Emerging markets (EMs) are likely to see negative trends continuing this year with the US Federal Reserve’s implementation of Quantitative Easing, QNB has said in a report.

Since the announcement by the US Federal Reserve (Fed) of the gradual reduction of its asset purchasing programme or the tapering of Quantitative Easing (QE), emerging markets have witnessed large capital outflows, a strong weakening of their currencies and reduced growth prospects.

If these negative trends continue in 2014 it will lead to lower economic growth, tighter macroeconomic policies and possible disruptions in the balance of payments (BOP) of selected countries.

The Fed announcement on May 18 last year of QE tapering and the start of its implementation in January 2014 have led to a sudden reversal of EM capital flows. “What had been the preferred destination of global capital in search for higher yields in the last few years suddenly became the emergency exit investors wanted to rush through. As a result, around $100bn were withdrawn from EM bonds and equities funds in the last eight months of 2013, based on data from EPFR Global. This led to a large weakening of EM currencies, a tightening of macroeconomic policies and a slowdown in economic activity,” QNB said.

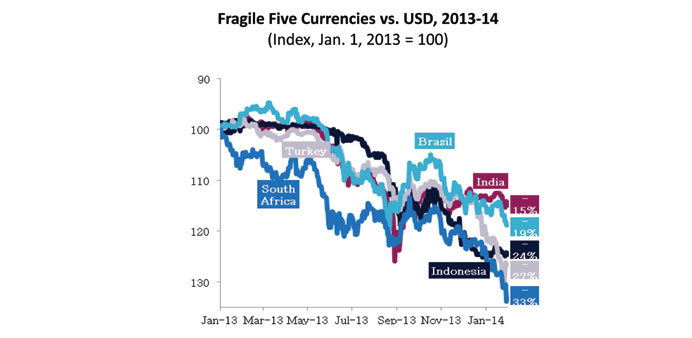

Five countries have been particularly affected by this sudden reversal of EM capital flows, given their large current-account deficits: Brazil, India, Indonesia, South Africa and Turkey. This group, called the ‘Fragile Five’, has seen the largest weakening of their currencies and the biggest impact on economic activity.

These trends are likely to continue in 2014. As the Fed gradually implements QE tapering during the year, additional capital is likely to flow out of EMs and be redeployed in advanced economies. This will put further pressure on EMs to tighten their fiscal and monetary policies and lead to lower economic growth.

In 2013, Brazil witnessed its largest capital outflows for ten years. This resulted in a significant weakening of the Brazilian real currency. The authorities responded with an aggressive tightening of monetary policy, pushing interest rates into double digits.

As a result, the economy went into recession in the third-quarter of 2013 and all coincident indicators point to a further decline in the fourth-quarter.

In 2014, further pressures on the exchange rate may lead to additional tightening of interest rates and a slow recovery in economic activity, notwithstanding the FIFA 2016 World Cup. As a result, QNB Group forecasts Brazil’s real GDP growth of 1%-1.5% in 2014.

India’s experience to-date with capital outflows has been better than other emerging markets. Skillful central bank policies have successfully stabilised the Indian rupee since October 2013 without the aggressive interest rate hike witnessed in Brazil. Instead, the authorities have curbed imports of gold and increased the incentives for sugar exports to reduce the current-account deficit.

However, India’s central bank did raise its policy rate by 25 basis points as EM currencies came under renewed pressure in the last week of January. Real GDP growth was probably just below 5% in 2013, although the momentum has been slowing, reflecting tighter domestic liquidity and a slowdown in consumer confidence and investment. QNB has forecast Indian real GDP growth in the 4%-4.5% range in 2014.

Indonesia has witnessed substantial capital outflows in 2013. As a result, the rupiah has lost almost a quarter of its value against the dollar. The authorities have so far been unable to stem the outflow despite a significant rise in interest rates as demand for imports remains robust.

Investment has slowed but private consumption remains strong on the back of a growing middle class. As a result, real GDP growth has slowed only moderately to an estimated 5.5% in 2013. QNB forecasts Indonesian real GDP growth to slow down further to 5.1% in 2014.

Amongst the Fragile Five, South Africa has witnessed the largest weakening of its currency to date (33%). This reflects both the largest current-account deficit (6.8% in Q3, 2013) and one of the lowest real GDP growth rates (1.8% in Q3 2013) on declining exports and domestic labor disruptions.

The South African Reserve Bank refused to increase interest rates until late January 2014 (the first hike in six years), letting the currency fall instead. However, the increase in interest rates did little to support the currency, which continued to weaken, as the move was presented by the central bank as a one-off measure. The prospects for 2014 remain modest on continued weakness of commodity exports and further social tensions.

As a result, QNB expects South African real GDP growth to remain in the 1.5%-2% range for 2014. Additional capital outflows are likely to lead to a further weakening of the South African rand.

Turkey has experienced a rapid outflow of capital and a sharp weakening of the Turkish lira (27%) as political tensions increased. In the January monetary policy meeting, the central bank elected to keep interest rates on hold. However, this was followed by a sharp weakening of the Lira, prompting the central bank to call an emergency meeting last week, when it decided to more than double its benchmark interest rate. The economy has been relatively unscathed in 2013, with real GDP growth estimated at 3.7%. However, the rapid weakening of the currency is likely to shake investor confidence further. As a result, QNB projects Turkish real GDP growth will slow to a range of 2%-2.5% in 2014, QNB said.