By Andy Home/London

On the London Metal Exchange (LME) three-month zinc has this week hit a 16-month high of $2,222 per tonne, eclipsing a first-quarter rally which stalled just shy of the $2,150 mark.

The galvanising metal has moved for the first time in two years to a premium to sister metal lead, although this may be as much to do with the heavy metal’s lethargy as anything else. Lead has done little more than shuffle sideways this year amid falling open interest and stagnant volumes.

Zinc, of course, has a compelling fundamental narrative of dwindling mine supply as some of the world’s largest operations come to the end of their natural life.

It is a story-line apparently echoed by the steady attrition of LME-registered stocks and monthly deficit headlines generated by the statistical updates from the International Lead and Zinc Study Group (ILZSG).

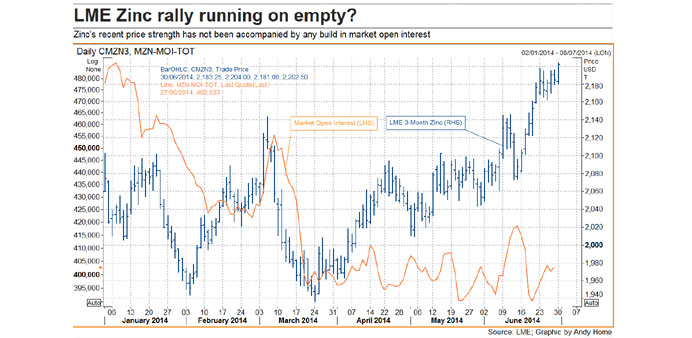

Yet both remain highly problematic market indicators, which is maybe why so few players are buying into the latest move. One of the curiosities of the latest zinc price surge is the fact that it has happened without any discernible change in market open interest.

It was a very different story back at the end of last year and beginning of this, when zinc went on its previous upside excursion. Open interest surged from under 400,000 lots in August 2013 to 486,000 lots in early January, coinciding with a price break up through the $2,100 level as speculative money flowed into the LME market to ride the bull story of mine supply shortfall.

By March both price and open interest had deflated in tandem as investors took profits and moved on to the next hot metals story offered by nickel after the Indonesian government’s ban on the export of nickel ore.

Right now open interest is still just over 400,000 lots and although there have been some minor flurries of activity, the market positioning landscape looks relatively featureless.

“The rally appears to be a bit half-hearted in nature,” concludes Leon Westgate, analyst at Standard Bank London, writing in the bank’s quarterly commodities review on June 27.

Drawing attention also to “pretty disappointing” volumes, Westgate suggests that “what does appear to have changed is that zinc is being traded on its own, or alongside lead, rather than against it as a relative value pair”.

Maybe the fact that zinc has been able to rally without any obvious speculative push is a positive sign that this market’s underlying deficit fundamentals are starting to assert themselves?

The only problem is that there is still scant evidence that there is any shortage of metal around.

LME stocks at 667,950 tonnes are still historically high and although they have fallen by over 260,000 tonnes this year, this may have very little to do with underlying market dynamics.

The biggest draws from the LME system this year have taken place at New Orleans, Detroit, Vlissingen and Antwerp, four warehouse locations characterised by load-out queues.

This means there is something of the rear-view window about current stock movements. Take, for example, Detroit, where zinc has been leaving daily since late April, but where the last sizeable cancellations occurred all the way back in November. It’s taken that long for the zinc to get to the front of the aluminium load-out queue. The picture is even hazier when it comes to New Orleans, where most of the LME zinc tonnage is concentrated and where most of what is there is being stored by Pacorini, the warehousing arm of Glencore. A whopping 265,000 tonnes have been loaded out at New Orleans since the start of January but has the zinc actually gone anywhere other than across a white line into off-market storage? It’s a suspicion that is only reinforced by the occasional mass movement of metal in the opposite direction, such as the 147,000 tonnes that “turned up” at the port in March.

LME stocks can be a problematic indicator of market balance at the best of times. In the recent history of zinc, they have been near useless, given the prominence of New Orleans, an LME location far removed from any zinc consumption hub.

But what of those monthly updates from the ILZSG? Surely, they are a “true” indicator that this market is shifting from years of structural oversupply to shortfall?

The latest Group bulletin, covering the first four months of this year, assesses the global market as being in supply deficit to the tune of 107,000 tonnes.

But here the problem is also one of stocks. Delving behind the ILZSG headlines reveals two very different dynamics at work. It is China that accounts for the global deficit calculation, while the rest of the world was in comfortable 145,000-tonne surplus over the January-April period.

And in China, as any copper trader can tell you, things get a bit statistically tricky. ILZSG, for example, uses an apparent consumption calculation, comprising production plus net imports plus/minus changes in visible stocks. On that basis “apparent” demand rose 12.4% in the first part of this year.

But, as sister organisation the International Copper Study Group has found out, builds in unreported stocks can seriously distort the mathematics. And particularly problematic are builds in bonded warehouse stocks, metal that has been counted as an “import” by China’s customs department but which has made it only as far as the port bonded zone.

China has been a net importer of commodity-grade zinc for a long time, not necessarily to fill domestic market shortfall but to meet financial demand for collateral to be used in the country’s shadow lending market, a trade that has recently come under the spotlight in the wake of the Qingdao scandal.

Most metal collateral financing is in the form of copper, but zinc has garnered its fair share of the business.

Analysts at Macquarie Bank, for example, estimate that bonded warehouse stocks of zinc have grown from around 50,000 tonnes at the end of last year to over 240,000 tonnes at the end of May (“Zinc: strong rally ahead of the curve”, June 30). That would account for a major part of the 311,000 tonnes of imports so far this year, serving to reduce ILZSG’s apparent demand indicator and its Chinese market deficit calculation.

All of which suggests there is a lot of surplus zinc still sloshing around the system, both in China and everywhere else.

That’s not to gainsay zinc’s background story of tightening mine supply but it’s to warn that this is going to be a long process, a slow grind rather than an explosion.

Even bullish analysts such as Stephen Briggs at BNP Paribas, argue that structural deficit won’t happen overnight. The first evidence might come as early as this year but the real impact will be felt next year and in 2016 (“Supply favours zinc over copper”, June 25, 2014).

Andy Home is a columnist for Reuters. The views expressed are his own.