By Santhosh V Perumal/Business Reporter

Buying interests from local retail investors and domestic institutions kept the Qatar Exchange (QE) afloat in the positive path for the fifth consecutive week.

However, Dubai, Abu Dhabi, Kuwait and Muscat bourses were splendid in their performance with their key indices returning double-digit appreciation year-to-date (YTD).

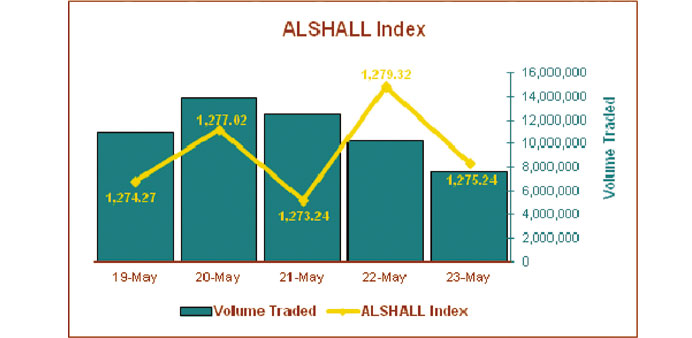

Notwithstanding the strong profit booking pressure from foreign institutions, the 20-stock Qatar Index gained 1.48% in the review week that saw Kuwait bourse add 3.19%, Saudi Arabia (3.02%), Bahrain (1.96%) and Dubai (0.42%); while Abu Dhabi and Muscat fell 1.53% and 0.2% respectively.

The insurance, transport and realty counters witnessed out-performance of the key index in the week that featured a Barclays report which said Qatar is expected to grow annually by 5%-6% in the next few years, mainly supported by non-hydrocarbon sector and fiscal deficit is not expected before 2017-18.

The Total Return Index gained 1.48% and Al Rayan Islamic Index 1.44% in the week that saw Doha Bank earmark QR12bn for lending to high potential clients in Qatar, the UAE and Kuwait.

The QE Index has risen 8.25% YTD against Dubai’s stupendous 42.1% gain, Kuwait (37.41%), Abu Dhabi (31.53%), Muscat (10.47%), Bahrain (9.83%) and Saudi Arabia (8.26%).

About 74% of the stocks extended gains to investors with major movers being Qatar Islamic Insurance, Al Khaleej Insurance and Reinsurance, Qatar Insurance, United Development Company (UDC), Barwa, Mazaya Qatar, Ooredoo, Milaha, Nakilat, Commercial Bank, QNB, Qatar Islamic Bank, International Islamic, Masraf Al Rayan and Gulf International Services in the week.

However, Widam Food, Vodafone Qatar, Industries Qatar and Doha Bank bucked the trend in the week that saw another report from Barclays which said Qatar’s banks’ credit is likely to grow 14%-17% year-on-year in 2013, much lower than the average 27% growth in the previous two years.

UDC, Nakilat and Barwa were among the most active by both volume and value in the week that saw Barwa’s plans to unveil several groundbreaking projects, including Oryx Island, at the Cityscape Qatar 2013, which will begin this week.

The QE All Share Index (comprising wider constituents) had risen 1.37% with the insurance group shooting up 7.54%, transport (4.8%), realty (4.69%), telecom (1.34%), banks and financial services (1.25%) and consumer goods (0.51%); while that of industrials fell 0.5% in the review week that witnessed al khaliji join hands with UDC to offer special mortgage loans for buying properties in the Pearl Qatar.

Transport, telecom, industrials, consumer goods, insurance, banking and real estate sectors indices had gained YTD 22.85%, 19.36%, 18.84%, 18.75%, 15.52%, 9.33% and 9.29% respectively.

Of the 42 stocks; 31 advanced, while only eight fell, two were unchanged and one was not traded in the week that saw a Financial Times specialist agency fDi Intelligence report that the outward foreign direct investments (FDI) from Qatar witnessed 29% fall; even as those from the Middle East and Africa (MEA) grew 9% in 2012.

Ten of the 12 banks and financial institutions; five each of the eight industrials; the eight consumer goods and the five insurers; three of the four realty; two of the three transport and one of the two telecom stocks closed higher in the week.

Market capitalisation swelled 0.77%, or about QR4bn to QR501.91bn, with small, micro, mid and large cap equities gaining 2.86%, 1.72%, 1.61% and 0.88% respectively.

Small, mid and large cap equities have gained YTD 10.15%, 9.83% and 7.41% respectively; while micro caps fell 1.42%.

Domestic institutions turned net buyers to the tune of 7.9% or QR150.25mn. A higher 29.38% of them were into buying against 27.65% the previous week whereas a much lower 21.48% were into selling compared to 33.41%.

Qatari retail investors’ net profit booking fell to 5.88% or QR111.83mn. A higher 39.63% of them were into buying against 35.11% the week ended May 16 although a marginally higher 45.51% into selling compared to 44.02%.

Foreign institutions turned net sellers to the extent of 0.35% or QR6.66mn. A lower 17.55% of them bought equities against 26.85% the previous week while a higher 17.9% of them offloaded compared to 9.91%.

Non-Qatari individual investors’ net profit booking fell to 1.67% or QR31.76mn. A higher 13.44% of them purchased stocks against 10.39% the week ended May 16 and a higher 15.11% sold compared to 12.65%.

Total trading volume was up 8% to 55.09mn shares, value by 9% to QR1.90bn and transactions by 22% to 27,708 in the week.

In terms of volume, the real estate stocks accounted for 34% of the total against 29.74% the previous week, banks and financial services 25% (24.33%), transport 14.96% (15.31%), industrials 9.33% (8.35%), telecom 6.81% (15.57%), consumer goods 6.28% (5.79%) and insurance 3.63% (0.91%).

The insurance sector witnessed more than quadrupling of trading volume to 2mn shares, realty surged 24% to 18.73mn, industrials by 21% to 5.14mn, consumer goods by 18% to 3.46mn, banks and financial services by 11% to 13.77mn and transport by 6% to 8.24mn; while that of telecom shrank 53% to 3.75mn.

In terms of value, the banks and financial services stocks constituted 29.57% of the total compared to 37.95% a week ago, real estate 20.8% (16.47%), industrials 19.73% (15.75%), transport 11.15% (10.34%), consumer goods 9.17% (11.76%), insurance 5.69% (1.3%) and telecom 3.88% (6.43%).

The insurance sector stocks’ trading value jumped almost five-fold to QR108.27mn, realty soared 37% to QR395.62mn, industrials by 36% to QR375.26mn and transport by 17% to QR212.04mn; whereas that of telecom plunged 34% to QR73.82mn, banks and financial services by 15% to QR562.36mn and consumer goods by 15% to QR174.47mn.

In terms of transactions, the banks and financial services sector’s share in total was 30.44% against 28.69% the previous week, real estate 21.46% (21.67%), industrials 18.2% (16.87%), transport 11.6% (11.26%), consumer goods 8.68% (11.46%), insurance 4.89% (1.75%) and telecom 4.74% (8.29%).

The insurance sector stocks transactions more than tripled to 1,355; industrials expanded 32% to 5,044; banks and financial services by 30% to 8,434; transport by 26% to 3,213 and realty by 21% to 5,945; whereas those of telecom plummeted 30% to 1,312 and consumer goods by 7% to 2,405.

In the debt market, there was no trading of treasury bills during the week.