When bitcoin broke into public consciousness in 2013, it couldn’t have been better: A digital currency being used to buy everything from drugs to cupcakes. Now there’s a new wave of excitement about an aspect of bitcoin that is a bit less attractive: Public online ledgers. Blockchain — the technology used for verifying and recording transactions that’s at the heart of bitcoin — is seen as having the potential to reshape the global financial system and possibly other industries.

The Situation

In August, the bitcoin community came together (mostly) over a software change meant to speed transaction times that had threatened a split. After the compromise, called SegWit2 was adopted, the price of bitcoins doubled, though the possibility of another split looms in November. In a setback in September, China was said to have decided to ban trading of bitcoin and other virtual currencies on domestic exchanges. The move came after China outlawed fundraising ventures by new forms of digital currencies in so-called initial coin offerings. Globally, investors have poured more than $2bn into ICOs despite warnings from regulators including the US Securities and Exchange Commission. Meanwhile, more than 100 banks including Barclays Bank and JPMorgan Chase & Co have joined the R3 consortium, created to find ways to use blockchain as a decentralised ledger to track money transfers and other transactions. The use of blockchain by banks and other companies may be sped up by new forms of encryption that can keep the details of a transaction private while allowing a network of users to verify them. Nasdaq Inc is already using blockchain for trading securities in private companies. Blockchain is also being tested by retailers like Wal-Mart Stores Inc for ensuring food safety, as industries explore what advantages the technology might hold over traditional databases.

The Background

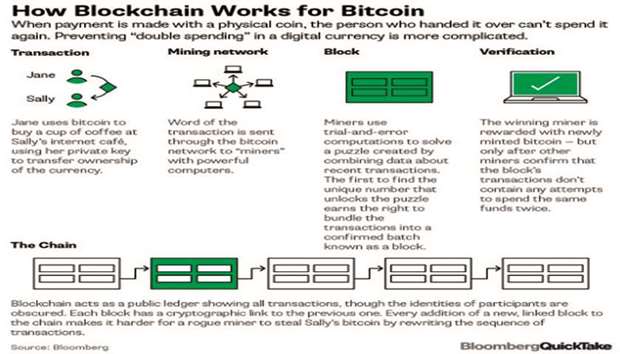

Virtual currencies aren’t new — online fantasy games have long used them — but the development of a secure digital currency without a central issuer rightly turned heads. The person or people who created the bitcoin system under the pseudonym Satoshi Nakamoto solved a problem central to any currency — preventing counterfeiting — and did it without relying on a government’s authority. The software also solved one specific hurdle for digital money — how to stop users from spending the same unit of currency twice. The breakthrough idea was blockchain, a publicly visible, anonymous online ledger that records every single bitcoin transaction. It’s maintained by a network of bitcoin “miners” whose computers perform the calculations that validate each transaction, preventing double-spending. The miners earn a reward of newly issued bitcoin. The pace of creation is limited, and no more than 21mn will ever be issued.

The Argument

Since bitcoin first boomed, there’s been no shortage of critics to call its rise a bubble and to argue that the currency has no intrinsic value. But entrepreneurs in the field say that focusing on the price of bitcoin is missing the point — its value is as proof of concept for a new kind of payment system not reliant on third parties like governments, big banks or credit-card companies. Promising applications of blockchain include moving money abroad, signing contracts, clearing complex financial transactions and as a medium for micro-payments in emerging countries. Others say blockchain advocates are hyping what amounts to no more than a new kind of database. Proponents of ether respond that the etherium blockchain does far more than let bitcoin users send value from one person to another. Its advocates think it could be a universally accessible machine for running businesses, as the technology allows people to do more complex actions in a decentralised manner.