Reuters/London

Default insurance markets show no obvious concern at the growing risk that Greece will leave the eurozone, suggesting investors can now contemplate a future for the currency union without Athens.

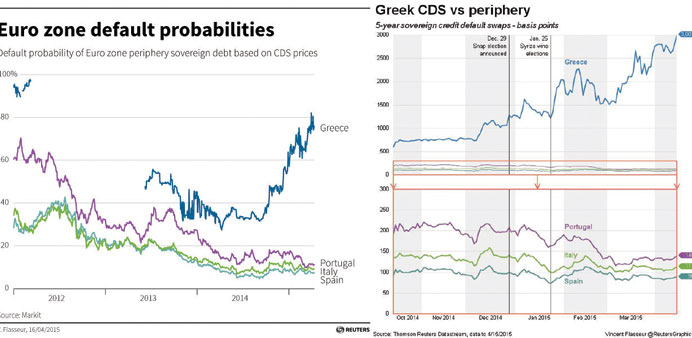

Default probabilities derived from credit default swaps — seen as the purest gauge of credit risk — have fallen this year in Italy, Spain and Portugal to around 10%, data from Markit show. In Greece, they have topped 80%.

In 2012, by contrast, the threat of Grexit pushed Portuguese, Spanish and Italian CDS prices to record highs. Default probabilities rose to between 40 and 60%.

During the debt crisis, the eurozone put in place a bailout fund and a mechanism to deal with troubled banks and the European Central Bank pledged to do whatever it takes to save the euro.

Eurozone banks now have only limited exposure to Greece and governments have never had easier access to markets, thanks to the ECB’s trillion-euro asset-purchase programme, which gives investors more confidence to risk lending to them.

“We see Greece as very isolated,” said Sandra Crowl, a member of the investment committee at Carmignac Gestion. “We’re in such a much better situation in 2015 than we were in 2012.”

Some analysts do say Grexit must have consequences, but its impact on other bloc members is impossible to quantify, making it difficult for investors to protect themselves in the CDS market.

Would it raise fears that other weaklings might leave or would the loss of a perennial laggard be good for the bloc? Portugal, considered the next weakest link, is implementing the reforms Brussels wants, so why would it go?

How would Berlin or the ECB react? Would Grexit be a gradual, controlled process or a sudden return to the drachma?

“Grexit is hard to define,” said Societe Generale rate strategist Ciaran O’Hagan.

“People speak about Grexit as if it’s a known entity. It’s not known at all ... The market is not reacting to this talk about Greece exit, which is consistent with the fact that there are many shades of grey out there.”