Qatar’s banking sector’s “profitability metrics” remain strong with “stable outlook and promising prospects” as government spending and global expansion will provide growth opportunities in 2013 / 14, QNB has said in a report.

“We expect Qatar’s banking sector to maintain its profitability in 2013-14. It is expected to continue on its strong growth trajectory as rising infrastructure spending by the government provides for ample opportunities in credit growth, coupled with further global expansion by local banks,” QNB said in its ‘Qatar Economic Insight 2013’.

The net profit of Qatari banks increased by 7.5% in 2012 to reach $4.4bn, QNB said. The return on average equity (ROAE) stood at 17.5%, while the return on average assets was at 2.7%. Higher lending, a low cost base and low provisioning requirements have supported the banks overall profitability.

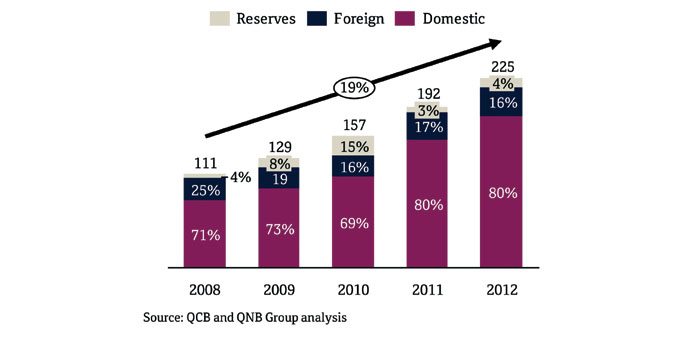

The total banking sector assets stood at $225bn in 2012.

Qatar has the third largest banking sector assets in the GCC and has stood at the forefront of asset growth in the region.

Qatar had the highest growth rate of 18% in banking assets region-wide in 2012. The main growth driver was domestic assets, which comprised mainly of credit (71%) and investment (21%) that increased by 27% and 11% respectively in 2012.

Conventional banks account for the largest share of assets (72%) and, therefore, were largely responsible for the strong growth in assets, with their balance sheets expanding by 18% in 2012.

The overall credit facilities extended by local banks increased by 26% in 2012 to $140bn, QNB said. Credit facilities to the public sector account for the largest portion of overall loans.

Lending to the public sector shot up by 47% in 2012 to $60bn and has been increasing by an average of 43% over the past three years.

This is mainly due to the increasing use of short-medium term funding by the public sector to finance ongoing infrastructure projects. Growth in loans to the real estate sector and consumption (retail) slowed down in 2012 mainly due to regulation on lending limits set by the QCB.

Banking sector deposits increased by 26% in 2012 to $126bn. The public sector was the key growth driver for overall gains in banking sector deposits.

Deposits from the public sector rose sharply by 44% ($15bn) in 2012 and came mainly in the form of long-term foreign currency deposits. Non-resident deposits went up by 105% ($6bn) in 2012, QNB said.

Qatar’s banking sector is highly concentrated with the top five banks accounting for 78% of total banking sectors assets in 2012. QNB is the largest bank in the Mena region with total assets of $100.8bn in 2012.

There were some 18 QCB licensed banks operating in Qatar as of 2012. This includes six commercial, four Islamic and seven foreign banks. Also present is the government-owned Qatar Development Bank.