AFP/Beijing

China weakened its currency for the third consecutive day yesterday, but financial markets that had been shaken by the surprise devaluation took heart as authorities pledged not to let the yuan plummet.

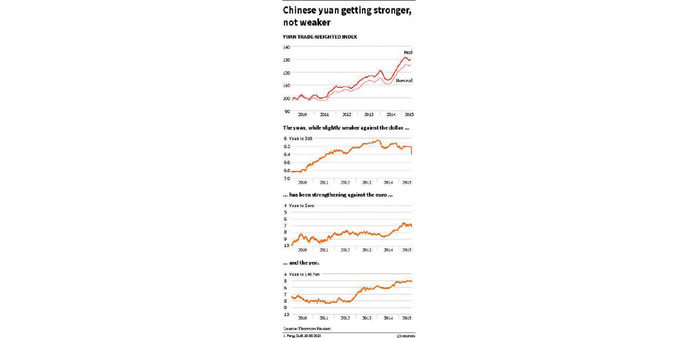

The central bank trimmed the reference rate for the yuan – also known as the renminbi (RMB) – by 1.11% to 6.4010 yuan for $1, the China Foreign Exchange Trade System said, from the previous day’s 6.3306.

The cut was less than the previous two days and came after reports the People’s Bank of China (PBoC) intervened Wednesday to stem the yuan’s fall.

China adopted a more market-oriented method of calculating the currency rate this week in a move widely seen as a devaluation, raising fresh questions about the health of the world’s second-largest economy. After global stock and currency markets staggered in response, the PBoC went on the offensive yesterday, telling reporters that the yuan was still a strong currency and that Beijing would keep the unit stable.

“Currently, there is no basis for the renminbi exchange rate to continue to depreciate,” assistant governor Zhang Xiaohui told a briefing, according to a transcript. “The central bank has the ability to keep the renminbi basically stable at a reasonable and balanced level,” she said.

The comments drove a relief rally yesterday in Asian shares and Asia-Pacific currencies, which suffered their biggest two-day selloff since 1998 this week, although analysts said sentiment remained fragile. “It’s likely the worst is over,” Patrick Bennett, a strategist at Canadian Imperial Bank of Commerce in Hong Kong, told Bloomberg News.

“PBoC intervention has calmed the market. There is not a sense that the onshore yuan will weaken forever.” The yuan ended at 6.3982 to the dollar yesterday, down from the previous day’s close of 6.3870 but stronger than the central bank’s reference rate.

China keeps a tight grip on the unit, allowing it to fluctuate up or down just 2% on either side of the reference rate, which it sets daily.

The PBoC on Tuesday announced a “one-time correction” of nearly two% in the yuan’s value against the greenback as it changed the mechanism.

Previously, it based the fixing on a poll of market-makers, but declared it would now also take into account the previous day’s close, foreign exchange supply and demand and the rates of major currencies.

It has since lowered the central rate twice more, and the week’s combined drop is the biggest since China set up its modern foreign exchange system in 1994, when it devalued the yuan by 33% at a stroke.

Analysts viewed the move as a way for China to both boost exports by making its goods cheaper abroad and push economic reforms as it seeks to become one of the reserve currencies in the International Monetary Fund’s SDR (special drawing rights) group.

The volatility in the normally stable unit has raised concerns, and many analysts predict the yuan will continue to depreciate in the coming months, impacting global trade flows.