Reuters

London

The cost of hedging against sharp fluctuations in many emerging-market currencies jumped to multi-month highs yesterday, and derivatives markets indicate that bets against them are on the rise as the dollar strengthens.

A rising dollar and higher Treasury yields are spooking investors engaged in dollar-based carry trades – borrowing at low interest rates to invest in a higher-yielding, riskier asset. The result has been a sudden spike in volatility, after it spent the summer trading near long-term lows.

So far, the sell-off is nothing like the slide seen after Ben Bernanke, then the chairman of the US Federal Reserve, signalled last May an end to the Fed’s loose monetary policy. But market watchers fear it will pick up as the Fed’s September 16-17 meeting approaches.

“Our concern is that if fears of a more hawkish Fed become more pronounced” before the meeting, said Steven Englander, global head of G10 FX strategy at Citi. “We will see more pressure emerge on broader carry trades than has been the case.”

One-month implied volatility, a gauge of expected swings in some emerging-market currencies that is derived from options prices, has spiked, with the Turkish lira, Indian rupee and South African rand the main victims. Implied volatilities climb when a currency drops and investors rush to hedge against further losses.

For the Turkish lira, the one-month volatility, or vol in market parlance, is at 10.5, the highest in 2 1/2 months. Rand and rupee vols are at one-month highs. Three-month vols across the emerging-market currency spectrum have picked up an average 0.5 vol, Morgan Stanley analysts estimate.

Implied vol spikes have been far greater in G-10 currencies - euro/dollar one-month vol is at its highest since January at 7.6, dollar/yen vols at 8.7 and sterling/dollar vols at 11.35, at five-month and three-year highs respectively.

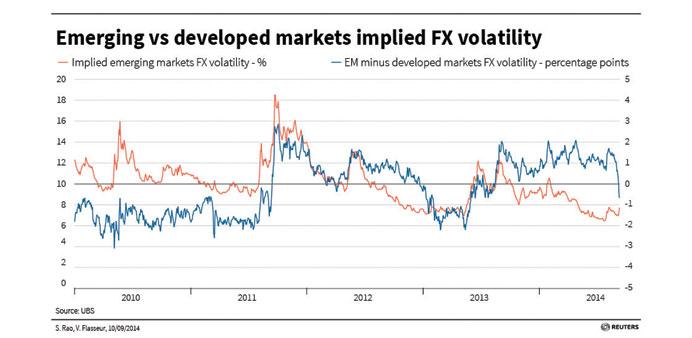

That is an ominous sign, says UBS strategist Manik Narain, who has analysed volatility surges in the past four years. Narain estimates three-month implied vols for a basket of nine emerging-market currencies at 7.7, up from 7 at the start of September.

But the discount to developed-market vols is the biggest since May 2013, just before the emerging market-wide rout took off.

“EM vols are now trading below that of G10, which traditionally has been a recipe of violent corrections,” Narain said. “The market has traded the recent pickup in volatility ... as primarily a developed-world issue, and there is a danger this transmits to EM more aggressively in the coming weeks.

“At this point I would be biased to being long vol in emerging markets.”

The latest jump in global volatility comes after a paper published by the San Francisco Fed on Monday noted that investors are pricing in a lower trajectory for interest rate rises than members of the Fed itself.

That lifted US yields to six week highs while the dollar rose to six-year highs against the yen and a 14-month peak against a basket of currencies, approaching levels not breached since 2010.