More work needs to be done to reduce wasteful spending, spur economic growth and reduce the high unemployment rates in several Middle East and North African (Mena) countries, according to QNB, which said the IMF has been successful in recent years in restoring confidence in the Mena countries.

Since 2011, the global lender has pledged about $10bn in financial support to Jordan, Morocco and Tunisia to implement their adjustment programmes and restore investor confidence.

Despite their individual differences, the ongoing programmes share three common causes, namely large domestic subsidies, regional instability and unfavourable global economic conditions, QNB said in a report

“The plan to tackle the corresponding domestic and external economic imbalances in the three countries has been successful, although more work needs to be done to reduce wasteful spending, spur economic growth and reduce the high unemployment rates,” the report said.

Jordan, Morocco and Tunisia shared three causes for their crises: large expenditure on subsidies, regional political instability and unfavourable global economic conditions. First, each of them suffered from a structurally large bill on domestic subsidies, ranging in 2011 from about 4% of GDP in Tunisia to around 6% of GDP in both Jordan and Morocco. This resulted in a significant economic and fiscal drag on its own. It also meant that these economies were particularly vulnerable to the two other shocks that hit them.

The second shock was the wave of political instability, which has swept the region since 2011. In the case of Jordan, this led to a disruption of gas supplies from Egypt, a breakdown of trade channels and a large inflow of Syrian refugees.

The instability also caused a slowdown in economic activity in Tunisia and a rise in popular demands in all three countries, which put more pressure on public finances.

The third common cause was the challenging global economic environment exemplified by the crisis in the eurozone — largest trading partner of Tunisia and Morocco — and the high global energy and food prices, which affected the three oil-importing countries.

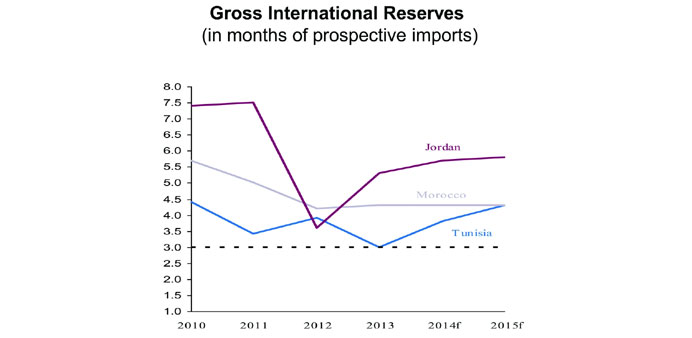

The resulting negative shocks manifested themselves through three common symptoms: larger fiscal deficits, wider current account deficits and depletion of international reserves. The slowdown in economic activity lowered tax receipts which, together with the large subsidy costs, resulted in larger fiscal deficits.

Similarly, the current account deficits widened as the weakness in the economies of trading partners and the breakdown of trade channels adversely impacted exports, while the imports bill rose due to higher international energy and food prices. This led to depletion in international reserves, which declined to levels close to three-months of prospective import cover, generally considered the minimum safety level for fixed exchange rate regimes.

The IMF-supported programmes in Jordan, Morocco and Tunisia designed to tackle these negative shocks have common elements centred around three axes: subsidy reforms, mobilisation of external funds and prudent monetary policy. A thorough and well-planned programme of subsidy reforms was needed to tackle the inefficient and structurally large subsidy bill without breaking down social safety nets.

In principle, this should involve the removal of price support provided by the government, the benefit of which has been mostly captured by higher-income groups. Inevitably, this would also hurt the poor by raising their cost of living as domestic food and energy prices go up, so the reforms should also involve protection for lower-income groups through targeted cash transfers or more-focused subsidy systems.

The second axis involved the mobilisation of funds in the form of additional loans and grants not just from other countries or international organisations but also from financial markets.

Both Morocco and Jordan have managed to successfully issue US dollar-denominated bonds, signalling investor confidence in the two economies against the assurances provided by the IMF support.

The final axis is prudent monetary policy which involves raising interest rates, where appropriate, to restore market confidence, reduce dollarisation of deposits and build up reserves.

While the stabilisation of the macroeconomic environment and the restoration of market confidence helped avert an immediate crisis, the three economies still face other challenges. Growth remains tepid: Jordan, Morocco and Tunisia are all forecast to grow by 3-4% in real terms in 2014.

Unemployment remains stubbornly high: it is expected to be 12.5% in Jordan, 9.1% in Morocco and 16.0% in Tunisia in 2014. In addition, despite the progress made on reducing the subsidy bills, more needs to be done to further cut wasteful spending, the report said.