The People’s Bank of China’s (PBoC) decision to reduce the daily fix of its currency against the US dollar by 1.9%, devaluing it by the most in over two decades, has surprised many markets, QNB said in a report.

The PBoC also changed the way the daily fix is calculated to reflect market conditions, resulting in a further 1.6% depreciation on August 12. QNB said three factors might have prompted the Chinese authorities to act: a slowing economy; falling stock markets; and the need to meet the International Monetary Fund’s (IMF) criteria for the inclusion of the renminbi as a formal reserve currency.

Each day, the PBoC sets an official fixed exchange rate for the value of its currency against the US dollar. The interbank exchange rate is permitted to deviate from the daily fix by at most 2% on either direction. On August 11, the PBoC reduced the daily fix by 1.9%. This is the largest daily move since 1993, and came largely as a surprise to market participants, the report said.

According to QNB, three factors were at play, prompting the PBoC to take such a measure.

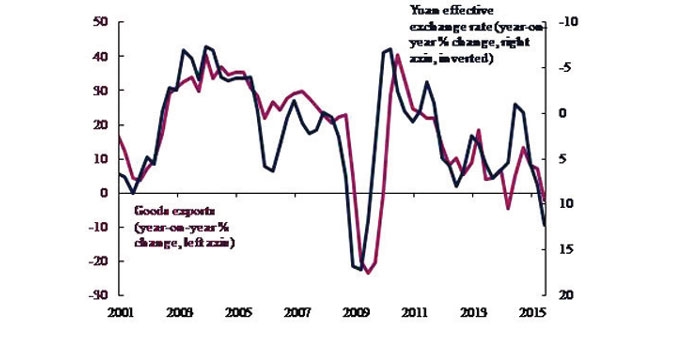

First, devaluation should boost exports and help the economy to grow. Although the yuan has been depreciating against the US dollar, it has been appreciating strongly against most other currencies. On a trade-weighted basis, the yuan appreciated by 13.6% in the 12 months to July 2015.

Given the strong link between the yuan’s effective exchange rate and Chinese export performance, the appreciation has resulted in exports dropping by 8.3% in July compared to a year earlier, much worse than the 1.5% decline that had been expected. The release of exports data might have prompted the Chinese authorities to act quickly and unexpectedly.

Second, devaluation should provide a lift to the turbulent Chinese stock market. Despite a host of measures by the Chinese authorities, the stock market has been volatile in recent weeks, with worries about potential spillovers to the real economy. By boosting exports, devaluation should improve the foreign earnings of Chinese companies, increasing their profits and therefore share prices.

The recent experiences of Japan and the eurozone confirm this link between currency depreciation and stock market performance, QNB said. Between November 2012 and May 2013, the yen depreciated by 29.0% against the US dollar. The yen move was associated with a 74.1% gain in the Japanese stock market. More recently, the euro weakened by 11.7% against the dollar between January and April 2015, and European equities gained 22.1% over the same period.

Third, the PBoC’s move might be motivated by the desire to be included in the IMF’s special drawing right (SDR) basket. The SDR is a global reserve asset, currently comprising the US dollar, euro, UK pound, and yen. The IMF is reviewing the basket this year and is considering the inclusion of the renminbi.

Criteria for inclusion include further liberalisation of the currency. To that end, the PBoC changed the way the daily fix is calculated. Market makers should now take into account changes to the previous day’s value, demand and supply conditions of the market as well as movements in other major currencies.

Will China succeed in achieving its three objectives? On the face of it, a devaluation of 1.9% is not significant enough to turn exports and the stock market around, the QNB report said.

But while the PBoC statement said that the devaluation was a “one-time correction,” the additional flexibility in setting the daily fix is expected to result in further weakening of the currency. Indeed, the yuan depreciated on each of the two days after the measures were introduced, resulting in a cumulative weakening of 4.7% over three days. If this trend continues, then it can provide the required boost to exports and the stock market, the report further said.

Furthermore, the IMF cautiously endorsed the measures taken by China, saying that the new regime is “a welcome step as it should allow market forces to have a greater role in determining the exchange rate”. But the IMF also emphasised that the changes have “no direct implications” for the criteria it would use to determine whether to include the renminbi in the SDR basket.

Overall, there are other problems with the Chinese economy beyond poor export performance and the stock market. QNB said China still has to undergo a painful credit bubble workout, and its transition towards a more consumer-led economy is far from smooth. Industrial production and retail sales data released last week showed the economy slowing down in July. China might manage to kill the three birds it is targeting with the yuan stone, but there are more to aim at, QNB report added.