By Clyde Russell/Launceston, Australia

Australia still has the Union Jack on its flag and the British queen on its coins, and was once described as the US “deputy sheriff” in Asia, but the real dependency relationship is with China.

Nowhere is this reality made more clear than in the quarterly outlook by the Bureau for Resources and Energy Economics (BREE), the government agency responsible for commodity exports and other forecasts.

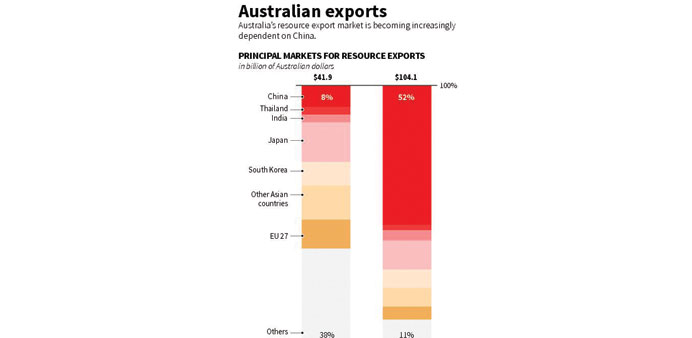

In the 2002-03 fiscal year, the biggest buyer of Australian resource and energy exports was Japan, which took 15% and 39% of the respective totals, according to BREE’s Resources and Energy Quarterly published June 25.

China was the fifth-biggest buyer of resources and sixth for energy, with a share of 8% and 3% respectively.

But by the 2012-13 fiscal year, China had accelerated into the top buyer of resources, with dominant share of 52%, and was second in energy purchases, taking 15%, behind Japan’s 41%.

It’s also likely that in years to come China will replace Japan as the top buyer of energy exports from Australia, given that Japan’s imports of liquefied natural gas (LNG) are probably at their peak, while China is just starting to ramp its purchases of the super-chilled fuel.

Australia has seven LNG plants currently under construction, and by the time these are all operational around 2018, LNG will become the nation’s second-biggest commodity export, trailing only iron ore.

Resource and energy exports accounted for 70.2% of all exports in 2012-13, up from 48.9% a decade earlier, underscoring just how vital commodity exports are to Australia’s economic wellbeing.

The strong growth of exports to China has continued in the 2013-14 fiscal year, with trade data showing exports reached A$101.4bn ($98.07bn) in the first 10 months of the fiscal year to end-April, a gain of 31.9% over the same period a year earlier.

Australian imports from China have also been gaining, but at a much slower pace, rising 11% to A$49.5bn in the first 10 months of the 2013-14 fiscal year.

This leaves a record trade surplus with China of A$50.9bn for the first 10 months, translating as CommSec Chief Economist Craig James put it, to more than A$2,200 ($2,079) for every Australian.

In contrast, the US trade deficit with China was $179.6bn for the 10 months from July last year, equivalent to about $577 for every American.

There is little doubt that Australia’s current economic wealth is very much related to China’s rapid urbanisation and its surge in commodity imports over the past decade.

From a political perspective, it’s probably less than ideal to be largely dependent on the economic fortunes of one major trading partner, especially one that with whom relations are somewhat testy.

But it’s equally hard to see just how Australia can diversify its export base, given China remains the driver of commodity demand and changes in its import appetite will dwarf any changes from other nations, even rapidly industrialising, high-populations Asian countries such as Indonesia and India.

Iron ore is a case in point, with Australia becoming increasingly dependent on Chinese buying.

Australia, the world’s largest iron ore exporter, will ship 680mn tonnes of the steel-making ingredient in 2014 and 764mn in 2015, according to BREE forecasts.

China, which buys about two-thirds of seaborne cargoes, will import 869mn tonnes this year and 927mn tonnes in 2015.

But iron ore prices are likely to fall, with BREE forecasting $97 a tonne in 2015, down from $105 this year. With the spot price at $94.90 on June 27, and more mine supply expected in Australia and number two exporter Brazil, the risk is that prices will be weaker than BREE expects.

This means Australian producers will have to mine and export more in order to maintain earnings, a situation that is likely to exacerbate global oversupply if competitors in other parts of the world adopt the same strategy.

It’s much the same story for coal, currently Australia’s second-largest resource export.

Prices for coking coal are forecast to average $122.50 a tonne in 2014 and $121.30 in 2015, down from $210 as recently as 2012, according to BREE. China buys about 30% of globally-traded coking coal.

In thermal coal, contract prices are expected to decline to $82 a tonne in 2014 and $77 in 2015, from $115 in 2012, BREE said. China is the world’s biggest importer of coal used in power plants.

For Australia, the reality is that it faces lower prices for its key commodity exports, and while demand growth remains positive, the rate of growth is moderating just as new supply comes online in many resource markets.

It also has to face up to China’s increasing role as a setter of commodity prices, with its imports, and the outlook for future imports, proving much of the prevailing market sentiment.

There is limited scope to diversify its resource exports, given the nature of mature markets in existing buyers such as Japan and South Korea, and the relatively small potential of new markets such as India and Indonesia, especially in comparison with China.

Australians tend to be keen followers of economic data, given one of the highest levels of share ownership and the fourth-largest pension fund pool in the world.

However, much of this focuses on domestic indicators such as gross domestic product and inflation.

There is nothing wrong with having strong cultural ties to former colonial overlord Britain, and being a solid US ally, even if this relationship isn’t quite as subservient as implied by the “deputy sheriff” characterisation of former US President George W Bush. But the real focus of Australia’s government and populace should be on the health and development of China, for their own future prosperity lies with Beijing, not London or Washington.

Clyde Russell is a Reuters columnist. The views expressed are his own.