Reuters/London

Investors dumped Greek bonds and US-listed Greek equity assets yesterday after Greece closed its banks and imposed capital controls over the weekend.

The Athens stock market was closed through to July 6 as part of broader capital controls, but trading in bonds and in US markets reflected investors’ alarm.

Greek bond yields rose sharply, according to financial platform Tradeweb, although strategists cautioned that capital controls would probably restrict trading by the domestic banks which hold most of the nation’s debt.

The Global X FTSE Greece exchange-traded fund (ETF) fell 15%, while National Bank of Greece’s American Depositary Receipts (ADRs) slumped by around 22%.

ETFs reflect a basket of underlying assets and are tradeable on international stock markets. ADRs are also typically used by U.S investors as a means of trading securities in a foreign company in dollars.

The ‘GREK’ ETF has fallen by nearly 30% since the start of 2015, pricing in deepening concerns over the Greek economy. ‘Short interest’ bets that the ETF will fall in future have also risen over the last month.

After receiving no increase in emergency funding for Greek lenders from the European Central Bank, Prime Minister Alexis Tsipras announced capital controls in a televised address on Sunday night to prevent banks from collapsing under the weight of mass withdrawals.

Index provider MSCI added yesterday that the closure of the Athens stock market and the imposition of capital controls could lead to Greece’s relegation from the benchmark emerging equity index and its reclassification as a “standalone” market.

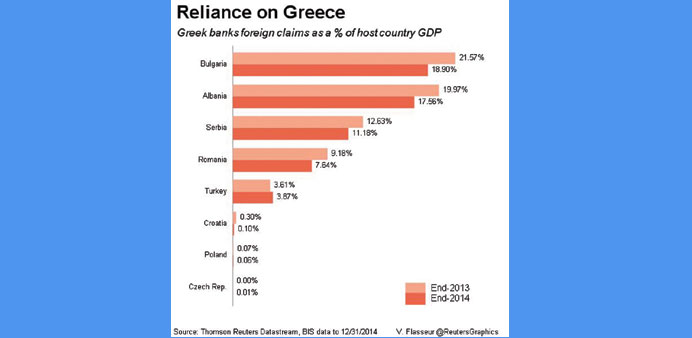

Meanwhile, hard currency bonds from Bulgaria and Romania fell by 1-2¢ yesterday and debt insurance costs inched higher as a default by Greece, with close trade and banking links to the Balkans, appeared inevitable. Greek banks have big geographic spread across the Balkans, with Alpha Bank for instance controlling lenders in Romania, Bulgaria, Serbia, Albania and Macedonia. Eurobank Ergasias and Piraeus Bank are both in Romania and Bulgaria and the former is also in Serbia.

Bulgaria’s 2024 euro-denominated issue fell 2.5¢ according to Tradeweb data, a 10-month low while Romania’s €1.2bn 2024 bond lost 1.2¢.

Serbia’s $1.5bn 2020 issue and Croatia’s 2022 €1.2bn bond also fell 1¢. Yield spreads for Romanian and Serbian dollar debt relative to US Treasuries widened by around 14 basis points on the day. “It’s regional contagion today... the more you are exposed to Greece the worse you are getting hit,” said Regis Chatellier, credit strategist at Societe Generale.

The countries’ credit default swaps, used to insure against default or restructuring, have been elevated all year, as the Greek crisis has deepened.

Analysts say Bulgaria looks most vulnerable, partly because its banking sector is relatively fragile, while Greek banks’ claims on Bulgaria stood at 18.9% of annual economic output by the end of 2014, the highest in the region.

But Bulgaria as well as the other Balkans are clearly much less vulnerable to any fallout from a Greek banking collapse than some years ago and that will cap market losses.

However, Greek banks still control the biggest lenders across south-east Europe and the worry is that if they go bankrupt, their overseas subsidiaries would suffer a domino effect.

That in turn would hit the finances of governments which might have to bail them out, ratings agency S&P has warned.

“We recommend remaining very cautious in the central European periphery, buying protection in Bulgaria — any withdrawal of deposits there, with subsequent euro or dollar purchases, would lead to an automatic drop in both the monetary base and (central bank) reserves,” Commerzbank told clients.