By Pratap John

Chief Business Reporter

Qatar’s huge fiscal surplus for many years until 2014, government deposits, and additional assets of government related enterprises are adequate if the country chooses to pay down the fiscal shortfall using these reserves, a recent report has shown.

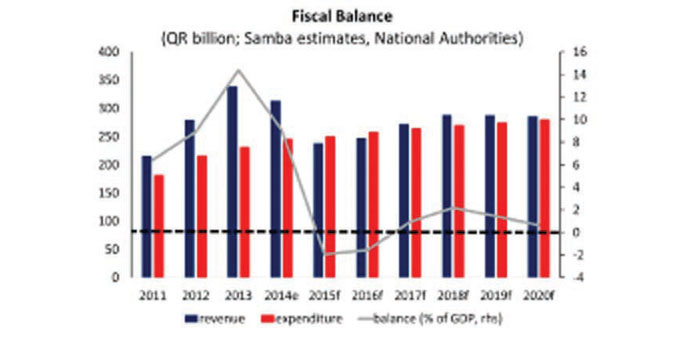

The country’s fiscal surplus in 2014 was $16bn, points out Samba Financial Group, which estimated that the reserves are enough to cover a deficit of the size it is forecasting in 2016 for five years. Surpluses of this size have been generated since 2000, the proceeds of which have been shared with the Qatar Investment Authority, which is now estimated to hold around $260bn in assets under management.

According to Samba, Qatar’s huge financial buffers and the capacity to issue domestic debt mean that the government is well able to finance any modest budget deficits that might stem from the spending on the National Development Strategy (NDS) through 2020.

“In this context, we project that the fiscal accounts will post deficits equivalent to 3% of GDP ($6.4bn) in total over 2015-16, as spending continues despite the slump in hydrocarbon revenues. We assume that from 2017 onwards, diminished but consistent fiscal surpluses will return, assuming oil prices recover in line with our forecasts. However, if hydrocarbon prices disappoint, then we could see small but manageable fiscal deficits in the medium term,” Samba said.

Although these resources are available, Samba said the government is likely to issue bonds to domestic banks. And in doing so, it will work towards the objective of developing a more comprehensive local debt market.

In fact, the Qatar Central Bank issued QR15bn ($4.1bn) of bonds recently, which were four times oversubscribed, although details on their tenor and yield are currently unavailable. This would take the total value of outstanding government bonds and sukuk to $24bn, or a manageable 13.5% of GDP.

“Although Qatar may produce a small fiscal deficit this year and next, the authorities have ample room to finance these without restricting spending. We do, however, think the change in hydrocarbon prices and implication for the budget will lead to a more prudent approach to government spending going forward,” Samba said.

“In fact, there is anecdotal evidence to suggest that although all existing planned project activity will go ahead, any new proposals will be stringently analysed and the less urgent items will be pushed back,” Samba said.