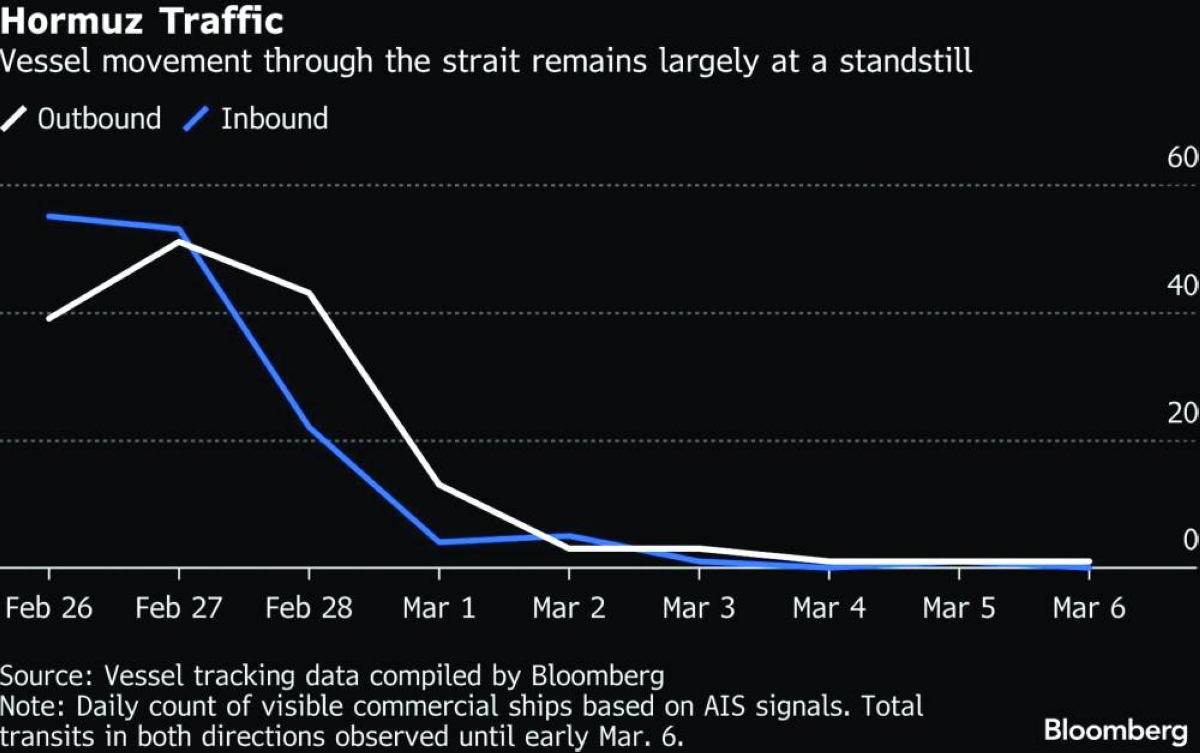

The economic fallout from the war in the Mideast is spreading outside the region.Gulf ports have turned into military targets. The vital Strait of Hormuz is effectively closed, sending fuel costs and shipping rates soaring. Vessels can’t reach a container hub that handles more volume than Rotterdam between four continents. Air cargo halted for a week will need time to work through backlogs as local carriers look to resume flights soon.The conflict between the US-Israel alliance and Iran is intensifying as it heads into a second week, straining global supply chains and raising questions about price spikes not seen since the pandemic.For companies exposed to the region, the risks are shortages of crucial components, higher costs and thinner profit margins. If that trickles down to stores, it’s another potential squeeze on consumers at a time many are already struggling with day-to-day expenses.Across financial markets, stocks, bonds and havens like the US dollar are reflecting those inflation concerns as well as the threats to households and businesses. Those are especially acute for countries still dealing with the legacy of Covid-era budget deficits, labour-market scars and subpar growth.“The world economy has been remarkably resilient, shock after shock,” International Monetary Fund Managing Director Kristalina Georgieva told Bloomberg Television on Friday in Bangkok. “But this resilience is being tested yet again and many countries step into more uncertainty with depleted buffers.”She added that central bankers need to be more attentive and fiscal authorities must be “very careful” in deploying stimulus given existing debt loads in many countries. “Every shock that comes on top of the previous one, the world faces it in a more difficult position,” Georgieva said.Beyond the old infrastructure of goods trade, bombs are dropping on the underpinnings of the digital economy: Data centres. Drone strikes damaged three facilities operated by Amazon.com Inc in the United Arab Emirates and Bahrain.For now, many economists say the overall impact on global GDP is likely to be modest and uneven, but that calculation will shift the longer the conflict drags on. Adding to the uncertainty in global trade is the lack of a clear roadmap for Washington’s tariff policy.In the US, Federal Reserve Governor Christopher Waller said that while consumers are likely to experience sticker shock as gas prices rise. He spoke before a Labor Department report Friday showed employers unexpectedly cut jobs in February and the unemployment rate rose, pointing to fragility in the job market.According to a Bloomberg Economics analysis, the biggest global economic headwinds come from energy markets, with about a fifth of global oil and LNG supplies passing through Hormuz. Asian countries like China, India, Korea, and Japan are top buyers of Gulf oil.By region, the fallout will be uneven. At Capital Economics, chief economist Neil Shearing said Asia, the euro area and the UK are more exposed than the US. Oxford Economics on Friday trimmed its UK economic growth forecast for 2026, saying the Iran conflict will push up inflation and household energy bills.Officials from the European Central Bank indicated they’re staying vigilant in case of any inflationary flareups, and executives with operations to the region aren’t hitting the panic button yet.“We see a world which is really under stress — that’s clear,” said Stefan Hartung, the chief executive officer of Robert Bosch GmbH, world’s biggest auto-parts maker.But the difficulties might be short-lived and many companies boosted resilience since the pandemic. Facing less transport capacity, “you need to be more like in the Covid times,” Hartung said in an interview, downplaying the possibility of widespread industry shortages. “I suspect that for the long term, we’ll see a stabilisation coming,” he said.Donald Trump’s administration is trying to relieve the energy supply crunch that’s helped push US retail gasoline prices to the highest level at any time under his terms as president. On Thursday, it cleared the way for India to temporarily increase its purchases of Russian oil, a policy reversal that reflects the concern about the energy fallout.But the global economy’s worries extend past oil, natural gas, jet fuel and gasoline.Bloomberg Economics estimates that almost 7% of global fertilizer exports, close to 6% of precious metals, 5.3% of aluminum and aluminum products and 4.4% of cement and other non-metallic minerals were shipped out of Gulf ports “and are at risk of disruption.”“This is a significant event — not just in the Middle East, but for supply chains and for the world,” Jan Rindbo, CEO with Danish shipping company D/S Norden A/S, one of the world’s largest transporters of raw materials.A Norden-chartered vessel that just offloaded grain in Saudi Arabia was about the leave the Gulf last Saturday when an Iranian order was broadcast for crews to turn around.“The longer this conflict continues, the greater the concern about what it means for the world,” Rindbo said in an interview. “We’re seeing people take a step back. It may be that they’re not buying quite as many raw materials as they otherwise would, as they wait to see how the situation develops.”Shipping through the region will soon come with a higher premium. German tire maker Continental AG on highlighted the risks on Wednesday, warning that the conflict may affect sales and earnings by driving up costs and disrupting its operations.“We are very early in this situation,” Chief Executive Officer Christian Kötz said. But the war has already created “more uncertainty.”In the short run, air cargo rates could double or triple on flights transiting the Middle East hubs, said Niall van de Wouw, chief airfreight officer with Xeneta, an Oslo-based digital freight platform. With freighters parked, as much as 18% of the world’s capacity disappeared this week.Tourism and business travel is suffered. London’s Heathrow Airport, the busiest in Europe, saw 300 flights scrapped since the conflict broke out, with more disruptions expected, Chief Executive Officer Thomas Woldbye said. He declined to say how much the disruption was costing per day.“We’re not talking a significant amount — not yet,” he said. “If it continues for a very long time, then we’ll have to look at that.”Much will depend on the resumption of flights and the return of capacity.State-owned Etihad said on Friday it will resume a limited commercial schedule between its hub in Abu Dhabi and a number of destinations in Europe, India, the US, and the Middle East, including Riyadh. Emirates plans to resume operations after flights were temporarily suspended on Saturday. Qatar Airways said it will operate limited flights to Doha on Sunday from London, Paris, Madrid, Rome, Frankfurt and Bangkok.Container lines are adjusting, too, though they’re less flexible to quick moves and more susceptible to attacks. Daily bookings placed by cargo owners looking to import goods into ports east of Hormuz plummeted by 81% over two just days this week, according to Vizion, which provides supply-chain visibility.There are roughly 100 container ships inside the Gulf, unable to leave given the security risks despite Trump’s pledge earlier this week to ensure safe passage using navy convoys. Dozens more are waiting to enter it or have been rerouted to other gateways, stretching capacity and raising the risk of bottlenecks elsewhere.Global shipping giants MSC Mediterranean Shipping Co, AP Moller-Maersk and several others have suspended bookings for routes linking Asia to the Middle East, and services connecting that region with Europe.That means congestion is spreading quickly in the region, but also throughout Asia, as ships offload cargo that had been bound for the Mideast at the nearest safe port.Nhava Sheva, India’s busiest container port sitting just east of Mumbai, was at 64% congestion as of Friday, skyrocketing from 10% since March 1, according to Xeneta’s Destine Ozuygur. Congestion at Singapore and Colombo is building as well, both are already above 40%.“Some secondary ports that we expect to see used as relay hubs, like Dar es Salaam, already have a baseline of 50% congestion and are now seeing wait time surge to 5+ days per vessel,” Ozuygur said Friday in a post on social media.Shutdowns at major petrochemical and refining facilities in the Gulf region are reverberating far beyond fuel markets to pharmaceutical supply chains, medical packaging and other health-care products, van de Wouw said.“Certainly this is a challenging situation,” DHL Group CEO Tobias Meyer said on Bloomberg Television this week, referring to the regional restrictions on air freight operations. “That will create some bottlenecks in the days and weeks to come, and similar on the ocean side – we’ll need to find new rotations for vessels.”He said DHL is deploying its fleet of trucks “to move cargo to airports that are open.”

. The US and Israel’s attacks on Iran, and Tehran’s retaliation across the Middle East, have disrupted supplies of fertiliser, and farmers worldwide are rushing to secure critical nutrients.")