By Santhosh V Perumal/Business Reporter

Domestic institutions were seen to impart bullish momentum to the Qatar Exchange, which was on the positive turf during the week.

Foreign institutions were, however, seen neutral, notwithstanding their pulling out money from other emerging markets in view of seemingly brightened prospects in the US as Washington nears the deadline of easing its stimulus package.

Local retail investors were seen to inject a QR41.53mn (net) in the market, which closed 0.4% higher in the week, mainly supported by consumer goods, transport and telecom counters.

A half of the 42 stocks returned gains to investors in the week that saw the 41 listed companies together report a 14% surge in their total net profitability in the first half of this year.

Major gainers included Nakilat, Doha Bank, Commercial Bank, Mazaya Qatar, Ooredoo, Vodafone Qatar and Medicare Group; even as Industries Qatar, QNB, United Development Company and Barwa bucked the trend in the week that featured Gulf Drilling International, an IQ subsidiary, earn QR240mn revenue.

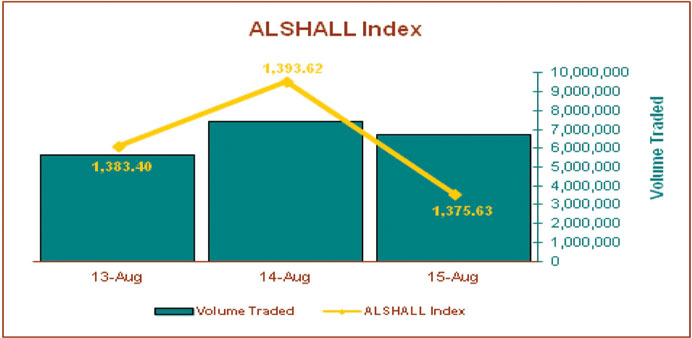

The 20-stock Total Return Index also gained 0.4% and All Share Index (comprising wider constituents) by 0.52%; even as Al Rayan Islamic Index was down 0.08% in the week that saw global credit rating agency Fitch affirm “A+” ratings with “stable” outlook on Nakilat’s debt programme. All the three indices factored in dividend income as well.

Under the All Share Index category, consumer goods segment witnessed 3.5% appreciation in their stock prices; transport (2.34%), telecom (1.35%), banks and financial services (0.3%) and insurance (0.15%); whereas realty stocks shrank 0.86% and industrials (0.17%).

Seven of the 12 banking stocks; four each of the eight consumer goods and the eight industrials; two each of five insurers and the two telecom; and one each of the four real estate and the three transport stocks closed positive in the week.

Market capitalisation expanded to QR541.43bn.

Of the 42 stocks, 21 advanced, while 19 declined and two were unchanged.

Qatari individual investors were bullish as they were net buyers to the tune of 4.61% or QR41.53mn; whereas their non-Qatari counterparts were profit takers to the extent of 8.43% or QR57.92mn.

Domestic institutions were bullish as they were net buyers to the tune of 1.8% or QR16.21mn; while their foreign counterparts were neutral.

Total trading volume fell 9% to 19.76mn shares, value by 13% to QR900.77mn and transactions by 17% to 11,015 in the week.

In terms of volume, the banks and financial services stocks accounted for 28.42% of the total, followed by transport (26.03%), industrials (15.23%) and realty (14.2%).

The banking sector witnessed 5.62mn shares being traded, transport (5.14mn), industrials (3.01mn), real estate (2.81mn), consumer goods (1.59mn), telecom (1.16mn) and insurance (0.43mn).

In terms of value, the banks and financial services sector led the chart with its stocks accounting for 30.58% of total trading value, followed by industrials (25.73%), consumer goods (14.34%) and transport (13.57%).

The banking and financial services sector saw stocks worth QR275.43mn being traded, industrials (QR231.81mn), consumer goods (QR129.20mn), transport (QR122.27mn), telecom (QR58.27mn), real estate (QR57.85mn) and insurance (QR25.93mn).

In terms of transactions, the banks and financial services sector’s share in total was 31.76%, industrials (22.91%), transport (14.54%) and consumer goods (13.74%).

The market witnessed as many as 3,498 banking transactions, industrials (2,524), transport (1,602), realty (978), telecom (548) and insurance (351).

In the debt market, there was no trading of bonds and treasury bills.