The recent surge in Qatar’s real estate prices is unlikely to destabilise the local economy’s robust growth as the market fundamentals appear solid, a new report has shown.

A sharp rise in asset prices also has the potential to destabilise the economy’s robust growth, points out Samba Financial Group.

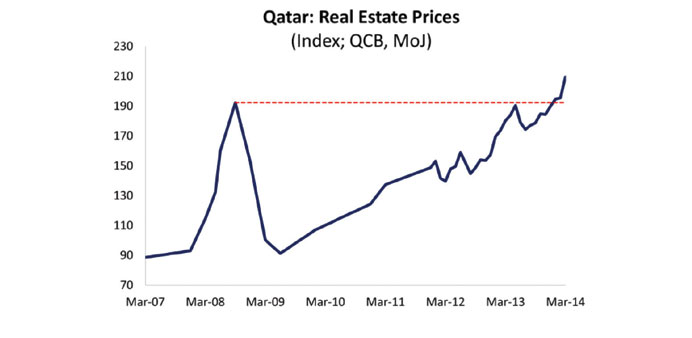

Since the trough in June 2009, the average price of real estate in Qatar has rebounded by 129.4% as of March 2014, and now stands 9% above its pre-recession peak, Samba said in its latest Qatar economic bulletin.

The pace of growth was especially marked in 2013 when prices rose by an average of 20%, though this is still well below the exuberant rate of increase seen prior to the crash in 2008. Year-on-year growth has moderated somewhat since the turn of the year, averaging 14.5% from January to March. “But clearly the dangers of any emergent real estate bubble need to be carefully assessed,” Samba said.

It is important to distinguish between growth underpinned by solid demand/supply dynamics and a rather more speculative and potentially destabilising element. Population growth and project spending point to strong fundamentals, which are driving the house-price growth of recent years.

However, Samba said Qatar’s real estate market is also an asset class, which has seen increased investor appetite of late. It is not easy to quantify the demand from investors, but the particularly strong house-price growth in designated areas that allow foreign ownership (The Pearl, West Bay etc) point to a significant contribution.

A demand-side factor underpinning the growth in real-estate prices is population growth. The population has expanded by 28.4% since May 2010 continuously outstripping the growth in the housing stock. There is reason for caution: although the total population in 2010 was 1.6mn, only 779,426 of these individuals lived in households, the implication being that the 820,000 others were housed in labour camps. Therefore the correlation between population growth and housing demand is perhaps not as strong as it might be.

Accompanying this is the aforementioned demand added by investors which appears to be significant but the lack of data limits the clarity of the situation. In the 2010 census, there was a sizeable surplus of housing units in the country as a whole, as compared to households.

House prices actually rose by 18.8% in 2010 and by 19.6% in 2011, suggesting that this apparent slack in the housing market was filled – at least in part - by investors.

The supply outlook is mixed, with data scarce.

According to a report by Colliers, Doha’s residential market comprised 129,000 units in 2014, whilst demand is estimated at 177,000. Taking into account the construction pipeline, Colliers projects the cumulative supply of residential units in Doha to be 151,000 by 2018. They foresee a compound average growth rate of 3% from 2014 onwards, lower than the 8% seen previously. The implication that the supply of housing stock will continue to grow at a slower pace than the population, gives some support for further price rises.

Colliers state that Doha is now a ‘significantly undersupplied market’. Adding to this is the ongoing pipeline of infrastructure project which is eating up land in Qatar, exacerbating the perceived supply shortage. This has been particularly prominent around Doha, where land sales accounted for 77% of total real estate transactions in Q1, 2014.

The IMF recently stated that “assessing when house prices are out of line with economic fundamentals is as much art as science”. Without up-to-date population data it is hard to get a firm picture on the supply/demand balance, and how much influence speculative investors are having on price rises. There is little doubt that real estate in Qatar is now an asset class and is therefore exposed to swings in investor sentiment.

“But we also note that Qatar’s house-price growth has been relatively modest when compared to some of its GCC neighbours. Coupled with the strong demand-side population growth and supply-side project expansion eating up land, we are reasonably comfortable that the real-estate market is in line with fundamentals. However, the data issues provide reason for caution, and the need for a more highly regulated environment and an improvement to the country’s early warning system,” Samba said.