quite a number of years in eroding. Oil will become more like other commodities, with volatile prices.”

Yergin was correct that reduced investment would eventually erode spare capacity and the era of surplus would end, but even he might have been surprised that it would take almost 20 years.

There are important differences between the oil market situation in 2015 and back in 1986. There is less spare capacity to work off now, less than 2mn bpd compared with 6mn in 1986.

* John Kemp is a Reuters market analyst. The views expressed are his own.