Reuters/Beijing/Shanghai

China’s central bank said yesterday there was no reason for the yuan to fall further given the country’s strong economic fundamentals, helping to restore calm to jittery global markets after it devalued the currency earlier in the week.

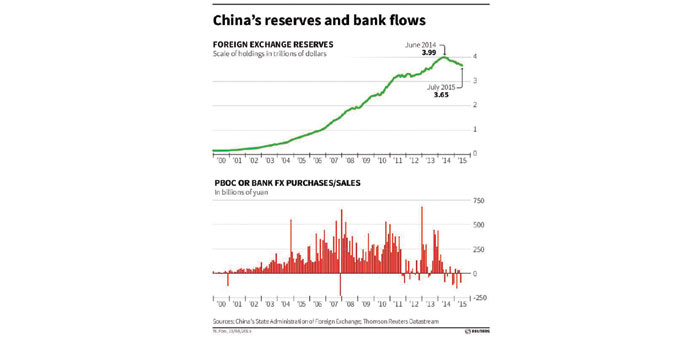

As the yuan slid for a third straight day, the People’s Bank of China (PBoC) said the strong economic environment, sustained trade surplus, sound fiscal position and deep foreign exchange reserves provided “strong support” for the exchange rate .

China’s decision to devalue the currency on Tuesday by pushing its official guidance rate down 2% sparked fears of a “currency war” and roiled global financial markets, dragging other Asian currencies to multi-year lows.

It also drew accusations from US politicians that Beijing was unfairly supporting its exporters.

The PBoC said at the time that the move was a one-off depreciation, but sources involved in the Chinese policy-making process told Reuters that some powerful voices within government were pushing for the yuan to go still lower, suggesting pressure for an overall devaluation of almost 10%.

PBoC vice-governor Yi Gang said it was nonsense to believe that government expected the yuan to fall that far.

Earlier yesterday, the PBoC said there was no basis for continued depreciation of the yuan.

However, even if the central bank succeeds in putting a floor under the yuan for now, poor July economic data and expectations of more interest rate cuts later in the year are likely to fuel expectations that authorities could let it weaken further.

Fitch ratings agency said yesterday that the depreciation in the yuan “highlights wider pressures on the economy”, but also demonstrated that authorities remained committed to market-oriented reform, a commitment many had questioned after Beijing’s heavy-handed interventions to stem a plunge in its stock markets in June.

Vice-governor Yi said China would quicken the opening of its foreign exchange market and would attract more foreign investors as it liberalises its financial markets.

Officials said the PBoC had stopped “regularly” intervening in the foreign exchange market but allowed that it could conduct “effective management” of the yuan in cases of extreme volatility.

Traders said the central bank appeared to have been caught off guard by the intensity of selling that was sparked by its surprise move on Tuesday, and believe it ordered big state banks to support the currency late on Wednesday, which influenced the PBoC’s official guidance rate for the following day.

State banks were also believed to be buying yuan and selling dollars yesterday.

Though the yuan opened slightly weaker yesterday, the spot rate was only about 0.1% below the guidance rate, the closest it has been since November, as the central bank tried to slow the sharp sell-off that has knocked around 3.2% off the currency since Monday’s close.

Spot yuan closed at 6.399 to the dollar, down 0.2% from Wednesday’s close, and almost level with the guidance rate.

The spot rate is currently allowed to trade within a range of 2% above or below the official fixing on any given day, and had been consistently trading over 1% weaker than the midpoint since March.

Shares rose in Asia and Europe, while yields on German government bonds, which had fallen on the previous two days as investors sought safe-haven assets, edged higher. Fears of a global currency war also eased.

“We are seeing a much calmer market today (Thursday) ... now it’s understood that it’s actually not an intentional steering of the yuan exchange rate, but rather ... a more market-driven move,” said Commerzbank currency strategist Esther Reichelt in Frankfurt.

Tuesday’s devaluation followed a run of weak economic data and resulted in the biggest one-day fall in the yuan since 1994, raising market suspicions that China was embarking on a longer-term depreciation of its exchange rate that would make Chinese exports cheaper.

Data on Chinese factory activity growth and retail sales on Wednesday underlined sluggish growth in the world’s second-largest economy, while fiscal expenditures jumped 24.1% in July, reflecting Beijing’s efforts to stimulate economic activity.

Weighed down by weak exports, sluggish domestic demand and a cooling property market, growth in the world’s second-largest economy is expected to slow from 7.4% in 2014 to 7% this year, its slowest pace in a quarter of a century.

China’s Ministry of Commerce, which sources said led the pressure within government for yuan depreciation, said it expected exports to see growth for the full year and was studying new measures to support trade.

Some Chinese steel producers have already cut export prices in response to the lower yuan, industry sources said, but analysts said the currency’s drop so far has been too mild to boost shipments much given sluggish global demand.

The PBoC also said yesterday that it would monitor “abnormal” cross-border flows after the devaluation raised fears that investors would seek to pull capital out of China in anticipation of further falls in the currency. Pages: 6, 8, 12